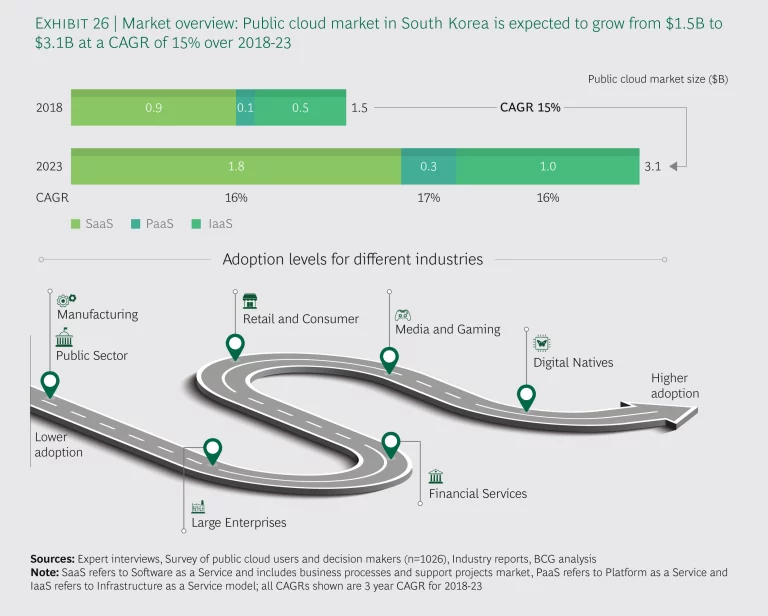

South Korea’s public cloud market is expected to double in size over the next five years from US$1.5 billion to US$3.1 billion, enjoying a compound annual growth rate of 15%.

The SaaS model is the largest and fastest growing segment, accounting for 45% of the market. IaaS is slowly gaining market share, and is expected to account for about one-third of the market by 2023 (See Exhibit 26).

Industry adoption

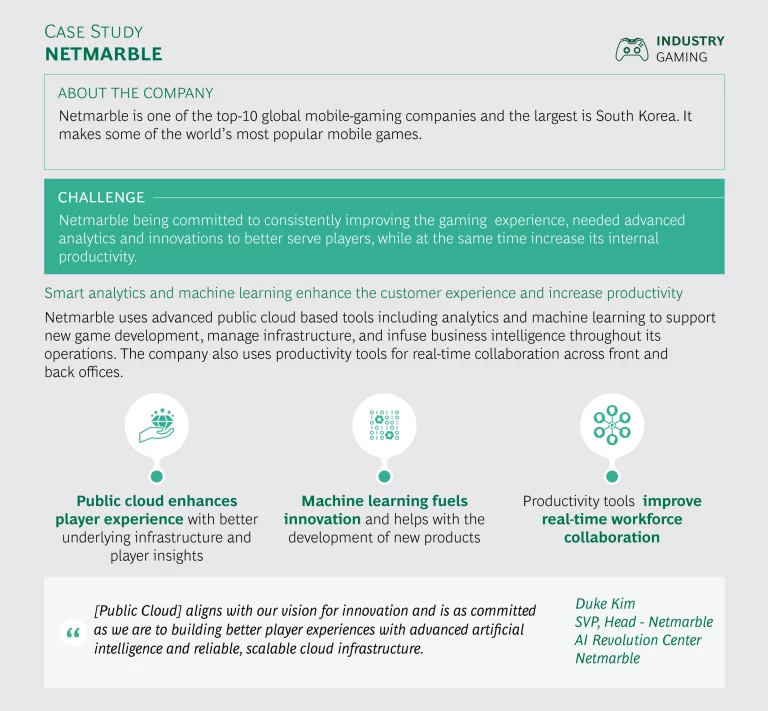

Digital native businesses, along with media and gaming companies, are major spenders in South Korea’s public cloud market. Online gaming, e-commerce, and other wholly digital businesses that need to deliver the best possible online experience can give their customers unprecedented speed, along with experimental games and features using augmented reality and virtual reality. The mobile game maker Netmarble, for example, uses smart analytics and machine learning to gain insights into its customers that help fuel further innovation, and has also found that the public cloud boosts its team productivity (See Netmarble case study).

E-commerce companies are using the public cloud to tap into big data that helps them personalize customer service. A large online seller of consumer products, for example, offers customers a subscription-based regular delivery service with automatic recommendations on products based on purchasing patterns. The rapid adoption by e-commerce startups has triggered interest from large retailers seeking to compete with DNBs. Both established retailers and e-commerce startups are using the public cloud to optimize delivery time by prediction of demand spikes, automate their warehouse logistics, and calculate the fastest routes. The public cloud also facilitates special promotions, with the scalability to handle surges in web traffic.

