For the better part of two decades, China has been the global automobile industry’s greatest growth market. Since 2000, sales of passenger and light commercial vehicles have increased about tenfold—to more than 20 million units a year—surpassing sales even in the U.S. and representing compound annual growth of about 20 percent.

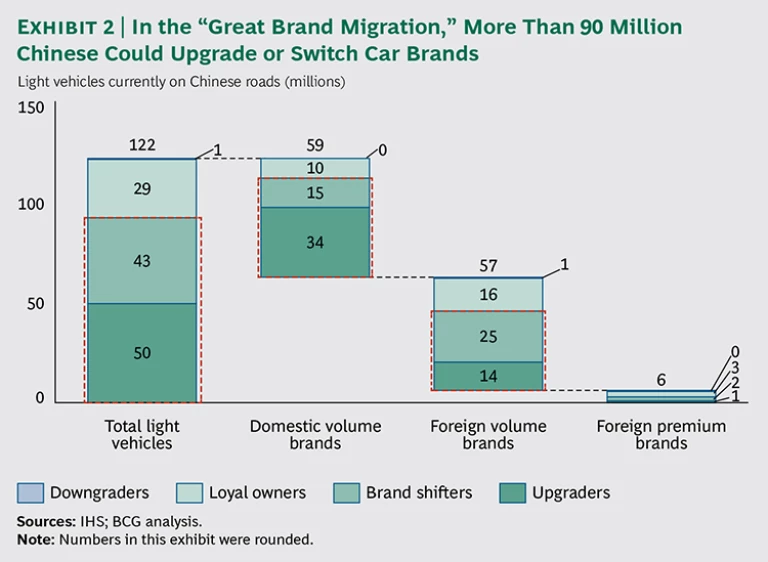

Now that this golden era of super-fast growth is winding down, the vast Chinese car market is entering a new pivotal stage. Instead of only racing to win over first-time buyers, domestic and foreign automakers alike must secure the loyalty of existing customers. Based on research by The Boston Consulting Group’s Center for Consumer and Customer Insight in China, at least three-quarters of Chinese car owners—representing a massive installed base of more than 90 million vehicles—are planning to switch brands when they purchase their next vehicle. We call this impending shift the “great brand migration.”

The reasons for this customer disloyalty vary. A large portion of China’s increasingly affluent consumers want to trade up to higher-quality or more prestigious brands now that they can afford to do so. Millions of others, however, intend to switch to a different car brand within the same segment. Why? When many of these consumers bought their first cars, they turned by default to brands they knew. Now, however, they are better informed about their options, and a high number of Chinese drivers are dissatisfied with various aspects of the cars they own.

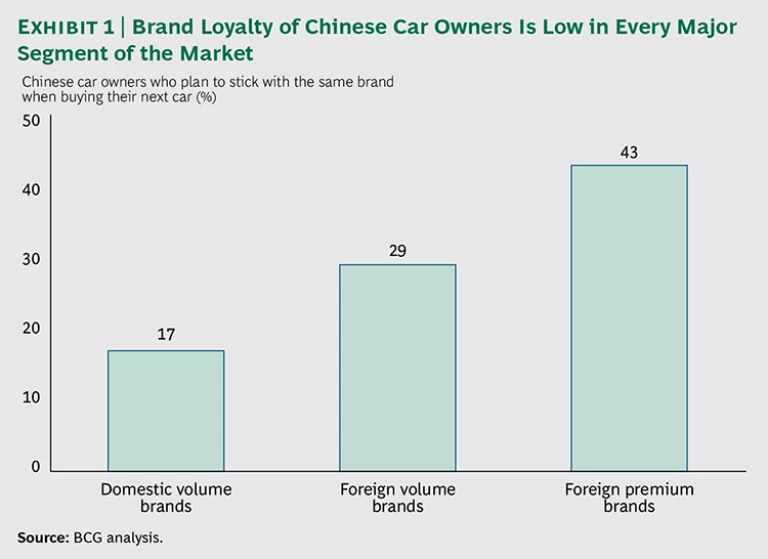

The findings of BCG interviews with 2,400 car owners in China indicate that Chinese drivers are far more eager to switch brands than average consumers in developed economies. This sentiment, moreover, resounded among owners in every segment—from those driving basic domestic models to owners of pricey luxury vehicles. (See Exhibit 1.)

