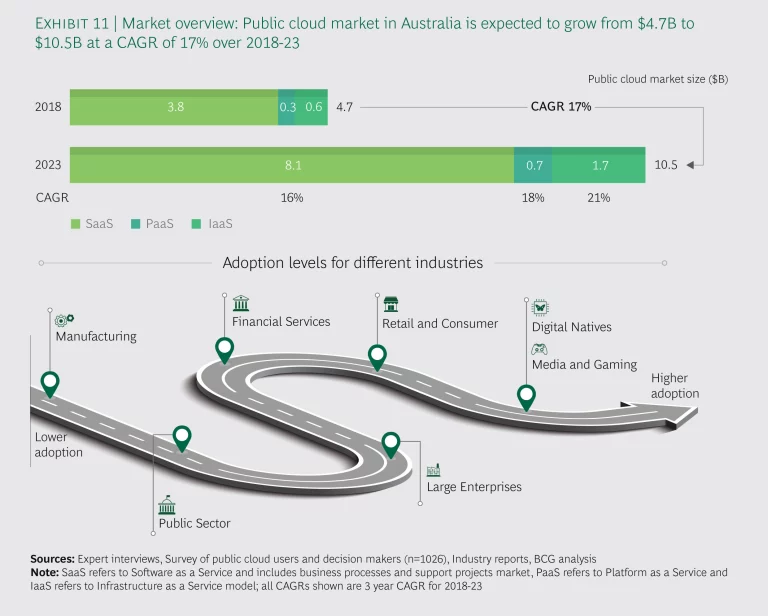

Australia is one of the most advanced public cloud markets in APAC. The market is expected to grow from a value of US$4.7 billion in 2018 to US$10.5 billion in 2023, with a CAGR of 17% over the next five years (See Exhibit 11).

Large enterprises across all business sectors have adopted the public cloud. This has been driven by a strong impetus from the government, which has created clear guidelines for data classification and other regulatory frameworks, and led the way to public cloud migration with its own cloud-first policy.

The largest users among industry verticals are media and gaming, retail and consumer, financial services, and the public sector. There is also increasing interest and traction with manufacturing and mining players in the market. Public cloud use has become increasingly sophisticated, with a focus on enhancing the customer or citizen experience.

SaaS is by far the largest segment, accounting for close to 70% of the market, but IaaS is expected to be the fastest growing between 2019 and 2023, with a CAGR of 21%.

Before 2014, users migrated to the public cloud largely as a means for achieving cost efficiencies. After that, however, the market began to evolve. Large companies were rapidly digitalizing their business functions and saw the value the public cloud brought when it came to developing new products and services. The government launched a cloud-first policy, and in recent years has greatly expanded its use, with federal and state agencies operating a variety of citizen-centric e-services.

Industry adoption

Media and gaming companies, followed by retailers and financial services institutions, have been major drivers of public cloud adoption in Australia. However, nearly all industry verticals are aware of the benefits of the public cloud when it comes to unlocking efficiencies across the value chain, and have harnessed it to some degree.

As the volume of applications deployed on the public cloud grows, businesses are using multiple vendors and hybrid clouds. There is a strong appetite among them for technology solutions that make it easy for the user to manage a multi-cloud environment.

The media industry has been at the forefront of adopting IaaS and PaaS. Use cases include such functions as data storage and encryption, content sharing and streaming, and digital content delivery, as well as meta-data analytics. Media companies are using these platforms to facilitate interactive customer experiences, real-time analytics to measure user engagement, strategic placement of ads, and real-time television viewing data and ratings.

“The public cloud allows us to scale quickly, spinning channels and events in seconds. The infrastructure is scalable to cater to spikes, and it’s easier to drive online viewing.” —Director, Media player

Retail players, too, have found that the public cloud is essential for increasing their supply chain efficiency as well as their operational efficiency across the value chain. Retailers told us that they’ve begun to use cognitive services as well, developing personalization technology to deliver ever more customer-centric experiences, and they are seeing a great deal of potential for real-time cross-channel customer engagement. One of Australia’s largest retailers, for example, is deepening its business intelligence through public cloud based advanced analytics and driving its loyalty program.

Many financial services players have adopted a cloud-first strategy. Although migration can be a slow process for legacy institutions, banks and other financial institutions are moving peripheral applications onto the cloud. ANZ Bank, one of Australia’s largest banks, is using cloud services to help analyse aggregated, de-identified data sets in order to deliver insights to their institutional customers, a task previously done manually. (See ANZ Bank case study). Some banks are evaluating the advantages of moving their core applications, which would require redesigning their applications as well as adhering to clear regulatory guidelines for how they can treat customer data. Moving their core functions such as foreign exchange platforms, loan approval systems, and leveraging big data and advanced analytics for product pricing, will make it possible for legacy banks to compete with newer financial technology businesses.

Use cases are also growing among manufacturing companies, especially in mining. In this industry, however, there has been some reluctance to move core applications onto the public cloud due to concerns about latency in connectivity.

