The competitive landscape for European machinery manufacturers—makers of traditional machinery (such as engines and turbines) as well as optical products and electronics—is changing rapidly. Chinese challengers are increasing their presence in developed markets and growing their businesses throughout the value chain. Once dismissed as low-end upstarts, Chinese machinery makers have built up their capabilities and now compete head-to-head with multinational companies on their home turf as well as in emerging markets. Indeed, China has driven the growth of machinery production worldwide in recent years. Chinese companies’ share of the global market increased from 23 percent in 2008 to 37 percent in 2012. During that period, the share claimed by German companies (the sector’s traditional leaders, especially for high-end products) decreased from 12 percent to 9 percent. Chinese companies’ growing share of the market also serves as a platform for expanding their offerings of higher-end products.

To avoid being overrun by aggressive challengers from China, European machinery manufacturers need to understand the new competitive landscape and develop an effective response to the emerging threats.

The Dragon Attacks

Chinese manufacturers have become strong competitors in the global economy on the basis of cost advantages arising from scale effects, as well as their large pool of low-cost labor. They have also used process innovations to increase productivity and efficiency. These advantages and innovations have helped Chinese challengers increase their share of the global market for construction equipment, for example, from 3 percent in 2006 to 15 percent in 2011. Market share gains have been even more impressive for Chinese manufacturers of telecommunications equipment and wind turbines: their sales represented approximately 25 percent of their respective markets in 2011, up from single digits five years earlier.

The ascent of Chinese challengers has been fueled in part by the rise of the middle market in rapidly developing economies (RDEs). RDE customers have boosted demand for “good enough” products that emphasize price competitiveness and sufficient functionality rather than customization and the most advanced technologies. These products occupy the middle ground between the low-cost products that have been a mainstay of Chinese cost innovators and the premium products typically offered by leading multinationals. Demand for good-enough products is also increasing in Europe and other developed markets, as companies seek to reduce supply chain costs in the face of persistent economic uncertainty.

Chinese companies are adding to their competitive strengths by building skills that go beyond cost leadership. In R&D, this means gaining access to advanced technology through either aggressive investments or acquisition of companies that have developed cutting-edge capabilities. To better serve their customers, Chinese players are offering both highly customized products and turnkey solutions. In an effort to improve access to global markets, they are building their own sales networks in developed countries or partnering with multinationals to share distribution channels.

Challengers are also investing to build global brands through, for example, event sponsorship. To reach upper-end customer segments and accelerate brand development, some Chinese companies have acquired a competitor with a premium brand. Using a “dual-brand strategy,” the acquiring company keeps both the premium and the low-cost brands in the market, each serving specific price segments. For example, China’s Sany Heavy Industry, a manufacturer of heavy machinery, acquired a majority stake in Putzmeister, a leading German manufacturer of high-tech concrete pumps. Sany remains focused on operations in China while Putzmeister continues as a premium brand. The acquisition also gave Sany access to Putzmeister’s innovative pump technology.

In addition to their cost advantages and ability to acquire Western technology and brands, Chinese challengers benefit from high demand within their home market as well as government support. China’s market is protected by formidable entry barriers, and the government invests in promoting the competitiveness of Chinese manufacturers and their aggressive pursuit of growth. Infrastructure investments have helped improve efficiency: for example, four Chinese ports are now among the global top ten ports in terms of cargo flow. Technology investments have improved manufacturing productivity and added value to products. The shift toward urbanization and improved living standards is also driving higher spending in the machinery sector. Reinforcing these developments, the Twelfth Five-Year Plan sets the goal of reaching higher levels of the value chain in manufacturing.

Chinese challengers will continue to use these strengths to build momentum. In this new competitive landscape, European companies can expect to see their traditional advantages diminish in areas such as advanced technology, brand strength, quality and reliability, and familiarity with customers.