The following are some of the most important facts about the Chinese market that we gathered from our interviews:

- Nearly 85 percent of owners of cars manufactured by domestic Chinese companies—which tend to be among the least expensive on the market—said that they plan to switch brands when they buy their next car. Of these respondents, only around 30 percent said that they plan to buy a different local Chinese brand. Quality and performance are among the most frequently mentioned reasons for switching brands.

- More than 70 percent of owners of midprice “volume brand” cars—a segment controlled by multinational joint ventures—said they intend to switch brands. Nearly half of these consumers plan to remain within the volume segment, but many intend to buy a more prestigious brand.

- Around 45 percent of owners of premium cars—a segment dominated by a few European luxury brands—intend to buy another car of the same brand. While intended loyalty in this segment is high compared with domestic and volume brands, it is somewhat lower in China than in developed economies. The leading reasons customers cite for switching brands are that the comfort and service experience of premium cars don’t live up to their expectations of luxury.

- Around 40 percent of car owners who plan to trade up from domestic brands are choosing one foreign volume brand—Volkswagen (VW)—which is manufactured by the joint ventures Shanghai Volkswagen and FAW Volkswagen. Nearly 90 percent of Chinese owners who plan to trade up from volume to premium cars are choosing one of three brands: Audi, BMW, and Mercedes-Benz.

These findings suggest that the next great battle in China’s car market will be waged over customer loyalty. To be sure, China is likely to remain one of the world’s hottest markets for first-time car buyers for the rest of this decade. But success in China will increasingly depend more on automakers’ ability to keep existing customers and to lure customers away from competitors. For companies with a portfolio of car brands across a full range of price points, the ultimate goal should be to build sufficient loyalty in order to win customers and hold on to them as they migrate from lower-priced vehicles to the luxury end—rather than to have to capture these same customers over and over again.

For the handful of automakers that enjoy rock-solid reputations and consumer loyalty in China, the great brand migration is an enormous opportunity to increase share in a still-growing market. Most other car companies, however, must raise their game considerably in order to win the intensifying battle for loyalty.

Domestic brands are under particular pressure as many have been losing market share in China. They must improve their reputations for quality and performance—a daunting task given China’s intense price competition for economy vehicles. But not even multinationals can take their success for granted. The advantages that foreign brands enjoyed among first-time Chinese car buyers are starting to fade as attractive alternatives emerge. Chinese consumers are maturing as car buyers, and they clearly expect better quality, service, and performance for their money.

For car companies that meet consumer expectations and position their brands correctly, the prize to be won in China is immense.

Compared with the more mature economies of the West and Japan, China’s automotive market remains highly attractive. Despite two decades of rapid growth, there are fewer than 100 light vehicles per 1,000 people in China, compared with close to 800 per 1,000 in the United States.

But the boom is beginning to fade. Since 2000, China’s car market has roughly doubled every four years and has far surpassed that of the U.S. Growth for the next four years, however, is projected to decelerate to a 6 to 9 percent rate, and by 2020 it is expected to settle down to an annual rate of 2 to 3 percent. At the same time, China’s car market has become far more competitive. In 2000, about 80 models of light vehicles were on the market, each with annual sales of at least 1,000 units. Today, there are nearly 500 models.

To explore the implications for automakers, we studied China’s car owners—and the shifts in brands many of them plan to make—by dividing types of brands into three segments. (See Exhibit 2.)

