The German Federal Government has announced an ambitious national contribution to the effort to combat climate change: In conjunction with the European Union's climate targets, it has set the goal of reducing greenhouse gas emissions (GHG) in Germany by 80 to 95 percent by 2050 compared to 1990 levels. Achieving this objective represents a long-term political, economic, and social project of enormous proportions.

THE STUDY IS THE RESULT OF A COMPREHENSIVE PROCESS WITH THE GERMAN INDUSTRY

Against this backdrop, the study "Climate Paths for Germany" shows economically cost-efficient strategies for successful 80 to 95 percent GHG reduction by 2050. The study was compiled over the course of the year 2017, with close to 70 companies and associations as well as a board of renowned economists involved in more than 40 workshops. Both the degree of validation and the depth of the study, spread over 270 pages of detailed facts, are unmatched in Germany.

The main findings of the study are summarized below.

- Continuing current efforts in the form of existing measures, the political and regulatory framework conditions already agreed, as well as foreseeable technological developments ("current policies path"), will achieve an approximately 61 percent reduction in greenhouse gas emissions (GHG) compared to 1990 by the year 2050. This leaves a gap of 19 to 34 percentage points to the German climate targets.

- 80 percent GHG reduction are technically feasible and macroeconomically viable in the considered scenarios. However, implementation would require significantly stepping up existing efforts, more decisive political steering and, without a consensus on global climate protection, effective carbon leakage protection.

- 95 percent GHG reduction would push the boundaries of foreseeable technical feasibility and current social acceptance. Such a reduction (three quarters more than the 80% path) requires practically zero emissions for most sectors of the German economy. In addition to more or less phasing out all fossil fuels

1 1 Solid, liquid, and gaseous energy carriers are generally referred to below as combustibles. Liquid and gaseous fuels used in the transport sector are referred to below as fuels. , this would for example mean importing renewable fuels (power-to-liquid/gas), the selective use of currently unpopular technologies such as carbon capture and storage (CCS), and even reducing emissions from livestock. Successful implementation seems only imaginable if most other countries pursue similarly high ambitions. - Several game changers could still reduce required efforts and costs of achieving the climate goals in the coming decades, including technologies for the "hydrogen economy" and for carbon capture and utilization. These game-changers will not be ready for use in the foreseeable future and have therefore not been considered for this effort. Nevertheless, research and development in these areas should be made a priority.

- Cost-effective attainment of the climate paths, from today’s perspective and compared against a scenario without additional focus on emission reductions, would require an overall additional investment of €1.5 trillion to 2.3 trillion by 2050, including about €530 billion to continue existing efforts in the current policies path. This corresponds to average additional annual investments of around 1.2 to 1.8 percent of Germany’s gross domestic product (GDP) through 2050. The additional direct costs after deduction of energy savings would amount to around €470 billion to 960 billion by 2050 (roughly €15 billion to 30 billion per year). Thereof, approximately €240 billion would need to be spent on existing efforts.

2 2 Additional investments include all extra investments for realizing the climate paths over and above the investments made in the current policies scenario. In order to calculate the additional costs, these were annualized at a national real interest rate of 2 percent over the life of the respective capital asset. Energy cost savings and expenses were offset. To this end, cross-border prices of fossil fuels and electricity system costs were applied. Moreover, the additional investments and costs for non-economic measures in the current policies scenario were roughly estimated. - Assuming optimal political implementation, the climate paths’ macroeconomic effects would nonetheless be neutral to slightly positive, for an 80 percent ambition even without global consensus. However, a unilateral effort would require greater efforts to protect vulnerable industries—in the form of effective carbon leakage protection and long-term, reliable compensation arrangements for industries facing international competition.

- Successful efforts to tackle climate change would trigger extensive modernization activities in all sectors of the German economy and could furthermore open up opportunities to German exporters in growing "clean technology” markets. Studies suggest that the global market volume of key climate technologies will grow to €1 trillion to 2 trillion per year by 2030. German companies can solidify their technological position in this global growth market.

- At the same time, the imminent transformation process presents Germany with significant implementation challenges. The considered climate paths are economically cost-efficient and are based on the assumption of ideal implementation, meaning optimization across sectors and "right decisions being made at the right time." Mismanaging the implementation (think of excessive feed in-tariffs and delayed grid expansion in case of Germany’s “Energiewende”) could considerably increase costs and risks or even render the goal unattainable.