Warning Signs in the Machinery Sector

Chinese machinery makers have already made impressive inroads into Europe and other developed markets. From 2008 through 2012, China’s exports of traditional machinery, optical products, and electronics to the European Union (EU), excluding Germany, increased by 23 percent. At the same time, Germany’s exports of these products to the EU decreased by 4 percent. China’s exports of these products to the rest of the world (excluding the EU) during this period increased by 44 percent, which far outpaced Germany’s increase of 16 percent. China’s exports of these products to Germany increased by 40 percent, while Germany’s exports to China showed a stronger increase of 64 percent. However, it remains to be seen whether German exports will sustain this growth rate given the rapid expansion of China’s machinery sector.

China’s increasing prominence in Germany’s stronghold of traditional machinery is especially noteworthy. The volume of Chinese exports of traditional machinery to the EU, excluding Germany, has exceeded 50 percent of German exports since 2011.

Moreover, the volume of Chinese exports of electronics to the region has matched or even exceeded German exports during this period. China has maintained a relatively smaller share of the market for optical products: the volume of Chinese exports to the region has ranged from 19 to 23 percent of German exports since 2011.

In contrast, Germany’s exports of traditional machinery to China are 12 percent lower than in 2011, and its exports of electronics to China have remained at approximately the same level. German exports of optical products have been an area of strength, increasing by 33 percent since 2011.

Identifying the Endangered Subsectors

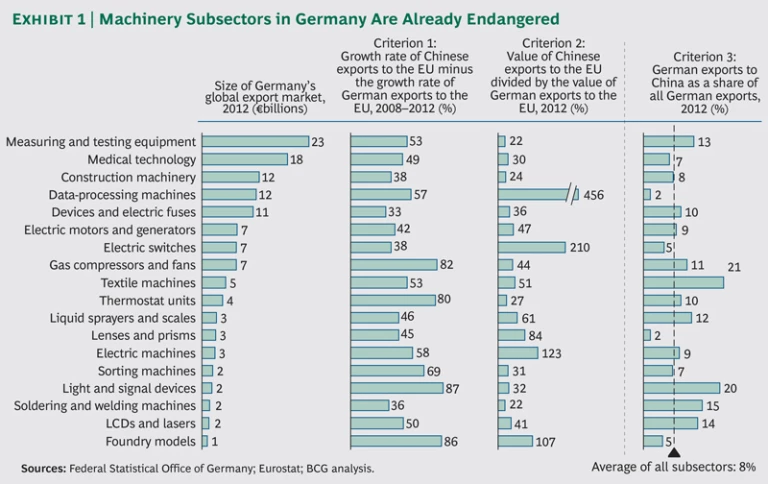

For some machinery subsectors in Germany, the threat from Chinese challengers is already evident. Our analysis identified 18 machinery subsectors endangered by Chinese exports. Exhibit 1 lists the subsectors in order of the size of the export market for German products and, thus, the subsector’s importance to the German economy. We then look at two criteria that indicate the severity of the threat to each subsector from Chinese competitors and a third that indicates the importance to Germany of its exports to China.

The first criterion is the difference between the growth rates of Chinese exports and European exports to the EU from 2008 through 2012. This figure is at least 80 percent for four subsectors—light and signal devices, foundry models, gas compressors and fans, and thermostat units—indicating that Chinese competitors are rapidly gaining ground on, if not overtaking, European manufacturers. The second is the relevance of Chinese exports in the subsector. Relevance is determined by dividing the value (in euros) of Chinese exports to the EU by the value of German exports to the region in 2012. Chinese exports have higher value in four subsectors—data-processing machines, electric switches, electric machines, and foundry models—meaning that Chinese attackers have already seized market leadership from German manufacturers.

The final column indicates the importance of the Chinese export market to each subsector, measured as a percentage of all exports in 2012. Subsectors with a higher percentage of exports to China have greater exposure to risks that stem from changes in tariffs and import duties, as well as slower growth of the Chinese market. Light and signal devices and textile machines are notable for sending one-fifth of their exports to China, giving them especially high exposure to these risks.