- Domestic volume brands dominate the market for basic, economy vehicles priced at less than $13,000. With about 9.4 million units sold in 2013, local Chinese brands command around 44 percent of the country’s overall car and light commercial-vehicle market. Along with Wuling, Changan, and Dongfeng, BYD and Great Wall are among the leading domestic volume brands. There are around 56 million domestic-brand vehicles on Chinese roads. Based on the share of current car owners who plan to switch brands or trade up, this indicates a potential brand churn of almost 50 million vehicles.

- Foreign volume brands are cars and light commercial vehicles priced between $13,000 and $41,000. While some Chinese companies market cars in this price range, the segment is dominated by foreign joint ventures that assemble vehicles in China. Several automakers, such as General Motors and Nissan, market separate brands at the lower and higher ends of the volume segment. Foreign volume brands account for nearly half of the Chinese car market, with about 10.4 million units sold in 2013. Volkswagen is the market leader, followed by Hyundai and Toyota. There currently are about 54 million foreign-volume-brand cars on Chinese roads, suggesting a potential brand churn of around 40 million vehicles.

- Foreign premium brands are cars at the high end of the Chinese car market, priced at $41,000 and up. Cars selling for $80,000 and above are regarded as “super premium.” Premium and super-premium cars account for roughly 7 percent of the Chinese market, with about 1.5 million units sold in 2013. Audi, BMW, and Mercedes-Benz are the clear leaders, while Land Rover and Porsche are well positioned in their niche segments. There is an estimated installed base of about 6 million premium cars in China, suggesting a brand churn of more than 3 million vehicles.

Why Chinese Car Owners Are Looking to Switch

The first step to improving customer loyalty in China is to understand why owners abandon their current brands in the first place. What needs aren’t being met? What are the brand migration patterns?

We asked Chinese car owners which brand they now own and determined which segment it’s in. Then we asked which type of brand they plan to purchase next. Customers that expect to change brands fall into two basic categories: brand shifters, who plan to buy another vehicle in the same category; and upgraders, who plan to trade up to a car in a higher category.

To understand the factors that are driving these car owners’ decisions, we asked them to rate the most important functional and emotional attributes that they are looking for in their next car. Functional attributes include performance, quality, safety, reliability, interior design, and after-sales experience. Emotional attributes reflect the feelings that consumers get by owning and driving the car. For example, a particular brand might make consumers feel more secure or athletic or give them the sense that they stand out more from the crowd.

The top responses varied—often markedly—depending on the car segment and on whether customers indicated that they are likely to be brand shifters or upgraders.

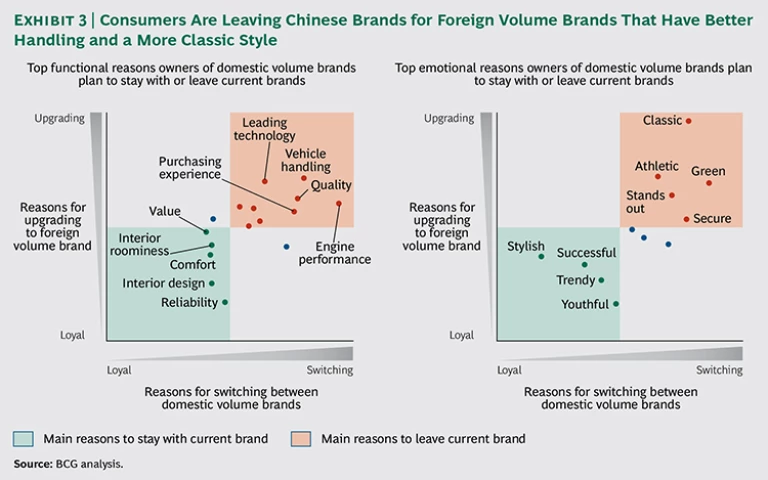

Domestic Volume Brands. Only 17 percent of people who own cars made by Chinese companies said they will stay with their current brand when they buy another car. Twenty-five percent said they expect to shift to another domestic local brand, and 58 percent said they are switching brands in order to trade up.