- On its own, Germany's share of global GHG emissions (a little more than 2 percent) is too small to significantly impact the climate. Comprehensive climate protection efforts in Germany are therefore only successful if they motivate other countries to follow suit. On the other hand, they could become counterproductive if a strong negative impact on the economy discouraged other states. A similarly ambitious implementation process by at least the largest economies (G20) would significantly reduce these risks and also open up greater export opportunities for German companies.

- Successfully achieving Germany's climate goals and a positive international multiplier effect therefore requires significant efforts on all fronts—politically, socially, and economically. It needs a long-term, holistic climate, industrial, and social policy that focuses on competition and cost efficiency, distributes the social burden fairly, ensures acceptance of the measures, and prioritizes the preservation and expansion of industrial value creation. The “centenary project” of mitigating Germany’s national contributions to climate change therefore calls for long-term political support

The ten main results are summarized below and described in detailed in the following chapters.

61 PERCENT GHG EMISSION REDUCTION UNDER THE CURRENT POLICIES PATH

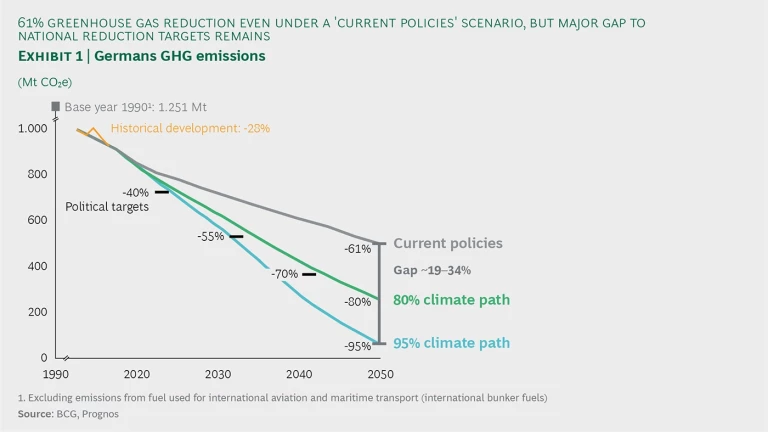

1. Continuing current efforts in the form of existing measures, the political and regulatory framework conditions already agreed, as well as foreseeable technological developments ("current policies path"), will achieve an approximately 61 percent reduction in greenhouse gas emissions (GHG) compared to 1990 by the year 2050. This leaves a gap of 19 to 34 percentage points to the German climate targets.

- Comprehensive efforts to bring down emissions have already been undertaken in the past: In the year 2015, Germany's national GHG emissions were 28 percent lower than in 1990. Only part of this decline can be traced back to the effects of reunification

- Emissions will be cut further over the next 35 years. Under a current policies path, Germany's national emissions will decline by approximately 61 percent by 2050 compared to 1990. This leaves a significant gap of approximately 19 to 34 percentage points to the government goals of 80 to 95 percent GHG reduction. The emissions remaining in 2050 under this scenario thus still amount to approximately two to eight times the targeted "residual quantities" (20 percent or 5 percent compared to 1990).

- In the building sector, steady modernization efforts and continued implementation of efficient building standards, combined with a steady expansion of renewable technologies for heat generation, will reduce emissions by about 70 percent until 2050 (compared to 1990).

- Further restructuring of the power system, including extensive expansion of renewable energies and a partial phase-out of coal-fired power generation, will result in more than 70 percent emission reductions in the energy sector.

- Gradual efficiency gains in the industrial sector continue to reduce emissions, although this reduction will be partly offset by 1.2 percent annual economic growth until 2050. As a result, energy- and process-related GHG emissions decline by about 48 percent compared to 1990 (22 percent compared to 2015). To avoid emission reductions caused from shifting traditionally emission-intensive industries abroad, this study assumes a comprehensive carbon leakage protection scheme. To be precise, it is assumed that the industry is protected from any direct and indirect CO2-related costs from the EU Emissions Trading System (EU ETS) beyond the current level.