The financial services sector’s use of the public cloud was limited by law, but that is now changing. Until the guidelines were revised effective January 2019, South Korea’s Credit Information Act allowed only non-critical, non-identifying data to be stored on the public cloud. Now the Financial Services Commission (FSC) is making changes aimed at promoting more innovative growth in financial technologies. Financial institutions are moving cautiously, however.

“Right now, most banks are uploading only non-critical data on the public cloud to test it out. They are waiting to see what the Financial Services Commission will allow.” —Cloud Head, Large IT firm

Other industries are also taking note of the transformative technologies they can readily access when they have the public cloud to facilitate a level of sophistication that would be hard for individual companies—even massive conglomerates like South Korea’s ‘chaebols’—to develop on their own. The potential for such advanced functionality has been an incentive for new industry verticals to expand their usage, and we expect to see large enterprises using more IaaS and PaaS models. South Korea embarked on 5G network rollout this year, and this next generation of connectivity has the potential to create newer use cases which can further encourage public cloud use.

Many ‘chaebols’ built their own private clouds over the past few years, sometimes incorporating a hybrid cloud model, but South Korea’s conglomerates and other large established organizations have begun to migrate more of their applications to the public cloud, particularly to take advantage of the easy access to advanced technologies such as artificial intelligence, big data and machine learning. A large electronics manufacturer, for example, has announced it will migrate all of its data center applications to the public cloud. Some large players have started moving data to the public cloud for their global operations and adding newer use cases for local operations.

Once corporations and institutions make a decision to migrate applications to the public cloud, they tend to seek a hybrid or multi-provider arrangement to avoid vendor lock-in, and make the most out of each vendor. As a result, there is room for South Korean companies with experience in running their own private clouds to expand as local cloud service providers. These providers are likely to play an instrumental role in encouraging further public cloud adoption, but as demand accelerates, the market will grow for all providers.

In the past, regulations prevented government institutions from using any infrastructure other than the private government cloud (G-cloud), but these rules were relaxed beginning in 2018. In expanding the number of public sector institutions that are allowed to use the public cloud, the government is looking ahead to the growth of smart cities in which extensive connectivity will be needed for transportation and communication. To encourage further use of the public cloud by the public sector, the government has established a cloud security certification process and a clarified procurement process. If these processes are set up to conform to international standards, it will be possible for a broader range of cloud service providers, including hyper-scale providers, to offer more options and technologies including artificial intelligence and advanced machine learning technologies to government agencies through their public cloud platform.

Key benefits

The key benefits identified by public cloud users include:

Higher team productivity and collaboration. South Korean users, like those in all of the APAC markets we surveyed, expressed appreciation for the tools, techniques and operating models that can boost productivity. The public cloud’s development approach and collaboration tools drive benefits for user teams, driving an increase in the speed and productivity not only for IT but for core business and operations as well.

Digitization and launch of new products and services. South Korean users see the public cloud as a key enabler for a digital transformation. The diverse range of cloud-based offerings and services such as big data and AI are seen as among the more attractive reasons for migrating, and users are choosing their cloud service providers based on these capabilities.

LG CNS has developed a ‘smart factory’ using the Internet of Things, artificial intelligence, and other advanced technologies over the public cloud to test and model its products (See LG CNS case study).

“Users are interested in adopting the public cloud less for the benefits of the actual cloud migration such as cost saving, but more for the fact they can more freely and easily try out additional services such as AI, big data, and analytics.” —Director, ICT accelerator

Scalability and flexibility of infrastructure. Respondents told us that the scalability of the cloud can help curb capital investments in capacity for peak load usage, and facilitate a flexible, on-demand infrastructure to support peak loads. This is particularly important to South Korea’s gaming and e-commerce companies, which might have very heavy traffic to their site at certain times of day, and a notable dip at other times. Additionally, as more users begin developing big data analytics, they are likely to turn to the public cloud for its virtually unlimited data storage and processing capabilities.

Key challenges

The key challenges identified by public cloud users include:

Gaps in organizational capabilities. There is also much concern related to managing internal team capabilities. There is not enough cloud-native talent to meet the growth in demand for specialists who are equipped in the day-to-day practicalities of running applications on the public cloud. Leading companies are setting up internal programs to train cloud-native engineers at an aggressive rate. Users say, however, that cloud service providers can help mitigate this challenge by offering more training programs to increase not just cloud literacy, but also cloud capabilities, with training and certification programs aimed at practical training in the use of cloud technology.

With many South Korean companies becoming increasingly interested in developing capabilities in such areas as artificial intelligence and machine learning, users are looking for partnerships with providers that can support these skills.