Why are so many Chinese car owners shifting to another brand? Disappointment with basic quality and performance was the chief functional reason that car owners cited for leaving their current domestic Chinese brands. Service was another major issue. Engine performance, vehicle handling, and quality were the top three unmet needs of owners of local Chinese cars among brand shifters. They also cited greater dissatisfaction with the purchase and after-sales experience than loyal customers did. Upgraders named technology, vehicle handling, and quality as the top unmet functional needs of their Chinese brand cars. This suggests that domestic carmakers are still struggling to meet drivers’ basic requirements.

The good news for Chinese car brands is that their current customers are generally fine with the comfort, roominess, interior design, and reliability of their current cars. Customers also regard their cars as a good value. In terms of emotional attributes, brand shifters said they are looking for a secure image. Upgraders felt strongly that their current Chinese brands did not project a sufficiently athletic image. Both groups of consumers want a classic look. And they are relatively satisfied that their current cars seemed youthful and stylish and made them seem successful. (See Exhibit 3.)

These findings suggest that domestic Chinese car brands are seen as offering good value and doing a sufficient job of satisfying certain needs, such as interior design. But to keep customers, Chinese volume brands must push much harder to improve quality and technology. At the same time, these brands must invest in marketing to ensure that this progress translates into a sound and reliable brand image.

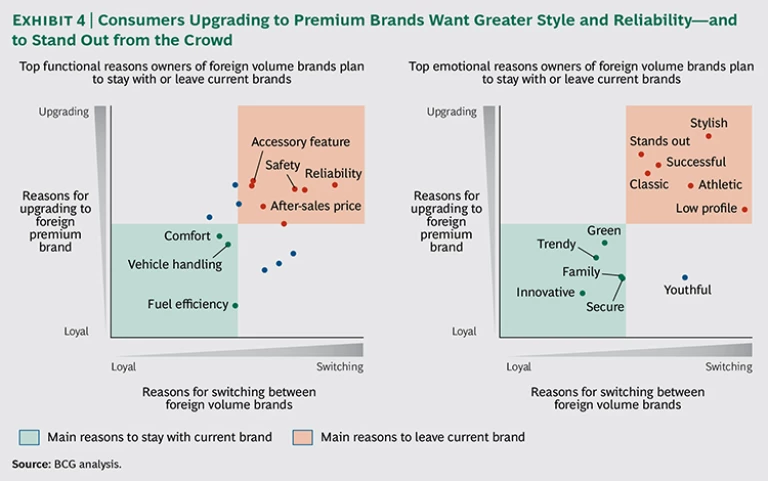

Foreign Volume Brands. Car brands in this category can expect to lose around 70 percent of their current customers. This level of brand loyalty is well below what is typical in developed economies. In the U.S., for example, the top five brands have loyalty rates of 51 to 63 percent. Forty-five percent of foreign volume brand owners surveyed in China said they will switch to other foreign volume brands, and 25 percent said they plan to trade up to a premium car.

Our research indicates that brand shifters and upgraders tend to fall into two distinct categories of volume brand owners. Those who plan to shift to another foreign volume brand tend to be younger—or want to project a young image—and focus on practical needs. In general, they are satisfied with how their vehicle functions. And by a large majority, customers believe that their current volume brands are eco-friendly.

The leading functional reasons cited by consumers planning to switch to a different foreign volume brand are concerns about reliability, safety, and high after-sales costs such as maintenance. In developed countries, by contrast, most of the major multinational brands enjoy good reputations for being safe and reliable.

These responses indicate that Chinese consumers do not take safety and reliability for granted when they purchase a leading multinational brand. As they localize production in China, some multinational joint ventures offer products based on previous generations of vehicles and may not be investing enough in quality control. They could also be using lower-quality, less-expensive materials and parts that are not holding up well under Chinese driving conditions. In terms of emotional attributes, consumers who are planning to switch to another foreign volume brand reported that they are looking for a young-looking, unpretentious style.