As a consequence of significantly increased traffic volumes since 1990, emissions in the transportation sector stayed approximately at the same level. Increasing penetration of more efficient vehicles3 3 And other means of transport (e.g., in aviation). and foreseeable electrification will reduce emissions in the current policies path by approximately 40 percent until 2050—despite continuously increasing heavy goods traffic. - The measures under the current policy scenario will require additional investments of around €530 billion by 2050 (additional costs after deduction of energy savings: €240 billion). These include costs for a further expansion of renewable generation and grids in the electricity sector, non-economic measures to comply with fleet emission limits in passenger road transportation, and individual non-economic measures to modernize Germany’s building stock.

80 PERCENT GHG REDUCTION ARE TECHNICALLY FEASIBLE AND ECONOMICALLY VIABLE

2. 80 percent GHG reduction are technically feasible and economically viable in the considered scenarios. However, implementation would require significantly stepping up existing efforts, more decisive political steering and, without a consensus on global climate protection, effective carbon leakage protection.

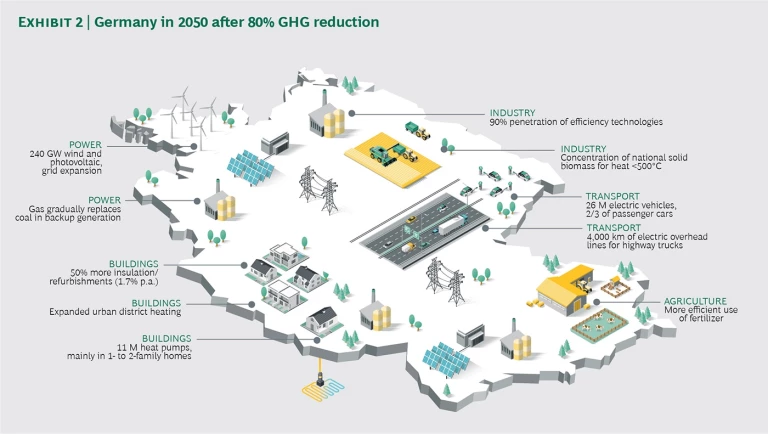

- Speeding up sector coupling while reducing emissions in the electricity system facilitates significant GHG savings particularly in transport and buildings; for example, through about 26 million electric cars

4 4 For the purposes of this study this includes battery electric passenger cars, plug-in hybrids, and fuel-cell passenger cars. and 14 million heat pumps5 5 In order to achieve the required penetration in existing buildings as well, current refurbishment activities need to be intensified—with an average refurbishment rate of 1.7 instead of 1.1 percent. by 2050. - At the same time, several sectors can better exploit existing energy savings potentials by ensuring greater penetration of efficiency technologies. As a result, total net electricity demand in the 80% path increases by only 3 percent.

- Almost 90 percent of the current electricity demand can be supplied from renewable sources by 2050. This requires accelerating the energy transition through an additional annual deployment of approximately one gigawatt of renewable generation capacity (to 4.7 GW of net capacity per year). Until 2050, gas-fired power plants would gradually take over the role of flexible "backup" from coal.

- The integration of increasing volumes of intermittent generation from wind and solar PV requires more flexibility in the power system. This requires more storage capacity, but also flexible consumption behavior of new electricity consumers, such as electric cars and heat pumps. As long as these are available, the economic potential for producing renewable synthetic fuels from "surplus electricity" (power-to-X applications) is limited.

- Nationally available sustainable biomass

6 6 Predominantly existing and some previously unused solids, no imports or reclassification of agricultural land. should be used primarily in the industrial sector, where it can replace coal and gas in industrial low- and medium-temperature heat generation. - The macroeconomic effects seem affordable for Germany in the considered scenario (about €15 billion average additional costs per year, plus 0.4 to 0.9 percent effect on 2050 GDP). However, the transformation process involved requires prudent government guidance, and individual industries will still face considerable challenges.

95 PERCENT GHG REDUCTION WOULD PUSH THE BOUNDARIES OF TECHNICAL FEASIBILITY AND CURRENT SOCIAL ACCEPTANCE

3. 95 percent GHG reduction would push the boundaries of foreseeable technical feasibility and current social acceptance. Such a reduction (three quarters more than the 80% path) requires practically zero emissions for most sectors of the German economy. In addition to more or less phasing out all fossil fuels, this would for example mean importing renewable fuels (power-to-liquid/gas), the selective use of currently unpopular technologies such as carbon capture and storage (CCS), and even reducing emissions from livestock. Successful implementation seems only imaginable if most other countries pursue similarly high ambitions.