The Australian government has taken a number of measures that help mitigate challenges to public cloud adoption and encourage its use. Its cloud-first policy has served as an endorsement to industry, signaling that data is secure on the public cloud, with cloud service providers offering classified services that are secure enough to receive government accreditation. Private sector users are well aware of the security and compliance standards set by the government, and the tendency is to follow or raise those standards internally, and hence when selecting a vendor they look for one that will meet their organization’s own standards.

In 2016, the government set up an online platform, cloud.gov.au, which provides tools and insights to make it easier for government agencies to install and operate public cloud services. Some 400 apps have been developed through cloud.gov.au and there is an ongoing process to add more applications on the cloud.

Key benefits

The key benefits identified by users of public cloud include:

Faster time to market for products and services. Many advanced users of the public cloud see agility as the most important benefit. As a highly developed market, Australia has many businesses that value the fast time to market that the public cloud makes possible. The time it takes to research newer digital products is much shorter than it would be otherwise; they can test early stage iterations of products at a lower cost, then receive quick feedback and quickly launch a completed version. The ability to try, and fail fast, with newer products, services, or business models gives a significant advantage to digital businesses, whether they are startups or new digital models for established companies.

“The turnaround time for results from cloud-based applications is weeks and days, instead of months and years. It accelerates minimum viable product development, and reduces the R&D costs and execution risk. It significantly changes the whole value proposition for us.” —CDO, Retail company

Higher team productivity and collaboration. Australian companies value both productivity and the way in which the public cloud fosters more efficient team collaboration, so that they can do more with the resources they have.

“The public cloud helps our teams coordinate and focus on solving problems in the core business, rather than on non-core requirements like administration and infrastructure.” —Senior Director, Tech firm

Enhanced ability to launch new products and services. Business leaders in Australia told us they place high importance on the way the public cloud allows their companies to be experimental and aggressive with new products. It is not just a matter of speed; the public cloud also facilitates new capabilities that make it possible to add new revenue streams. Financial institutions appreciate the way they can use analytics to personalize their products. E-commerce sites can run special sales that increase their web traffic without the risk of the server slowing down, and use advanced analytics to let individual consumer buying patterns guide their promotions.

Key challenges

The key challenges identified by users of public cloud include:

Legacy migration cost and risk. Migrating and integrating existing systems and databases is a particular challenge in Australia because a large proportion of businesses are large, established multi-nationals with significant investments in legacy technologies. They also tend to hold large storehouses of legacy data. Transferring historical data from traditional devices such as tapes or disks is a complex and risky exercise for large enterprises, including many banks, financial firms, insurance companies, and public sector agencies.

Gaps in organizational capabilities. While both providers and users are investing in employee training for the public cloud, and working with systems integrators to meet gaps, there are concerns that the gap will widen. The current supply of cloud-native talent is not large enough to match the rapidly growing demand, and many organizations in Australia say they are struggling to develop their internal team capabilities. In selecting a cloud provider, organizations look for one with services that are easy to use. A provider that offers internal training is also highly valued, particularly if the training is aimed at day-to-day management of public cloud platforms and fostering a deeper understanding of how the public cloud can enable advanced digital capabilities.

Complexity of managing multi-cloud environment. Most companies in Australia are interested in advanced uses for the public cloud, but are eager to explore operating in a multi-cloud environment so that they can gain from the expertise of a variety of providers, along with their private cloud and on-premise setups, and avoid being locked in with one vendor.

An IT leader at a systems integrator told us that when a company wants help with moving to the cloud, one of the requirements is that the integrators build systems for the company that are provider-agnostic, so that the organization doesn’t have to depend on a single provider. Working with multiple providers is a complicated proposition, and users need support in managing their multiple environments.

The economic impact

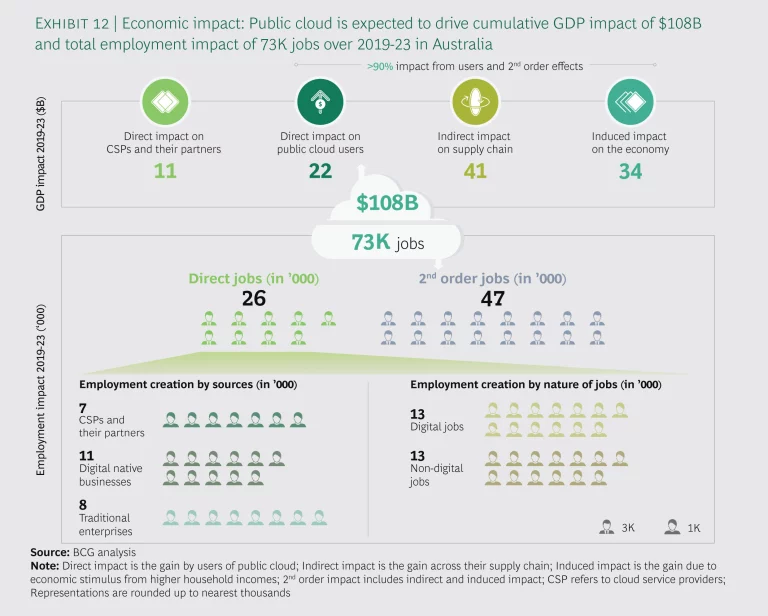

The overall cumulative economic impact from direct, indirect and induced sources is expected to be about US$110 billion, if CSPs continue to launch new products and services at their present rate and policymakers maintain their current stance on public cloud deployment (See Exhibit 12). When annualized, this is a sum equivalent to 1.5% of Australia’s annual GDP, about 50% of the annual economic impact of large traditional sectors such as mining, and about 15% of the annual impact of financial services. Around 90% of the total impact will be generated within industry verticals, particularly retail, financial services, media and gaming, and manufacturing, with about 10% from the growth of cloud service providers and the IT industry.