The upgraders seem to be focusing more on cars that convey social status and tend to be in the market for a premium brand. The top functional attributes cited by volume-brand owners who plan to upgrade were better accessory features as well as reliability. A large portion of upgraders also cited better purchasing and after-sales experiences as unmet needs. The top three emotional attributes cited by upgraders—wanting cars that make them stand out from the crowd, feel stylish, and look successful—are benefits that mainly high-end cars offer. (See Exhibit 4.) These responses suggest that China’s middle class expects to be richer and more successful in the future—and will want to drive cars that project that.

Foreign Premium Brands. Premium brands sold by multinationals and their joint ventures suffer from levels of customer loyalty that are below the levels of around 70 to 80 percent that market leaders enjoy in some developed economies. Forty-three percent of premium-car owners in China plan to stay with their current brand when they buy a new premium car, and 37 percent said they plan to buy a competing premium brand. Sixteen percent said they intend to trade up to a more expensive, super-premium car.

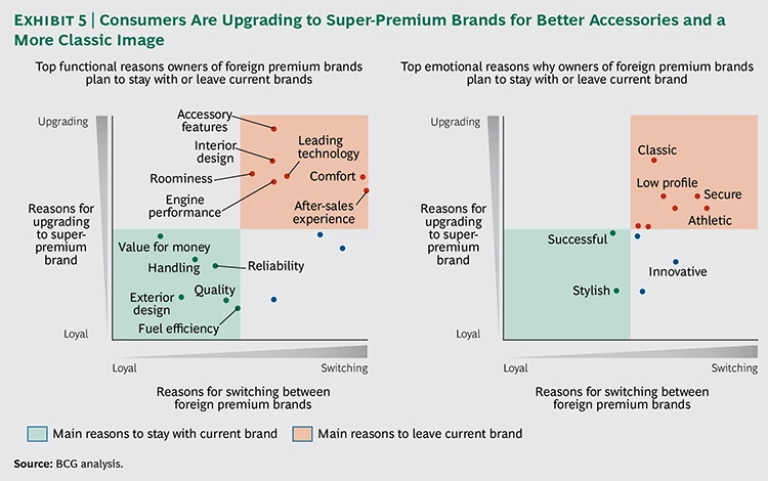

Premium-car owners who are planning to switch brands within the same basic price range said they are primarily seeking more comfort and superior after-sales services. This indicates that companies must put much greater emphasis on service than they did in the past in order to keep these customers or draw them away from competitors. Premium-car owners who plan to trade up, however, are attracted by more luxury, such as accessories, roominess, and interior design. Better comfort and engine performance also rank high among functional attributes.

The emotional attributes that resonated most strongly with premium customers who plan to switch brands include cars that seem athletic and innovative. By contrast, upgraders said that emotional attributes that reflect a more conservative image—such as classic, secure, and low profile—are the most important. (See Exhibit 5.)

One conclusion we draw from these findings is that the expectations of affluent Chinese car owners are rising. Owners of premium cars—especially those planning to upgrade—demand the quality, superior service, and exclusivity they are paying for. This suggests that there is room in the growing Chinese market for super-premium cars that fill niches for style, performance, and luxury services.

The Implications for Car Companies

The intensifying battle for customer loyalty presents different sets of marketing, design, manufacturing, and positioning challenges for manufacturers of domestic and foreign volume brands and for foreign premium brands. Much also depends on which type of consumer the company decides to target: current customers, brand shifters, or upgraders.

The increasingly winner-take-all nature of China’s competitive landscape raises the stakes even further: car buyers seem to be converging on a handful of brands that have broad, solid reputations for being safe choices. Our research found that a surprising 40 percent of owners of local Chinese car brands who plan to trade up to the foreign volume category are leaning toward a VW. Nearly 90 percent of foreign volume-brand owners who are trading up are likely to be captured by Audi, BMW, or Mercedes-Benz.