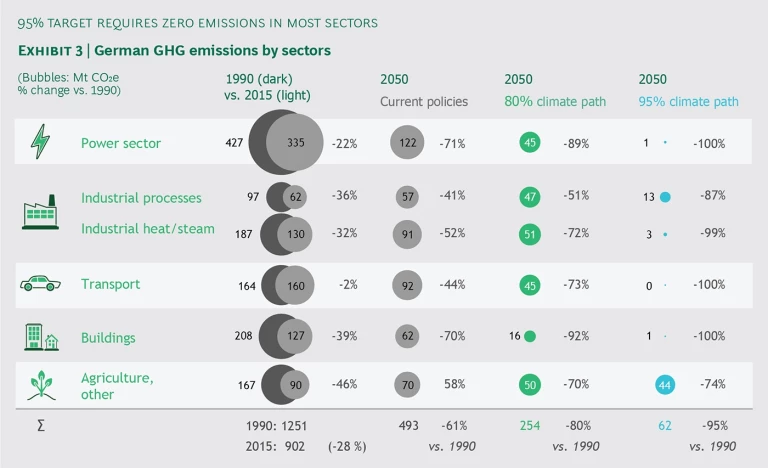

- An emissions reduction of 95 percent compared to 1990 requires virtually zero emissions in energy, transport, buildings, and industrial heat generation, as residual emissions persist in other sectors—especially in agriculture.

- Zero emissions in the power system would be possible if previously fossil-fueled, flexible backup generation were powered 100 percent with Power-to-Gas (PtG). The gas grid would turn into a seasonal renewable energy storage.

- Heat production in the industrial sector could be "de-fossilized" to a large extent by using nationally available biomass and biogas. This would furthermore incur an additional system benefit, since the emitted non-fossil carbon could be used for the production of Power-to-Gas through carbon capture and utilization technology.

- Almost 80 percent of the 2015 building stock would have to be renovated by 2050, and on average consume as little heat as a new building does today. In parallel, fossil fuels would have to be completely phased out from space heating and warm water generation—replaced primarily by heat pumps and emission-free district heating.

- Road traffic would have to be electrified to an even greater extent—through battery vehicles for passenger transport and light commercial vehicles as well as, for example, electric overhead lines for trucks on all major highways. At the same time, road traffic would need to shift towards more energy-efficient modes of transport (rail, bus, inland waterways). Finally, full avoidance of fossil emissions in aviation, shipping, heavy goods, and passenger transport would require the use of renewable fuels (Power-to-Liquid/Gas).

- A significant share of these fuels would need to be imported from countries with more favorable renewable energy conditions. Nevertheless, energy imports

7 7 Based on energy content. until 2050 would decline by almost 80 percent compared to 1990 levels. - The total required net electricity generation of 715 TWh (2015: 610 TWh) can still be fully covered by domestic renewables.

8 8 The expansion potential of renewable energies is subject to technical, ecological, economic, and acceptance-related restrictions. The present study assumes that the potential for electricity generation from renewable energies in Germany is limited to between 800 and 1,000 TWh per year. A more comprehensive electrification of all sectors would not only be very expensive, but could soon double the annual power generation required. Given the geographic limitations for installing renewable generation in Germany, this would currently not be considered realistic. - As long as possible alternatives do not become significantly cheaper, Carbon-Capture-and-Storage (CCS) technology would be required to eliminate process emissions in steel and cement production, steam reforming, as well as emissions from remaining refineries and waste incineration plants. To achieve this, serious acceptance issues would need to be overcome.

- Finally, fully meeting the 95 percent reduction target would require a reduction in emissions from agricultural livestock (approximately 30 percent compared to current figures). This could for example be achieved through methane-emission-inhibiting feed additives ("the methane pill").

9 9 Currently conceivable alternatives would only increase the carbon-absorbing properties of agricultural soils which, according to the United Nations Framework Convention on Climate Change, would not realize the targets (LULUCF), as well as the separation of biogenic emissions from biomass incineration (CCS with negative emissions), although feasibility for the scope required is unclear at the very least. - After implementing all these measures, agriculture would account for almost 70 percent of the remaining 5 percent of emissions. The rest would come mainly from residual emissions in industrial processes and waste management.

- Overall, such a path would imply significantly larger challenges for all sectors (e.g., Power-to-Gas, renewable synthetic fuels), require overcoming current public acceptance hurdles (e.g., CCS, heavy grid expansion, "methane pill") and require extensive government support and navigation. Therefore, and given the high levels of additional investment required especially in today's emission-intensive industries, this 95 percent path only appears feasible if other major economies pursue similarly ambitious reduction goals.

