There’s a new player on the digital landscape. Digital (or digitalized) incumbents in traditional industries are joining digital natives and a small group of so-called digital hyperscalers in the congregation of companies that have developed the capabilities to disrupt existing business models and deliver the innovation and revenue growth that are rewarded by investors. But by our estimate, only about 30% of the companies in the S&P Global 1200 index are successfully transforming themselves into digital incumbents, leaving most legacy companies struggling to keep pace.

Digital incumbents enjoy multiple advantages. They outperform their less digital competitors, delivering more value to shareholders, customers, employees, and partners. Digital capabilities build resilience—the ability to adapt to adversity and changing market conditions. Achieving true bionic capacity—the point where human and technological capabilities combine to perform at a level that neither can achieve independently—requires a strong foundation of digital proficiency. But there’s also a flip side: incumbents that can’t transform will find themselves under expanding attack, and growth will be increasingly elusive.

The competitive landscape today is far more dynamic than the traditional “scale wins” pre-internet paradigm or the “digital natives will eat your lunch” internet-age template. Companies need to assess their capabilities realistically and understand that, with many further waves of technology disruption to come, growth from innovation will underpin future success. Winners will thrive by adapting their companies to a model of continuous innovation rather than sticking with static business models. It’s a big challenge, but our latest research offers empirical evidence that leading incumbents are indeed building the same digital capabilities as digital natives and can participate in value-creating growth from disruptive innovation. They start by putting their digital houses in good working order—and a successful digital transformation is the critical first step.

A New Hierarchy for Business

The research highlights the different digital dynamics in four types of companies: hyperscalers, digital natives, digital incumbents, and legacy incumbents.

Hyperscalers are the top dozen or so digital natives whose platforms, infrastructure, and data enable them to scale with enormous breadth and depth as demand increases, thus conferring major structural advantages. The dividing line between hyperscalers and other large digital natives is blurry, but the former include Meta (Facebook), Amazon, Apple, Netflix, Alphabet (Google), and Microsoft in the US as well as Baidu, Alibaba, and Tencent in China. Given their advanced digital capabilities and advantages in scale and scope, hyperscalers remain well positioned to be major disruptive forces in multiple markets in the future.

Digital natives, which are companies founded in the digital era, include such well-known names as Atlassian, Gojek, Pinterest, Roku, Spotify, and Zoom. Digital natives represent about 5% of the constituents of the S&P Global 1200. These companies are themselves evolving; many have excellent digital capabilities that enable them to disrupt traditional profit pools and grow to become tomorrow’s blue-chip stocks. Some, however, face risks similar to those of legacy companies as they struggle to combat the organizational complexity, out-of-date technology, and ways of working that come with age and size.

The new digital incumbents, traditional businesses that have successfully executed a digital transformation and are making progress in systematically building digital capabilities, can be found around the world in most industries. They include such companies as adidas, Diageo, ING, John Deere, KLM, L’Oréal, Ping An Insurance, and Telstra. Digital incumbents are beginning to break away from their traditional competitors by building the capabilities that can drive growth from disruptive innovation. Their capabilities already overlap those of digital natives.

Legacy incumbents, which are traditional companies that have yet to successfully achieve a significant digital transformation, risk becoming uncompetitive. These companies, which represent around two-thirds of the S&P 1200, are under real pressure from digital attackers.

Performance and Innovation

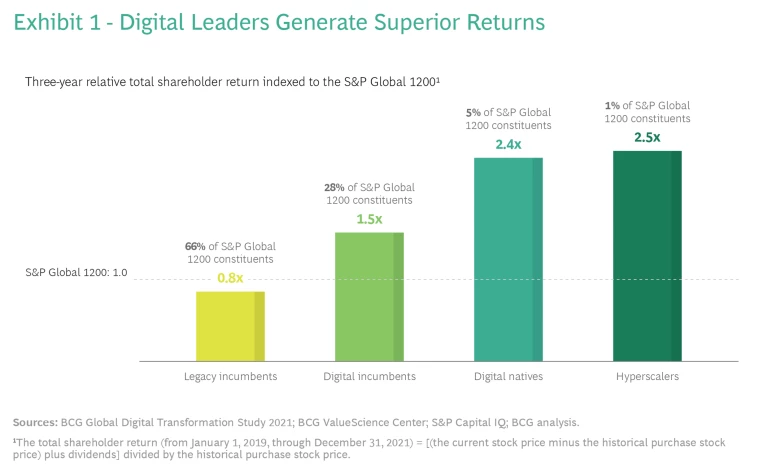

The successful companies of the future will follow the lead of hyperscalers and many digital natives by building digital capabilities—both human and technological—to become what we call bionic. Along the way, they will deliver superior innovation and performance. For the three years ending on December 31, 2021, hyperscalers generated returns that were 2.5 times higher than those of the S&P 1200 as they benefited from high growth and low unit costs in huge high-growth markets, such as cloud services, search, and data-driven advertising. (See Exhibit 1.) Digital natives overall performed at a similar level, benefiting from high growth and the high multiples that investors awarded to the future growth prospects of their disruptive business models. Leading digital incumbents outperformed the S&P 1200 by about 50% as they used their digital capabilities to improve customer experience and productivity and began to focus on innovative revenue growth. Legacy incumbents—which struggled to drive growth and improve productivity, relying predominantly on traditional levers—underperformed the index.