We see two probable reasons for this tendency among upgraders. One is that they are unfamiliar with offerings in the new segment and are choosing what they regard to be a “safe” brand by default. Cars are very much regarded as status symbols in China, and consumers tend to buy brands that convey success. The other reason is that car owners doubt that other brands will deliver the driving experience and image they expect.

As the Chinese market and the buying behavior of its consumers mature—and as the stakes in the battle for consumer loyalty grow larger—creating a distinctive brand identity on both the functional and emotional levels will become more critical not only in the premium segment but in all others as well. Thus far, however, most car brands in China are far from attaining that goal. Each segment needs to address some basic challenges.

Domestic Volume Brands. Having successfully established their brands, domestic Chinese carmakers must move to the next level not only to try to improve their share of China’s growing market in the face of intensifying competition but also simply to sustain it. The general challenge is to build a strong brand based on a solid foundation. This will become even more critical as domestic carmakers attempt to compete head-on with multinationals in higher-end vehicles. To succeed, domestic brands must deliver the fundamentals, such as safety, quality, and engine performance, and then capitalize on their progress through better marketing. Trying to lure drivers by offering unique accessories will not be sufficient. It is also urgent for China’s domestic brands to strengthen their dealership networks in order to improve the buying experience as well as after-sales service.

Several leading Chinese car companies have been early to recognize that winning customer loyalty is not only a challenge but also an opportunity. And they have begun to make clear moves to improve quality and safety.

BYD Auto is one company that is tackling the challenge directly. The Chinese automaker’s F5 Surui family sedan—sold overseas under the nameplate Suri—recently received a five-star safety rating from the China New Car Assessment Program. BYD’s score of 56.5 in crash tests set a record for Chinese brands and outperformed the vehicles of several multinational brands. This represented a major improvement from the three-star rating and score of 34 that BYD’s F3 received five years ago.

Another Chinese automaker that is focusing on quality improvement is Qoros Automotive, a joint venture between Chery Automobile and Israel Corporation. The company’s new Qoros 3 sedan received a five-star rating in safety tests by the European New Car Assessment Program, the first Chinese model to do so.

For many Chinese automakers, building a brand based on safety and reliability will require transformational change and will take time. What’s more, they will have to make those improvements while controlling costs tightly to keep their prices competitive. But there is little alternative.

Foreign Volume Brands. To earn customer loyalty in China, multinational car companies face an apparent marketing conundrum: should they focus on current core customers who want to replace their cars with another foreign volume-brand vehicle? Or should their marketing strategies target owners of domestic volume brands who intend to trade up?

Automakers cannot use the same strategy to win over each of these customer types. As explained above, the emotional attributes desired by brand shifters and upgraders are seemingly incompatible: brand shifters want to keep a low profile; upgraders want to stand out. Emotional preferences also differ by age. More mature buyers want to convey a stylish and successful image, whereas younger buyers prefer more family-friendly cars. Brand shifters and upgraders are basically aligned when it comes to functional desires, however. Reliability and safety are key to both, and differences between the age groups are modest.

One possible approach to resolve this tension is to build different brands to address the needs of different target segments. Nissan, for example, has established Venucia, a separate brand, aimed at the lower end of the Chinese volume market. There are serious considerations when launching a new brand, of course. One is cost. Others are the risk that the not-yet-established brand won’t be accepted by upgraders and that a conflict will be created within the company’s existing customer base, which could undermine the core brand. It is important, therefore, to manage this tension as well as cross-brand migration.

Because there is wide agreement on the functional benefits that volume car buyers want, companies can share platforms and components across brands. That will free them up to focus on the emotional attributes that customers want—and to build unique brands that appeal to different consumer segments.