TECHNOLOGICAL “GAME-CHANGERS“ COULD STILL REDUCE EFFORTS AND COSTS OF ACHIEVING THE CLIMATE GOALS

4. Several game changers could still reduce required efforts and costs of achieving the climate goals in the coming decades, including technologies for the "hydrogen economy" and for carbon capture and utilization. These game-changers will not be ready for use in the foreseeable future and have therefore not been considered for this effort. Nevertheless, research and development in these areas should be made a priority.

- A radically steeper learning curve in photovoltaics ("third generation") and electrochemical or alternative storage technologies would make cheaper electricity much more widely available and could enable more widespread electrification in transport (e.g., battery trucks).

- More efficient production and better solutions for the transport and storage of hydrogen as well as more efficient Power-to-X processes could widen the technology space for replacing fossil carbon in many sectors.

- In the industrial sector, cheaper Carbon-Capture-and-Utilization (CCU) methods could facilitate closed carbon cycles.

- Last but not least, new technologies around carbon bonding and sequestration could help to replace non-sustainable CCS applications in the longer term.

- As these game changers are not sufficiently mature, they have not been included in the climate paths. Nonetheless, research in these areas should be of high priority.

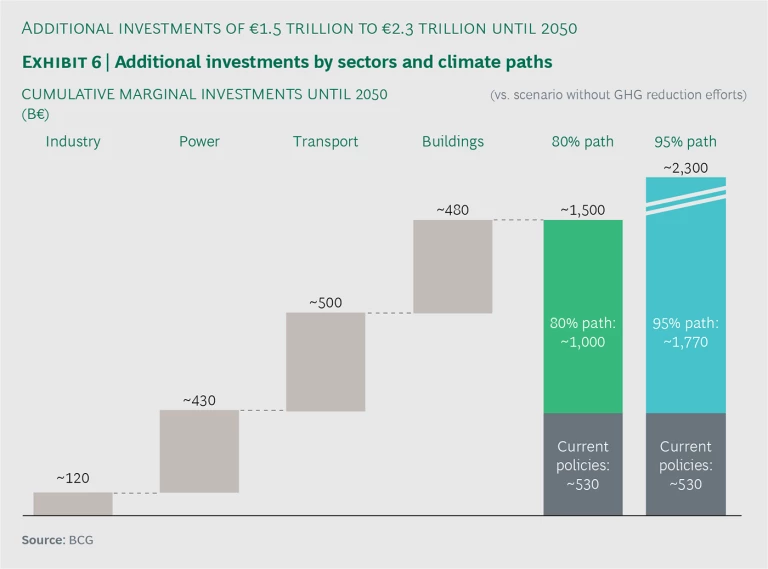

ADDITIONAL INVESTMENTS OF €1.5 TRILLION TO €2.3 TRILLION TO ATTAIN CLIMATE PATHS

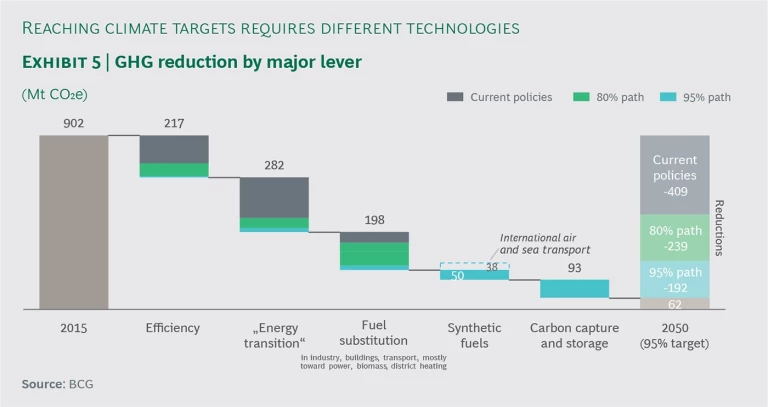

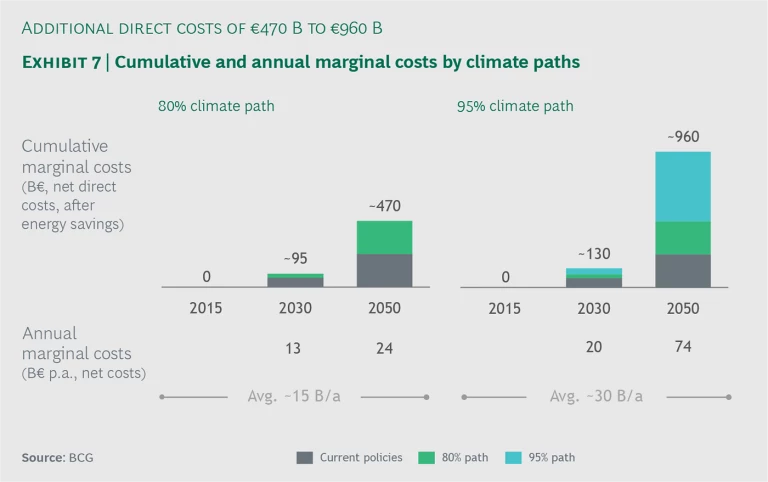

5. Cost-effective attainment of the climate paths, from today’s perspective and compared against a scenario without additional focus on emission reductions, would require an overall additional investment of €1.5 trillion to 2.3 trillion by 2050, including about €530 billion to continue existing efforts in the current policies path. This corresponds to average additional annual investments of around 1.2 to 1.8 percent of Germany’s gross domestic product (GDP) through 2050. The additional direct costs after deduction of energy savings would amount to around €470 billion to 960 billion by 2050 (roughly €15 billion to 30 billion per year). Thereof, approximately €240 billion would need to be spent on existing efforts.

