The technology industry has become a magnet for activist investors. These activists—figures as prominent in the investment scene as their targets are in the technology sector—include the likes of Carl Icahn, Jeffrey Smith (of Starboard Value), Dan Loeb (Third Point), Jeffrey Ubben (ValueAct Capital), and one of the fastest-rising activist investors, Jesse Cohn of Elliott Management. The attraction: maturing companies that activists perceive are falling short in delivering shareholder value.

For an industry that has long been synonymous with innovation, the newfound interest is sobering. Often, companies that become targets of activists are unprepared for the sudden and swift actions of these shareholders. As the CFO of a leading tech company recently told us, “One of the biggest things keeping me up at night is thinking about activist investors.”

In this new era, tech companies need to take a more proactive stance. We believe companies should respond to an activist’s challenge the way a judo fighter would answer an attacker: by anticipating the attacker’s moves and responding to circumvent his intent. Beyond gaining the ability to repel attack, companies can, more importantly, emerge stronger and more powerful as value creators.

What’s Fueling the Tech Frenzy?

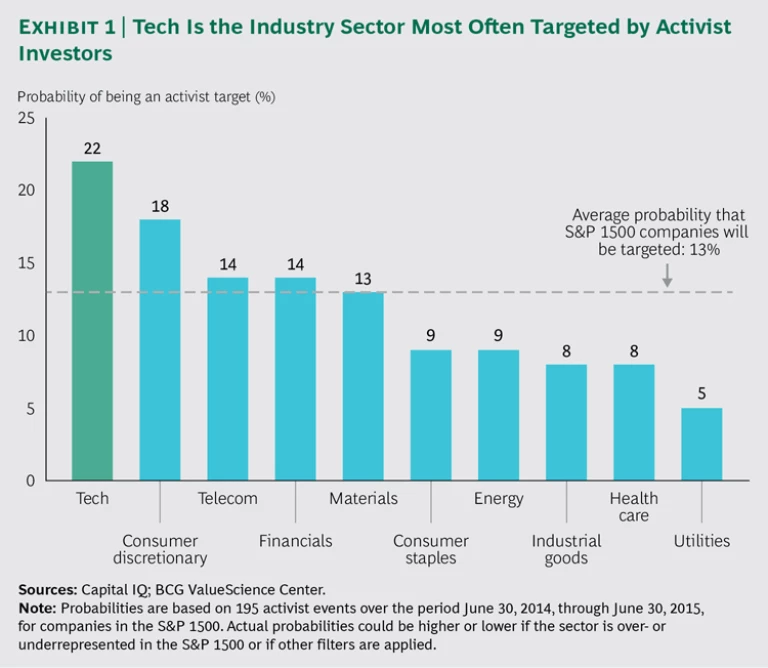

From 2010 through 2014, the number of activist challenges to companies across all sectors with upwards of $100 million in market capitalization more than quadrupled. (See Winning Moves in the Age of Shareholder Activism, BCG Focus, August 2015.) In the 12 months ending June 30, 2015, tech was the sector most targeted by activists. (See Exhibit 1.)