Legacy migration cost and risk. South Korea’s ‘chaebols’ generally have their own legacy systems built by their IT subsidiaries, either on-premises or on a private cloud. Migrating these massive applications is a serious challenge to any established organization, and for that reason ease of use is an important factor that organizations consider when they’re selecting a cloud vendor. It may be hard to overcome concerns that the costs of migrating or integrating data to the public cloud will outweigh the cost savings, especially over the shorter term, although as more digital transformation opportunities arise, companies are starting to look beyond the costs of migration, focusing more on the need to be digitally competitive and explore newer sources of revenue.

Lack of clear understanding of data privacy features. Users said they remain worried about the privacy of their PII, and data leaks, though these risks exist whether data is hosted on-premise, on a private cloud, or on a public cloud. Strong security and compliance standards can be a deciding factor when they are choosing among public cloud vendors. While South Korea’s policy makers are considering a series of data privacy policy revisions, businesses are erring on the side of caution when it comes to storing sensitive data on the public cloud. One approach that is popular is the hybrid model, using a private cloud for more sensitive data, and the public cloud for front-end work. More advanced users of public cloud continue to deploy most applications, using different levels of security controls for different classification of data. Regulators can help by issuing stronger evidence of public cloud feasibility for government agencies, as well as supporting security standards and data classification systems that are interoperable with international standards.

Lack of clear understanding of product reliability and performance. Businesses expressed concern that any vendor they work with should have a track record for highly reliable service. This is a question that has arisen more often after one incident in 2018, a rare exception, in which a network failure shut down much of the country’s e-commerce activity for more than an hour. The hybrid cloud or multiple provider model is one way users ensure reliability. CSPs can also take measures to avoid network failures and enhance the reliability of their service, and reassure their clients that they’re doing so. Users should benchmark the online performance of their on-premise and private cloud systems against the public cloud to assess any differences.

The economic impact

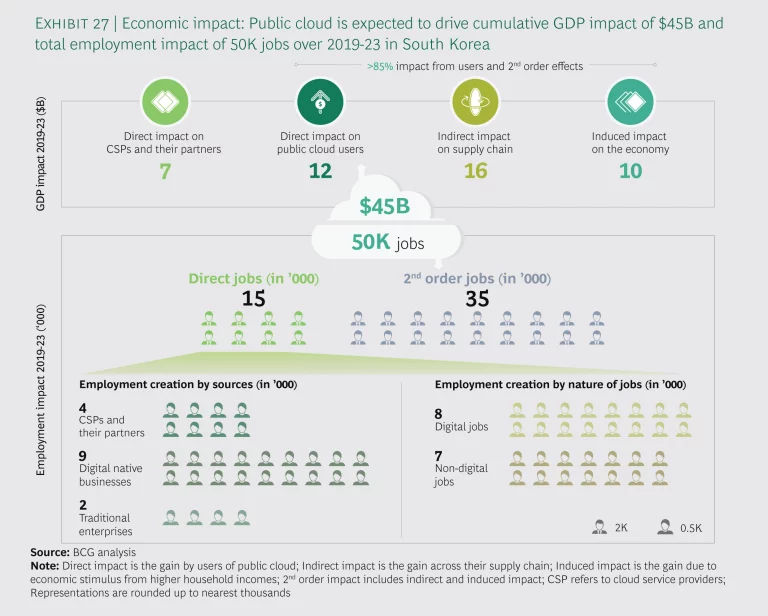

The overall cumulative economic impact from direct, indirect and induced sources is expected to be US$45 billion [SK₩54 trillion], if CSPs continue to launch new products and services at their present rate, and policymakers keep their existing stance on public cloud deployment. When annualized, this is equivalent to roughly 20% of the annual impact from large traditional sectors such as the automotive industry, about 10% of the annual impact of the electronics industry, and about 0.6% of the country’s annual GDP (See Exhibit 27).

About 85% of the total impact will be generated within user verticals, while around 15% of the impact will come from the growth of cloud service providers and the IT industry. Of the direct gains to industry, a major percentage will come from enhanced business revenues. A total of US$10 billion [SK₩12 trillion] will come from revenue uplift, while another US$1.3 billion [SK₩1.5 trillion] will result from productivity benefits, and US$0.5 billion [SK₩0.5 trillion] from IT-related cost reductions.

Half of the total impact is expected to come from the industries that have been the big spenders on the public cloud—digital native businesses, especially those in retail, along with media and gaming companies and select chaebols driving public cloud within their businesses.