Currently, foreign volume brands are not well differentiated in China. In our research, few brands stand out in the eyes of consumers when it comes to how their cars make them feel. Toyota is an exception. Thanks in large part to Toyota’s success with hybrid, fuel-efficient technologies, Chinese car owners give the brand especially high marks for being “green” and trendy.

The Volkswagen Group illustrates a path to win—and keep—different types of Chinese consumers as they migrate. VW is China’s market leader in volume cars, with more than 2 million units sold per year, as well as in the premium segment, where its Audi brand sells close to 500,000 units annually. VW enjoys an intended loyalty rate of 42 percent in China, significantly higher than the average loyalty rate of 29 percent for multinational brands.

The first reason for this intended loyalty is that VW has long been regarded as one of the safest and most reliable automotive brands in China, a reputation it has nurtured since 1984, when it became the first foreign brand to enter the market. VW uses the same platforms and technologies across its brands, and its marketing activities reinforce its image of safety and reliability.

VW’s Audi brand has managed to appeal to upgraders who want to convey success. Audi has a significant history of leadership in the government procurement market, where it had long been the sedan of choice for Chinese officials. This associated Audi with success in the minds of consumers. Our research shows that Audi is essentially the default choice for Chinese upgraders. More than one-third of foreign volume-brand owners who said they want to upgrade said they plan to buy an Audi. Our research also indicates that VW manages brand migration within its group better than most other car companies in China.

Foreign Premium Brands. The profiles of premium brands are also not well differentiated in China. That is in sharp contrast with their reputations in developed economies, where affluent drivers have a clear idea of what distinguishes, say, a BMW from a Mercedes-Benz.

Overall, Chinese drivers who upgrade from a foreign volume brand overwhelmingly gravitate toward only three brands that make them feel like winners: Audi, BMW, and Mercedes-Benz—all of which, according to our research, stand for success among Chinese upgraders. Unless other brands can crack this short list, they risk being marginalized in China’s winner-take-all market.

Premium brands enjoy higher customer loyalty in China than volume brands do. But there is still a lot of room for improvement, such as in the way companies manage the migration of customers to their internal brands. Our research shows that customers place a high priority on the ownership experience. Premium brands should also make sure that their customers feel they are getting what they pay for. Affluent Chinese are willing to pay premium prices, but they expect luxury and superior service in return.

Our research highlighted several other trends that are critical for foreign premium brands. One is the emergence of the super-premium segment. As premium-brand owners grow wealthier and gain experience, they typically feel less need to show off their social status through the car they drive and instead want something more personalized. We see growing demand for distinctive luxury vehicles, such as Porsche and Land Rover, that fit in certain niches. Another trend is emerging among young, affluent buyers, some of whom are focusing less on standing out and are more interested in keeping a low profile. This could mean greater opportunities for brands other than Audi, BMW, and Mercedes-Benz.

Responding to the needs of some customers, several premium brands are trying to lure upgraders by going down-market and offering small, less expensive “near premium” cars. But this is a difficult and risky strategy. For one, there is the danger of overstretching the brand and losing acceptance at the high end of the market. In addition, the market for near-premium cars is relatively small and highly competitive. High-end foreign volume brands, such as Buick and higher-end Toyotas, battle with the lower level of the premium segment, which includes Volvo, Cadillac, Lexus, and Lincoln, for essentially the same customers.

BMW illustrates how products and marketing strategies that are well aligned with the desires of affluent Chinese can be rewarded with higher customer loyalty. BMW has enjoyed a reputation for athletic design and superior service ever since it started exporting vehicles to China in the early 1990s. The handling of BMW’s 3- and 5-series cars, which have powerful, smooth-running engines, also makes the brand more appealing in China. BMW customized these models for the Chinese market by making changes such as increasing the wheelbase. Our research also shows that BMW is regarded as more athletic and innovative than its major competitors. Its marketing messages reinforce the image that driving a BMW is fun. For all these reasons, BMW has become China’s fastest-growing premium brand, with sales increasing by more than 40 percent annually from 2009 through 2013.