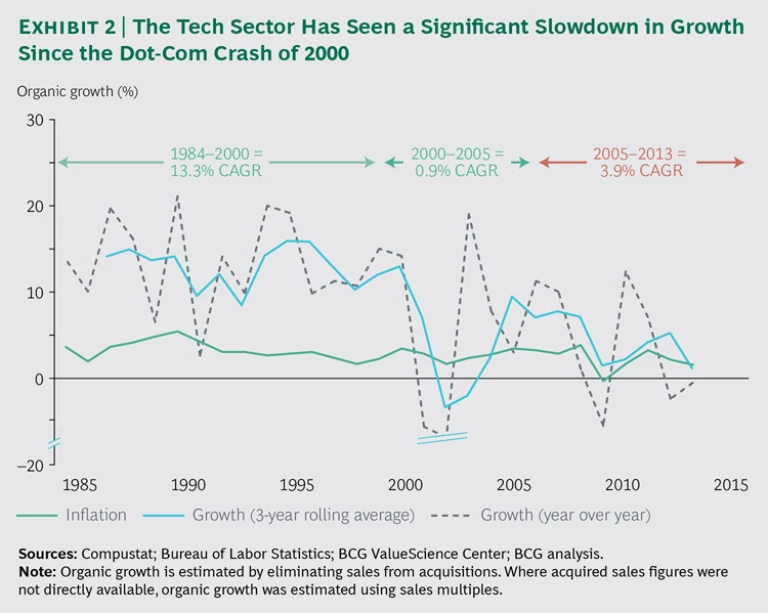

Underlying this broad increase is a fact of life in the corporate landscape: as industries and companies mature, management’s legacy thinking about the role of growth, capital deployment priorities, and business or product portfolios can create openings for activist intervention. And the tech industry has certainly been maturing. Since the recovery from the dot-com crash of 2000, organic sales growth has averaged 3.9% each year, a scant 1.4 percentage points higher than the inflation rate during that period. (See Exhibit 2.)

Projected growth is similarly muted, forecast at 3.4% annually for the period from 2013 through 2018. (See “Break Up or Shake Up: Get Ready for the Technology Industry Revolution,” BCG article, December 2014.)

Furthermore, over the past 30 years, the industry’s center of gravity has shifted radically, from PC- and storage-based ecosystems to the cloud, mobile, big data, and the Internet of Things. To sustain (or reinvigorate) the top-line growth that was historically the primary driver of their shareholder-value creation, many companies have tried to adjust their business models, focusing on these powerful tech trends as well as on software and customer solutions. Many have also tried to leverage their scale and deliver portfolio diversity. But these efforts haven’t always delivered shareholder value.

The Drivers of TSR Have Shifted

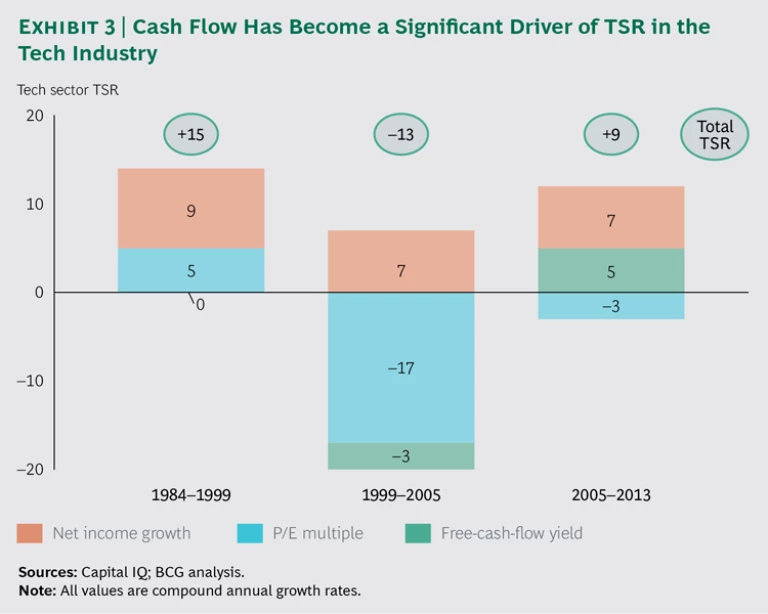

In the 1990s, total shareholder return in the tech industry was driven by growth and amplified by rising P/E multiples. Over the past decade, however, TSR has been lower than it was before the dot-com crash of 2000, a trend linked to the slowdown in organic growth and the corresponding decline in P/E multiples. Before, during, and after the crash, net income growth was a consistent driver of TSR because, as growth slowed, companies contained costs to improve margins. Today, with improved margins, lower revenue-growth rates, and lower P/E multiples, TSR is increasingly fueled by free-cash-flow yields in the form of dividends, share buybacks, and debt repayment. (See Exhibit 3.)

In our view, investor activism in the tech arena stems from management’s lagging reaction to changing TSR performance and the shifting dynamics of their businesses. Indeed, from Yahoo! to NetApp, from eBay to Motorola, activists have been forcing the value creation discussion upon technology companies’ executive teams and boards and, in the process, exerting massive influence on corporate decision making. Although activists’ moves have often been perceived as destructive, the reality is quite the opposite—and, indeed, the perception is changing. Objectively speaking, activists have helped usher in a new era of disciplined capital allocation among tech companies. At least 29 tech companies, for instance, initiated dividend programs in the period from 2008 through 2013. Where senior leaders once assumed they could reinvest all cash flow into operations or acquisitions, they are now being pressured to return at least some portion of capital directly to investors.