Public cloud usage stands to create close to 15,000 direct jobs over the next five years. Roughly 7,000 of the direct jobs will be in non-digital roles such as sales, marketing, human resources, finance, logistics and operations. Another 8,000 will be digital jobs, of which an estimated 4,000 will be with cloud service and IT system providers and the remaining 4,000 will be with industry verticals— representing approximately 1% of the current information and communications technology workforce.

The second order effects are expected to influence another 35,000 indirect and induced jobs, bringing the total potential jobs that are offshoots of public cloud use to 50,000. That is equal to about 0.4% of the current workforce. A large proportion of these jobs will likely be taken up by the existing workforce after their retraining and upskilling.

Two alternate scenarios

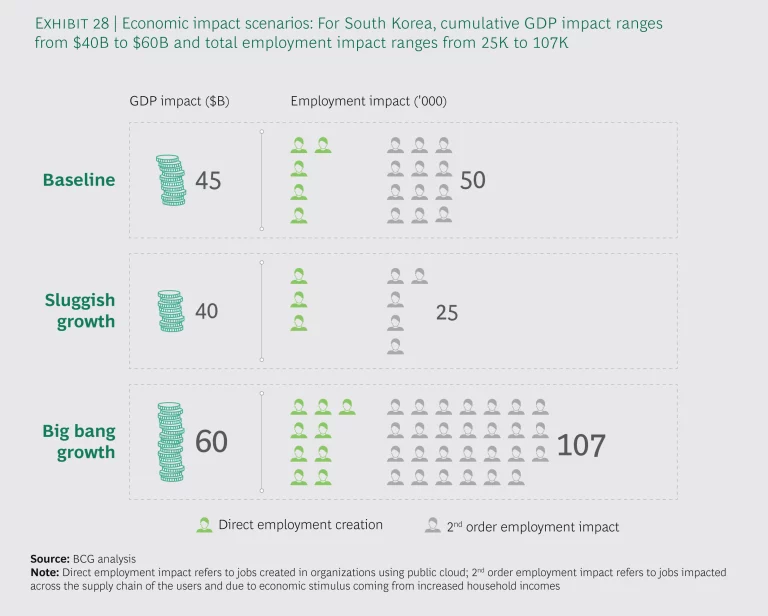

The economic impact we have assessed above represents the Baseline Scenario, but we have drawn up two additional scenarios. The Big Bang Growth Scenario and the Sluggish Growth Scenario show the economic impact that would occur if the forces that shape the public cloud market cause growth to either speed up or slow down. If either of these scenarios were to unfold, the full cumulative economic impact of the public cloud could vary by a difference of nearly US$20 billion [SK₩24 trillion] between 2019 and 2023 (See Exhibit 28).

The Big Bang Growth Scenario. This is the value that could be unlocked if the government, users, and cloud service providers combine their best efforts. All stakeholders need to work together to develop a pool of cloud-trained talent to meet future demands. Acceleration of the government’s ’digital nation’ push and a greater presence of hyper-scale service providers can also help drive further growth, as will a heightened emphasis on achieving digital transformation in large organizations and deploying newer technologies like AI and machine learning in business and government applications.

In this scenario, a CAGR of 24% would lead to a total economic impact of about US$60 billion [SK₩71 trillion], or 0.7% of annual GDP. This growth would spur the creation of 27,000 direct jobs and influence 80,000 additional indirect and induced jobs, for a total impact of approximately 107,000 jobs.

The Sluggish Growth Scenario. This scenario would be the outcome of a more restrictive policy environment, inadequate management of the cloud talent supply, and particularly, increasing moves toward market localization. A key trend to watch is the new government accreditation system—if it is not interoperable with international standards, it could affect the ability of global hyper-scale providers to introduce the best of breed technologies in the market, potentially slowing down and impacting deployment within organizations.

In this scenario, CAGR would sit at just 12%, with a total impact of US$40 billion [SK₩48 trillion], or 0.5% of annual GDP. Direct job creation would amount to about 9,000 jobs, with another 16,000 jobs influenced due to the indirect and induced impact, for a total of 25,000 jobs.

With digital native businesses and gaming industries driving the initial growth of the public cloud in South Korea, the country is expected to see even stronger growth over the next five years as ‘chaebols’ and other large traditional sectors, including banking, seek digital transformation and advanced capabilities in such technologies as artificial intelligence and machine learning. The government could do a great deal to further fuel this growth with a concerted effort to push for more migration and work with CSPs to educate digital talent in working with cloud technology. If government, providers, and users can work together to mitigate challenges such as the shortage of tech talent and the difficulties ‘chaebols’ and other very large traditional businesses have in migrating applications, by 2023 the use of the public cloud could produce, through the direct and second order effects, more than twice the jobs it would under our Baseline Scenario.