- Four fifths of emission reductions in the modelled 80% path are delivered by technical measures which result in positive direct macroeconomic abatement costs. This also applies to all additional measures for the 95% climate path.

- Overall, the optimal implementation of the 80% path will require additional investments of approximately €970 billion compared to the current policies path. Another €800 billion would be needed to execute the 95% climate path, of which some €180 billion would be needed for synthetic fuel plants in other countries. Additionally, the current policies path already requires an estimated €530 billion. Total additional investments thus amount to about €1.5 trillion to 2.3 trillion—the equivalent of around 1.2 to 1.8 percent of the annual German gross domestic product.

- Many of these investments are at least partly counterbalanced by energy cost savings. Assuming optimal implementation, the resulting additional direct macroeconomic costs of the 80% and 95% climate paths amount to €230 billion to €720 billion by 2050 across all sectors. In addition, costs for non-economic measures in the current policy path amount to approximately €240 billion. Overall additional direct costs therefore total €470 billion to 960 billion by 2050—on average around €15 billion to 30 billion per year.

- The illustrated investment and cost levels are based on current conservative technology cost curves. Faster cost reductions and additional innovations, such as higher efficiency gains from Industry 4.0 and digitalization, could still bring these down going forward.

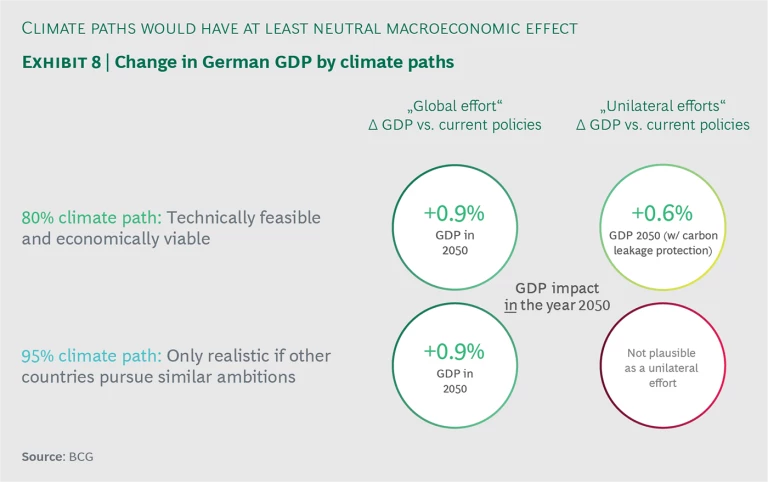

CLIMATE PATHS HAVE NEUTRAL TO SLIGHTLY POSITIVE GDP IMPACT

6. Assuming optimal political implementation, the climate paths’ macroeconomic effects would nonetheless be neutral to slightly positive, for an 80% ambition even without global consensus. However, a unilateral effort would require greater efforts to protect vulnerable industries—in the form of effective carbon leakage protection and long-term, reliable compensation arrangements policies for industries facing international competition.