The Conditions That Trigger Activist Intervention

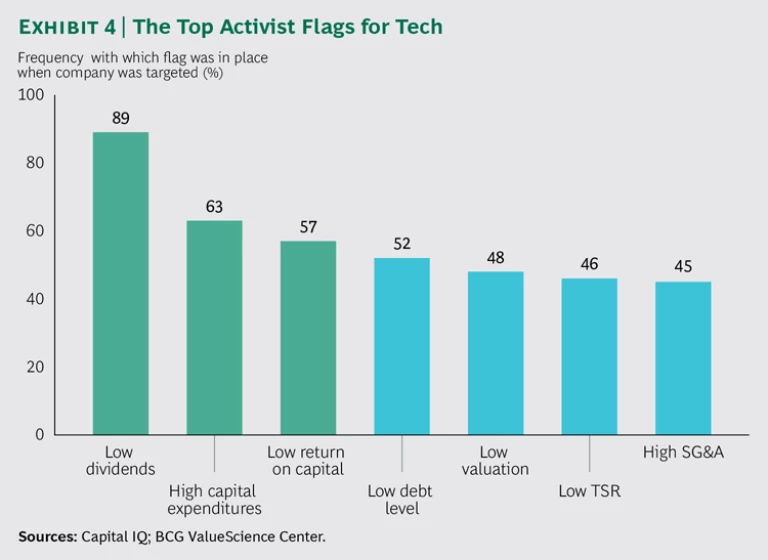

Through our research on the conditions that make companies ripe for activist intervention, The Boston Consulting Group has identified a number of financial indicators that, in combination, signal the likelihood of being targeted. For targeted tech companies, three of those flags rise to the top: low (or no) dividend payouts, high capital spending, and low return on capital. (See Exhibit 4.) Traditionally associated with slow-growth industrial companies, these three financial characteristics are now an important part of the tech landscape, too.

Other activist flags that BCG identified include low levels of debt on the balance sheet, a low valuation multiple, historically low TSR, and high SG&A expenses. Not surprisingly, a declining forward earnings growth rate (which was not part of BCG’s screen) is also often associated with activist targeting. Among 24 recent activist events involving tech companies with more than $100 million in market capitalization, forward earnings growth rates fell in the vast majority of cases—in many, by at least 50%.

As activists continue to make the rounds through the industry, two imperatives have become patently clear. Companies not only must be able to manage activists in the short term, they also must have a comprehensive plan to maximize value creation in the long term.

In other words, leaders should strive to create a better balance between delivering value today and positioning their company to deliver value in the future. Above all, value creation for shareholders and good governance should be the objectives and the overriding focus of the leadership team.

Four Activist Traits That Inform a “Judo Defense”

In addition to identifying activist flags, BCG has identified four defining characteristics of shareholder activists that should inform how tech executives keep activists at bay and foster more value creation for their shareholders. These characteristics include activists’ boldness, their well-honed investment thesis, their practice of rallying support from the investment community, and the value that they seem to inject into their targets.

Activists Are Bold

Activists have been making headlines in large part because of the boldness of their actions, starting with the size of their targets. Historically, their targets have been small. An activist could rapidly amass a 5% to 10% stake in a company and easily gain considerable influence by becoming a dominant shareholder.

But today, not even giant companies are immune to a campaign. The list of targets in the past two years alone is a veritable who’s who spanning the breadth of the industry: Apple, Microsoft, Sony, eBay, Juniper Networks, Yahoo!, AOL, Oracle, Dell, EMC, and NetApp, among others. The average target size jumped from a market cap of less than $3 billion in 2013 to one of $27 billion in 2014. Recently, Jana Partners acquired a 2% stake in Qualcomm Technologies (whose market cap at the time was $114 billion), illustrating how even a small stake is sufficient to influence an industry behemoth. There is no sign of the trend abating, either.

But activist boldness is measured by more than just target size. It is also reflected in the lengths to which activists are willing to go. By the very nature of their strategy—taking a significant ownership position in the company—activists commit to pursuing every possible option to generate the value they demand, often with fierce tenacity. Recall the disruptive legal battles (at Dell and Apple), the contentious proxy votes (Oracle), the aggressive PR campaigns (Yahoo!), and even the takeover bids (Riverbed Technology, Compuware). As capital continues to flow into their funds, activists are increasingly able and likely to impose their demands.

