The fundamental economics of the global life insurance industry are broken, with distribution consuming an increasing share of the industry’s total economic value, particularly compared with customers’ declining share. After decades of limited innovation, traditional distribution is on the cusp of meaningful change—especially in the agency channel—which will unlock benefits for all stakeholders. This is the conclusion of a joint BCG/Morgan Stanley report, Reinventing Life Insurance Agency Distribution Globally.

Of course, transformational change is not so easy to accomplish. Agents have historically been resistant to change, significant amounts of technology and innovation are required, and some carriers still struggle to separate the performance of new business from that of the in-force book. Even so, we believe the time to act is now. Human-to-human interaction will remain key to insurance distribution, but the role of agents will change as the use of data and predictive analytics grows, customer behaviors evolve (with the use of mobile devices and social media, for example), regulations continue to change, digital players from adjacent industries look to disrupt the insurance industry, and traditional competitive pressures continue to increase.

Human-to-human interaction will remain key to insurance distribution, but the role of agents will change.

The BCG/Morgan Stanley report looks at the future of human-to-human life insurance distribution globally. It draws on more than 50 interviews with senior insurance executives; a survey of 850 agents in China, India, Germany, and the US; and detailed proprietary financial modeling of the interaction among the in-force book of business, new business, and agency economics. It concludes that there is significant value at stake for insurers that successfully manage to reinvigorate the agency, revamp solutions, drive efficiencies, and address the in-force book of business. Moreover, carriers in China offer important lessons for carriers in developed markets, particularly how to drive efficiencies with technology adoption.

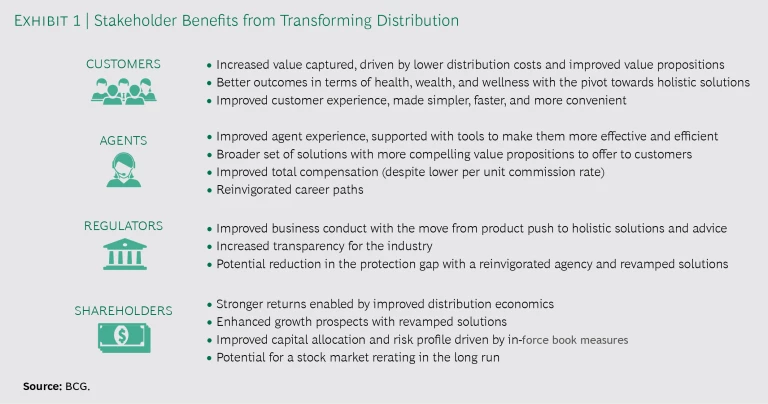

All stakeholders stand to benefit from transforming distribution—even the agents themselves.

The Four Foundational Elements of Transformation

Carriers should identify, design, and implement a set of holistic initiatives based on the four foundational levers of transformation. Depending on the carrier’s starting point and ambition, it is quite possible to lower acquisition costs by 10% to 20%, reduce administration costs by 20% to 30%, and deploy capital more efficiently. Indeed, all stakeholders stand to benefit from transforming distribution—even the agents themselves. (See Exhibit 1.)

Reinvigorate the agency. The term “agency” is used broadly to include any form of human-to-human distribution. Insurers need to start by improving agent “life cycle” management: recruiting, onboarding, and retaining agents to create a more vibrant and productive channel. In many locations, the agency force is aging and the industry is finding it difficult to recruit the next generation of talent. For example, in the US, the average age of agents is 56, according to LIMRA, and recruiting the next generation has proved challenging; only 4% of millennials are interested in a career in insurance.

Insurers need to segment their agents based on performance and build a more nimble support function to help them maximize their potential. For example, the top-performing segment can be an excellent testing ground for support services that carriers might roll out to the wider agent population.

Finally, individual agent compensation should increase to motivate existing high performers and attract new talent. However, any increase should depend on improved productivity—that is, the sale of more policies—in order to lower per unit sales compensation.

Revamp solutions. Historically, many insurers considered their primary customers to be their agents. This has resulted in products that are overly complex, do not resonate with customers, and reinforce the adage that life insurance is “sold not bought.” It’s time to design simpler and more customer-centric solutions and ensure that the average customer understands how these products can address their needs.