- Assuming global cooperation on climate change mitigation and a level playing field, all the climate paths considered result in low but generally positive effects on the gross domestic product (plus 0.9 percent in 2050).

- The 80% climate path would even have a slightly positive to neutral GDP impact in case of a unilateral German emission reduction effort, assuming optimal implementation.

- One key driver of this effect is the sharp decline in energy imports. Between today and 2050, fossil fuel imports decline by more than 70 percent in the 80% climate path and by 85 percent in the 95% climate path.

10 10 In terms of energy content. In the 95% climate path imports will still be needed for producing chemicals and plastics. - Most industries benefit from increasing national value creation, for example construction, electronics, parts of the energy sector, or mechanical and plant engineering.

- At the same time, individual sectors and companies may face significant commercial risks despite an overall positive macroeconomic impact. These risks are greater the more they are exposed to international competition.

- To mitigate the risk of a gradual exodus of energy- and currently emission-intensive industries and to prevent a breakup of national value creation networks, effective political carbon leakage protection should be implemented in case Germany pursues an ambitious emission reduction agenda unilaterally. Depending on other countries’ parallel efforts, this may require establishing more extensive compensation arrangements than in the past.

OPPORTUNITIES FROM MODERNIZATION OF THE GERMAN ECONOMY AND FROM GLOBALLY GROWING "CLEAN TECHNOLOGY" MARKETS

7. Successful efforts to tackle climate change would trigger extensive modernization activities in all sectors of the German economy and could furthermore open up opportunities to German exporters in growing "clean technology” markets. Studies suggest that the global market volume of key climate technologies will grow to €1 trillion to 2 trillion per year by 2030. German companies can solidify their technological position in this global growth market.

- Such a comprehensive national investment program will present Germany with the chance to become a lead market for innovative, resource-efficient technologies—as well as for digital solutions and system know-how.

- Demand for these technologies has also been growing globally. Third-party studies indicate a global market potential of €1 trillion to €2 trillion per year by 2030.

- In many segments, the "race" for global market leadership is still on—and German companies can bolster their technological position for key growth markets.

- The evolution of Germany’s market-leading wind power industry to this day is a “success story” for innovation policies focused on such opportunities. The rapid loss of a former pioneering role in photovoltaics can be considered a negative example.

8. At the same time, the imminent transformation process presents Germany with significant implementation challenges. The considered climate paths are economically cost-efficient and are based on the assumption of ideal implementation, meaning optimization across sectors and "right decisions being made at the right time." Mismanaging the implementation (think of excessive feed in-tariffs and delayed grid expansion in case of Germany’s “Energiewende”) could considerably increase costs and risks or even render the goal unattainable.

- The climate paths considered in this study assume a cost-effective selection and implementation of measures.

- The 80 percent path requires, beyond existing efforts, a further acceleration of the transition in the electricity sector, a significant expansion of sector coupling, greater exploitation of existing efficiency potentials, and a re-allocation of biomass to the industrial sector, among other things.

- Efforts required for achieving 95 percent emission reduction would be even greater and more complex. This would require the complete phase-out of fossil fuels for energy use, massive synthetic fuel imports, CCS in the industry sector, as well as a reduction of emissions from livestock. On top of the technical and economic hurdles, overcoming societal acceptance barriers against measures such as CCS will be a serious challenge.

- Despite successful renewable growth over the past 10 years, Germany’s mixed experience from the ongoing “Energiewende” indicates the dangers of inefficient political steering.

11 11 Such as excessive subsidies, delayed power grid expansion, sharply rising redispatch costs, or the shock of structural change in the energy industry that has not yet been fully absorbed. In the challenge ahead, overall complexity, direct involvement of citizens, and the impact on companies will be significantly larger. - Several implementation risks can make achieving Germany’s emission goals more expensive and thereby increase the costs for affected industries. These include, for example, further delays in grid expansion, insufficient demand flexibility from electricity consumers, a continued inefficient use of biomass outside the industrial sector, and a lack of efficiency gains in buildings and industry. Failing to avoid these risks would require a faster and more comprehensive exploitation of Germany`s renewable energy potential.