What can tech executives take away from this observation? Like activists, tech company executives would do well to question the current value thesis of their company—and be willing to consider bold, if not provocative, actions that could enhance it. BCG recently supported a leading tech company in doing just that: taking a fresh look at its business portfolio through activist eyes. The result was that management needed to consider divesting at least two businesses, that costs could be cut much further, and that capital allocation policies could be fine-tuned to attract more committed shareholders. Each of these remedies represents key value levers.

Activists Hold a Well-Honed Investment Thesis

Activists have developed a general thesis for their approach to tech companies, informed by an increasingly successful history across industries and tailored to the specific characteristics of their targets. Although not complex, this thesis has been proven and repeated across the industry. It consists of four core strategies.

Refine the business strategy. Increasingly, activists are positioning themselves as potential allies of company leaders, offering their own insights on strategic options and growth opportunities. They make their case, often in letters, white papers, or Microsoft PowerPoint decks that reveal a deep understanding of the business. They propose tangible steps to unlock value.

Take ValueAct Capital’s recommendations for Microsoft. In its first-quarter 2013 master-fund report to investors, ValueAct suggested that Microsoft was struggling to create value in the consumer and device sides of the business; instead, the document noted, the company should exploit its competitive advantage in the infrastructure areas of the technology landscape. These “enterprise-centric” businesses, ValueAct argued, already represented the lion’s share of Microsoft’s earnings, and 60% of their revenues come from multiyear annuity agreements. So not only were they lucrative in themselves, they held great potential for distributing new products and features.

Optimize portfolio composition. Activists are wary of corporate portfolios that appear to lack synergies, that unnecessarily divide management’s attention, that require strong businesses to subsidize weak ones, or that otherwise suggest that the whole may be less than the sum of its parts. With tech companies, TSR and portfolio diversity share an inverse relationship, so it is no surprise that many recent high-profile activist demands have involved divesting assets or splitting up companies: witness Yahoo!’s proposed spin-off of its investments in Alibaba (ultimately rejected) and Yahoo! Japan, PayPal’s break from eBay, and EMC’s spin-off of VMware. (More recently, Yahoo! began exploring strategic options for its core businesses and announced massive cost cuts, including shuttering offices and selling its digital magazines.)

Find efficiencies. Although activists have been distancing themselves from the slash-and-burn reputation they acquired in the 1980s, they are still on the lookout for opportunities to cut costs. Tech companies that augmented their R&D workforces in businesses with plateauing technologies to drive the next wave of growth, or that invested heavily in sales teams or partnerships to win market share, now face heightened scrutiny of their cost structures. For example, under pressure from Elliott Management and Jana Partners in 2014, Juniper Networks committed to a $160 million cost-savings plan. Similarly, Motorola, Qualcomm Technologies, and others have responded to activist pressure with operating-expense reductions of 15% or more.

Use cash to boost shareholder returns. Profit-rich tech giants have accumulated hefty amounts of cash on their balance sheets, amassing it faster than they can spend it on acquisitions or research opportunities. These dormant funds have captured the attention of activists who recognize that shareholder returns can often be boosted with dividends or share buybacks. Many activist demands have centered on returning cash to shareholders. Some activists even support repatriating overseas dollars (and paying the corporate taxes incurred) as a vehicle for returning cash to shareholders or reinvesting domestically, rather than allowing cash to languish indefinitely overseas. (Others, like Carl Icahn at Apple, advocate taking on substantial debt to pay cash to US investors and maintain foreign cash balances as a reserve.)

The moral here: develop an investment thesis that is as compelling as an activist’s. Know what creates shareholder value in the tech industry today—and in your company in particular. And hone a strategy that most effectively bridges the near-term value drivers with longer-term enhancements to the business.

Activists Rally Investors’ Support

The use of increasingly small ownership stakes to exert pressure on ever-larger targets is partly a function of necessity (that is, fund size constraints). But it is just as much the result of the growing push toward increasingly effective tactics. Stakes of 1% to 2% or even less can be large enough to provide an activist a soapbox, even if they are too small to formally qualify for a 13D filing with the US Securities and Exchange Commission.

Activists amplify their influence by rallying support from other activists or from institutional investors. Increasingly, pension funds and sovereign wealth funds are willing to follow, and even shape, activists’ game plans. Support from just one or two of these large shareholders is often enough to make the threat of a proxy battle real—and risky—for management. For example, Jeffrey Ubben of ValueAct Capital secured a board seat at Microsoft in 2014 with less than 1% ownership because he garnered support from institutional investors.