Agents need to move from “pushing products” towards “providing holistic solutions.” This will require more training and a focus on creating new offerings that address evolving needs around health, wealth, and wellness. This approach could help counter many consumers’ distrust of the life insurance industry. According to LIMRA, 36% of consumers rate the honesty and ethical standards of the insurance salesperson as low or very low.

Drive efficiencies. To raise productivity, insurers should invest in building digital and advanced analytic capabilities that can provide agents with qualified leads with a high propensity to buy and qualify for coverage. Moreover, by applying these tools to the in-force book, carriers can identify many leads (for example, buy-up options) that are often untapped today. With their deep resources, carriers are in a better position than other distribution partners to invest in these capabilities. For example, carriers in China have made significant per agent productivity gains thanks to their transition to a digitally delivered, analytics-enabled, end-to-end experience.

Automation and artificial intelligence will be critical to driving efficiencies and making the underwriting process simpler, faster, and less invasive, thus reducing overall costs (such as those associated with medical exams). For example, straight-through processing can modernize, streamline, and automate front-, middle-, and back-office processes. Proven tools such as e-application, e-delivery, and case tracking can reduce acquisition and administrative expenses while improving the customer and advisor experience.

Address the in-force book of business. Investors and insurance executives must isolate the economics of the in-force book, new business, and distribution to determine where value is being created or destroyed. Too often, they find unwelcome surprises, such as new business being written at a loss in order to sustain the in-force book and distribution structures. This is mostly a problem in mature markets, where carriers often struggle with capital intensive/low-return in-force books.

Going forward, it is critical to evaluate a broad range of strategic options, including whether to maintain the in-force books open to new business, place the business into runoff, divest underperforming books, or acquire books and become an aggregator to drive scale.

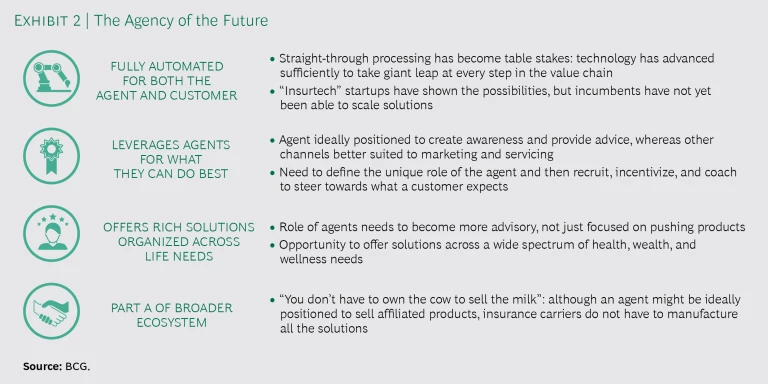

The Agency of the Future

The pace of change will accelerate. Some insurers are already making bold distribution moves, and that is important because digital players from adjacent industries are looking for disruptive opportunities, perhaps as part of a broader health, wealth, and wellness planning and advisory offering.

Although there is no one-size-fits-all formula for success, the agency of the future will likely be fully automated, will provide agents with qualified leads and other digital and analytic capabilities to boost their productivity, and will address customer needs more holistically, with richer solutions across their lifetimes. (See Exhibit 2.)

Despite all these necessary changes in insurance distribution, human-to-human interaction will remain vital. Direct digital sales will mostly involve simpler products, such as term insurance, unit-linked (variable) savings contracts, and personal lines of insurance. Given the complex nature of many life insurance products and the emotional component often involved, human interaction and distribution will retain their value and importance.

Inefficiencies in distribution are a drain on the entire insurance ecosystem and are not sustainable. While some carriers have begun to experiment with new products, accelerate underwriting, and digitize the middle and back offices, there’s been no transformational change in distribution and no one company has emerged as a clear leader. Insurers that approach the problem holistically, looking for ways to reinvigorate the agency, revamp solutions, drive efficiencies, and address their in-force books will unlock significant value.

For more information on India, please contact Pranay Mehrotra, partner and managing director in the Mumbai office, at mehrotra.pranay@bcg.com.

For more information on Germany, please contact Walter Reinl, partner and managing director in the Zurich office, at reinl.walter@bcg.com.

For more information on China, please contact Tjun Tang, partner and managing director in the Hong Kong office, at tang.tjun@bcg.com.

For more information on the US, please contact one of the authors below.