- In addition, cost risks for individual companies and industries could impact their international competitiveness. For example, electricity-intensive companies are faced with the risk of rising wholesale prices, as the flexible generation fleet shifts from nuclear power and coal to gas.

- Furthermore, the imminent economic transformation process will pose a challenge for existing value creation networks in several industries (e.g., automotive). Whether climate protection measures entail positive overall effects also depends on their impact on increased industrial value creation.

SIMILARLY AMBITIOUS IMPLEMENTATION BY OTHER MAJOR EMITTING COUNTRIES WOULD REDUCE RISKS AND INCREASE OPPORTUNITIES

9. On its own, Germany's share of global GHG emissions (a little more than 2 percent) is too small to significantly impact the climate. Comprehensive climate protection efforts in Germany are therefore only successful if they motivate other countries to follow suit. On the other hand, they could become counterproductive if a strong negative impact on the economy discouraged other states. A similarly ambitious implementation process by at least the largest economies (G20) would significantly reduce these risks and also open up greater export opportunities for German companies.

- In 2015, Germany's share of global GHG emissions amounted to about 2 percent, the European Union's share to about 12 percent. Even massive efforts on the part of Germany or the EU alone would not be sufficient to counter global warming.

- As one of the world’s leading industrial nations, any ambitious German initiatives to tackle greenhouse gas emissions would be closely watched by the rest of the world.

- Therefore, any economically and socially successful climate protection agenda in Germany could have a positive multiplier effect. This would present Germany with the opportunity to establish itself as a leading market for innovative and resource-efficient technologies, from which German companies could then secure a valuable position in the "race" for global market leadership.

- At the same time, negative economic effects of emission reduction measures—be they excessive costs or hard-hitting structural reforms—would not only unnecessarily increase the price tag of this complex transformation and in effect jeopardize acceptance within Germany. They would also act as deterrents in many other world regions, reversing their original intentions.

- Larger international consensus and similarities between political climate instruments in other countries—particularly in the G20—will lower the risk of negative structural economic effects from German climate action. At the same time, a global consensus on climate change mitigation would also boost export opportunities of resource-efficient technologies for German companies.

FIVE MAJOR POLITICAL AREAS FOR ACTION

10. Successfully achieving Germany's climate goals and a positive international multiplier effect therefore requires significant efforts on all fronts—politically, socially, and economically. It needs a long-term, holistic climate, industrial, and social policy that focuses on competition and cost efficiency, distributes the social burden fairly, ensures acceptance of the measures, and prioritizes the preservation and expansion of industrial value creation. The “centenary project” of mitigating Germany’s national contributions to climate change therefore calls for long-term political support.

- Policy makers are facing the challenging task of reconciling the implementation of complex climate protection measures with maintaining the competitiveness of Germany as an industrial location. At the same time, they need to ensure a fair burden-sharing and public acceptance. This will require long-term political support in five major areas.

- Action area 1: Establishing long-term, cross-sectoral policy frameworks. These include, among other things, an international approach towards climate protection instruments, reliable competition and investment conditions, as well as a continuous focus on cost efficiency.

- Action area 2: New climate policies and strategic decisions. Implementing the 80% climate path would require further impulses in all sectors, for example, additional efficiency increases, continued restructuring of the power system, creation of incentives for sector coupling, and ultimately GHG savings. In view of the much higher ambition and larger social tradeoffs, a 95 percent target would also require a comprehensive public debate and key strategic decisions in the coming years (e.g., CCS infrastructure, highway overhead lines).

- Action area 3: Public investments in infrastructure, research, and skills. For key infrastructure investments,

12 12 The key investments required include, for example, modernization of the rail system, development of a (fast-)charging infrastructure for electric vehicles, truck overhead lines, as well as storage and transport networks for carbon capture and storage (CCS). the public sector would have to create appropriate investment conditions, invest into research and scale-up of new technologies as well as in professional training and reskilling. - Action area 4: Monitoring and flexible steering. Any long-term strategy is subject to uncertainties—on the evolution of learning curves, the impact of political instruments, or the development of international climate ambitions. Actual progress should therefore be continuously monitored and flexible control mechanisms should be implemented.

- Action area 5: Complementary policy measures. These include ensuring a balanced distribution of the social burden, avoiding structural breaks, as well as linking climate and industrial policy to maintain, grow and modernize Germany’s industrial structure in parallel to achieving the climate objectives.