Tech executives could strengthen their position by understanding the kinds of actions that earn the support of large institutional investors. By maintaining an open and positive dialogue with shareholders, executives can signal their commitment to shareholders’ interests and command more support from the broader investor community. And by anticipating the activist agenda (before an event happens), they will be in a position to propose an alternative that could stand up to an activist’s thesis (or possibly even draw from it). As a tech CEO who resigned following an activist event commented to us, “If only we had been six months faster, this would have turned out so much differently. We already wanted to do 80% of what the activist was recommending.”

Activists (Seem to) Create Value

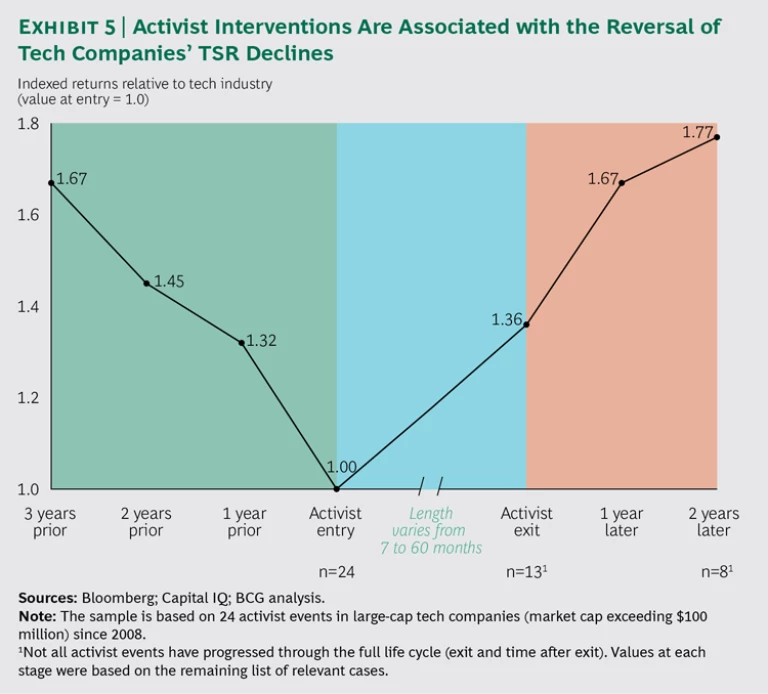

In examining 24 recent activist interventions at select tech companies, we found that, on average, the targets experienced significant reversals in TSR decline. (See Exhibit 5.) Contrary to popular perception, activism in Silicon Valley has, in fact, been associated with generally positive shareholder value creation, at least in the short term. Companies on average suffered TSR declines prior to an activist event and enjoyed 36% cumulative TSR during the activists’ involvement. Moreover, the interventions continued to generate shareholder value for two years after the activists exited, and often beyond that.

Public discourse and sentiment about activists have evolved considerably since the days of the evil corporate raider. In a December 2013 speech at a conference organized by the European Corporate Governance Institute, SEC chairperson Mary Jo White praised certain tactics employed by activists. Activist funds are beginning to establish themselves as a distinct asset class worthy of an increasing number of specialist reports and annual reviews. The Economist, Fortune, and the Wall Street Journal have all recently published pieces highlighting the controversial history, growing influence, and financial success of activist investors. All tech companies need to understand this pattern of shareholder value creation and the change in public sentiment as they consider their own TSR strategies.

Implications

Delivering sustained superior TSR is a major challenge, particularly as a company matures. And activists, as consummate opportunists, are keenly aware of companies that lose their footing or their focus in the face of this challenge. Activists pounce when they perceive a disconnect between achievable near-term value creation and a company’s priorities. Moreover, they are not shying away from taking on bigger challenges in the tech industry.

Tech leaders must seize the opportunity to prepare for potential confrontation by applying the principle of judo defense: using the very kinds of objectives and tactics that activists use to their own advantage. Leaders should ask themselves how well the business portfolio is returning value and be willing to make bold moves to enhance value. They need to develop a compelling investment thesis that addresses the business strategy, portfolio composition, opportunities for efficiencies, and use of cash in bolstering shareholder returns. They should demonstrate their commitment to shareholder interests. And they should recognize—and publicize—the value they generate through these actions. Adopting these measures is about more than just creating a solid defense: it’s about doing the right things to fuel and sustain value creation.