As China’s auto boom slows, the time is drawing to a close for automakers to enjoy rapid growth by marketing traditional styles and technologies and relying on brand names. The winners in China’s intensifying battle for consumer loyalty will be car companies that are best able to meet the increasingly demanding expectations of Chinese consumers. Domestic and multinational brands will need to build better capabilities and stronger, more clearly differentiated brands.

One place to start is to better understand the needs of target customers. Another is to conduct objective “health checks” to assess how well brands are satisfying those needs. Companies that want to win should gain a clearer picture of which functional and emotional qualities drive the decisions of different segments of the Chinese auto market. These desires clearly go beyond the product itself. The purchase and ownership experiences are increasingly important.

Companies should understand how well their brands are positioned with regard to their competitors in terms of the most important functional and emotional attributes. What are their brands’ strengths? Where exactly do they fall short? These regular health checks should also assess whether brand awareness of potential automotive customers is high enough to meet sales goals in China—and how well that awareness is being converted into actual sales.

Based on these findings, companies need to develop a strategy to sustain and improve their brand equity in China. In most cases, they must enhance the attractiveness of their offerings by improving their product’s design and boosting the quality of their cars, customer experience at dealerships, and after-sales service. Some companies may also need to make their pricing more competitive.

At the same time, most carmakers must adjust their marketing approach in China. They must ensure that their dealership networks are sufficiently dense in key markets and that they are staffed by professional, well-trained personnel. To increase consumer familiarity with their brands, most companies need to adjust and potentially increase their investments in broadcast and online advertising. To convert prospective customers into sales and improve the loyalty of existing customers, carmakers must upgrade the quality and scale of their customer-relationship-management programs.

The priorities vary by market segment. The most urgent challenge domestic volume brands face is to continue improving their vehicles to bridge the quality and performance gap with multinationals and to professionalize dealership networks. But they must do so without losing their cost advantage. They must also make sure that this progress translates into a stronger brand reputation through smart marketing. Those who cannot make the next leap are at risk of losing out in what is likely to be a brutal shakeout of China’s domestic car industry. The winners will secure the opportunity to not only seize clear leadership in China but also attain the scale to improve their global competitiveness.

Most foreign volume brands are facing a challenge as Chinese car buyers pay less attention to famous foreign names and more attention to substance. Foreign volume brands must anticipate and meet consumers’ higher expectations for quality in order to defend their market positions against competition from premium prices at the low end of the foreign volume market as well as from domestic brands. It is also important for carmakers to persuade their current customers to migrate to other brands that they control—urging them to move from Chevrolet to Buick, for example. By offering options such as service packages, used-vehicle trade-in programs, and leases, carmakers can increase the financial attractiveness of switching brands within a group instead of leaving the group.

As the Chinese market changes, foreign volume brands must also make it a priority to offer attractive, alternative products—such as small SUVs and other vehicles with different body styles—to young Chinese buyers.

Foreign premium car brands must upgrade their sales and ownership experiences, which our research indicates Chinese customers will value more and more. Establishing distinct brand profiles—in both functional and emotional attributes—will also become more critical. Premium brands should consider marketing programs that can help develop a customer community, such as driver training and adventure trips, which ultimately help increase brand loyalty.

Although such an agenda will likely take years to complete, car companies hoping to succeed in the next phase of growth have little option but to adapt to the new environment. The nature of China’s automotive market suggests that the costs of failure in the looming battle for customer loyalty are likely to be steep. But the rewards for companies that win and hold the loyalty of Chinese car owners as they mature and migrate up to higher-end vehicles could be enormous.

Acknowledgments

This report would not have been possible without the efforts of our BCG colleagues Jun Chen, Belinda Gallaugher, Marion Gasperment, Tobias Glas, Mary Leonard, Leanne Lewin, Xavier Mosquet, and Alfred Xu.