Public cloud usage stands to create close to 26,000 direct jobs over the next five years. Roughly 13,000 of the direct jobs will be in non-digital roles such as sales, marketing, human resources, finance, logistics and operations. Another 13,000 of those will be digital jobs, 7,000 of which will be with cloud service and IT system providers and the other 6,000 with industry verticals. This represents approximately 1.8% of the current information and communications technology workforce.

The second order effects are expected to influence another 47,000 indirect and induced jobs, bringing the total potential jobs that are influenced due to public cloud use to 73,000, which is equivalent to 0.6% of the current workforce. A large proportion of these jobs will likely be taken up by the existing workforce after their retraining and upskilling.

Two alternate scenarios

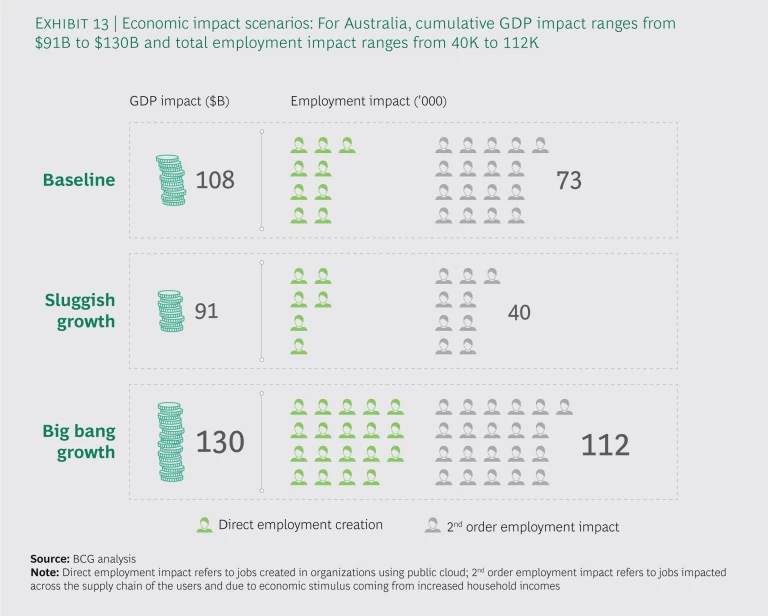

The economic impact we have assessed above is the Baseline Scenario, but we have drawn up two additional scenarios. The Big Bang Growth Scenario and the Sluggish Growth Scenario show the economic impact that would occur if the forces that shape the public cloud market cause growth to either speed up or slow down. If either of these scenarios were to unfold, the full cumulative economic impact of the public cloud could vary by a difference of nearly US$40 billion between 2019 and 2023 (See Exhibit 13).

The Big Bang Growth Scenario. Optimal growth would be the result of continued regulatory support and deployment of government applications, combined with the government and CSPs taking measures together to increase the pool of digital talent available in Australia. They would need to invest heavily in IT talent and enhance existing cloud literacy through strong promotion of cloud use.

In this scenario a CAGR of 22% would lead to a total impact of about US$130 billion, or 1.8% of Australia’s annual GDP. The growth would spur the creation of 53,000 direct jobs and influence 59,000 additional indirect and induced jobs, for a total of about 112,000 new jobs.

The Sluggish Growth Scenario. This scenario could be the outcome if the government were to become more restrictive, and the supply of cloud-literate talent comes under serious pressure, without enough training to close the gap between supply and demand. Restrictive data and digital policies including restrictions on cross-border data flows can impact sentiment and potentially reduce deployment, thereby inhibiting growth.

Here, CAGR would drop to 13%, bringing the total impact to US$90 billion, or 1.3% of annual GDP. Direct job creation would amount to about 16,000, with another 24,000 jobs influenced from the indirect and induced impact, for a total impact of 40,000 jobs.

The stage is set for Australia’s public cloud market to continue on a strong path, with businesses increasingly interested in using the cloud to help develop advanced digital capabilities, and government agencies actively using the public cloud to enhance citizen services. The main stumbling block to a more rapid growth scenario than the baseline is the supply of cloud-savvy talent that the country will need as demand for public cloud services increases. Australia would do well to push for more widespread cloud literacy and hands-on training of IT professionals. With a joint effort on the part of CSPs, government and business, use of the public cloud stands to generate a particularly notable effect on the economy and employment.