Assessing the Threat

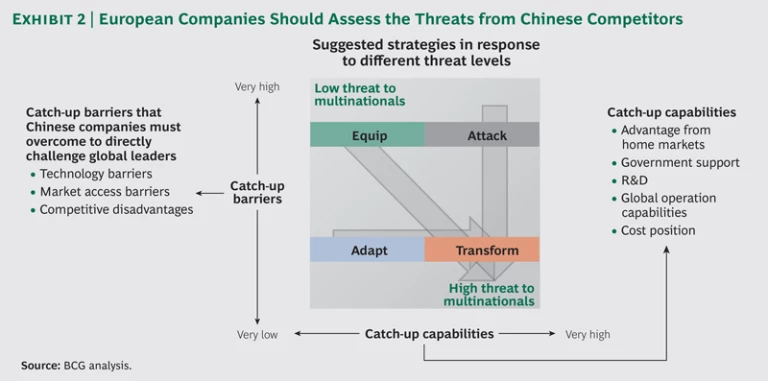

To respond effectively, European machinery manufacturers need to understand the specific threat Chinese competitors pose. We have constructed a “threat matrix” that classifies the intensity of Chinese competition in an industry or subsector. (For a general discussion of the matrix, see “The Next Wave of Chinese Cost Innovators,” BCG article, January 2013.) The matrix assesses the threat by considering the catch-up barriers (such as technology and market access) that Chinese companies must overcome to challenge global leaders directly, as well as their catch-up capabilities (such as R&D, cost position, and government support). On the basis of the threat classification, the assessment suggests four basic corresponding responses: equip, adapt, attack, and transform. (See Exhibit 2.)

-

Equip. In machinery subsectors in which the catch-up barriers are high and the catch-up capabilities of Chinese companies are low, European companies should nevertheless act to preserve their dominant position for as long as possible. They should create sustainable competitive advantages and speed up globalization efforts.

-

Adapt. In subsectors in which both catch-up barriers and the catch-up capabilities of Chinese companies are low, European companies should build strong cost advantages of their own and increase penetration in China and other emerging markets. That will give Chinese challengers less room to emerge in the home market and the good-enough segment.

-

Attack. In subsectors in which both catch-up barriers and the catch-up capabilities of Chinese companies are high, European companies should identify potential Chinese challengers and take preemptive action. This can mean competing directly with the challengers, trying to acquire them, or joining forces in strategic alliances. Companies that should pursue such a response include makers of medical technology and measuring and testing equipment—Germany’s two largest subsectors in terms of global exports. China’s exports to Europe are growing rapidly in these subsectors, but German companies still have the opportunity to defend their market leadership.

- Transform. In subsectors in which the catch-up barriers are low and the catch-up capabilities of Chinese companies are high, it is, in many cases, too late for defensive action or counterattack. European companies in this situation are likely to require deep and comprehensive transformation. German manufacturers of electric switches and data-processing machines may face the need for transformation given that Chinese challengers have already claimed a dominant share of the European export market.

This threat assessment should also inform a forward-looking risk analysis. European machinery manufacturers need to understand whether they are investing enough in R&D and offering sufficiently differentiated products. They also need to take a close look at how Chinese companies’ aggressive acquisition strategies have affected their business. This includes understanding the implications of Chinese acquisitions of competitors, suppliers, and customers, as well as technology transfers that have occurred or could occur in the medium term.

European manufacturers must also understand how Chinese competitors’ sales will develop in RDEs and the growth strategies the Chinese are pursuing. In this context, European companies should look at their own portfolios and consider whether they offer products suitable for or tailored to RDEs, including their own good-enough products aimed at the low-end and middle market. A slowdown in the growth of the Chinese export market is a further risk to assess. European companies need to understand how their share of exports to China will develop and the consequences of a decline in these exports.

The threat from Chinese challengers in the machinery sector will persist over the long term. Chinese companies will continue to invest heavily in R&D, expand their offerings of high-value products, and pursue aggressive acquisition strategies to gain access to technology, brands, and markets.

European companies in the most endangered machinery subsectors are already falling behind their Chinese competitors, notably in RDEs. The effort to reclaim a strong market position should begin with a thorough threat assessment. Companies should also review their business model, product portfolio, cost position, regional footprint, and relationships with Chinese competitors. The insights each company gains will form the basis for developing its tailored response that will position it to win in the rapidly evolving competitive landscape.