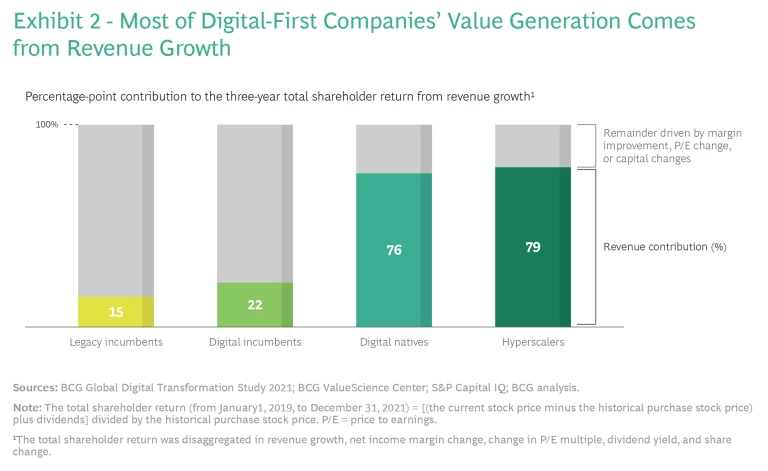

Much of the contribution to the high returns of digital companies comes from revenue growth. Leading digital incumbents generate significantly more value from growth than their legacy counterparts do, and they will emphasize growth even more as they pivot their agenda toward innovation both within and beyond the core. Revenue growth dominates value creation for digital natives, something that digital incumbents can aspire to as they build their innovation skills. Hyperscalers also continue to rack up impressive gains, especially given their size. (See Exhibit 2.)

A big reason for the outperformance of digital natives and hyperscalers is the ability to innovate continuously over time. Of the top 50 companies in our 2021 survey of the most innovative companies, 12 were either hyperscalers or digital natives—and many of the others were leading digital incumbents. (By comparison, back in 2010, only 4 of the top 50 were hyperscalers, and there were no other digital natives on the list.)

Becoming Bionic

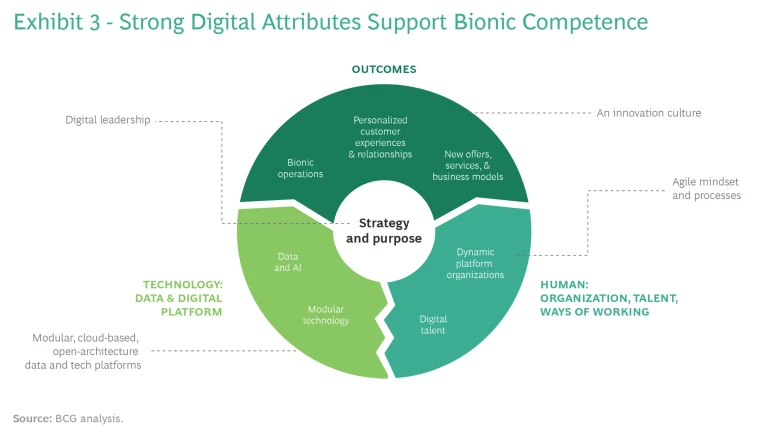

Digital transformations are difficult, but companies can dramatically flip the odds of successfully becoming a digital incumbent by applying the six key success factors for digital transformation that we identified in 2020. Once they have cleared that hurdle, they can invest in continuous, at-scale innovation, joining digital natives and hyperscalers on the journey toward becoming a bionic company. (See Exhibit 3.)

In our latest research, we asked more than 950 senior leaders from all types of companies to describe where they are on their digital or bionic journeys and to self-score their digital capabilities on a scale of 0 (low) to 10 (high). Our analysis of this data reveals that five attributes best define any company’s progress toward the bionic target state:

- Leadership with a purposeful digital strategy

- A culture that promotes innovation

- An agile operating model

- The ability to attract, retain, and develop world-class digital talent

- Open-architecture technology and data platforms

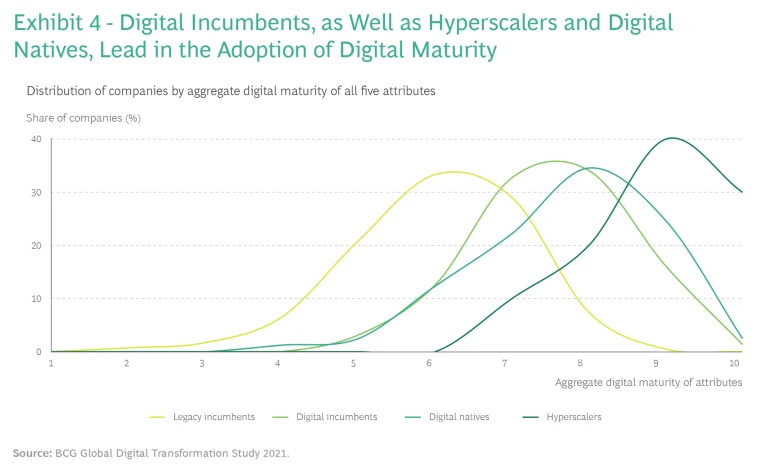

Hyperscalers, digital natives, and digital incumbents lead in the adoption of these attributes on an aggregate basis. (See Exhibit 4.)

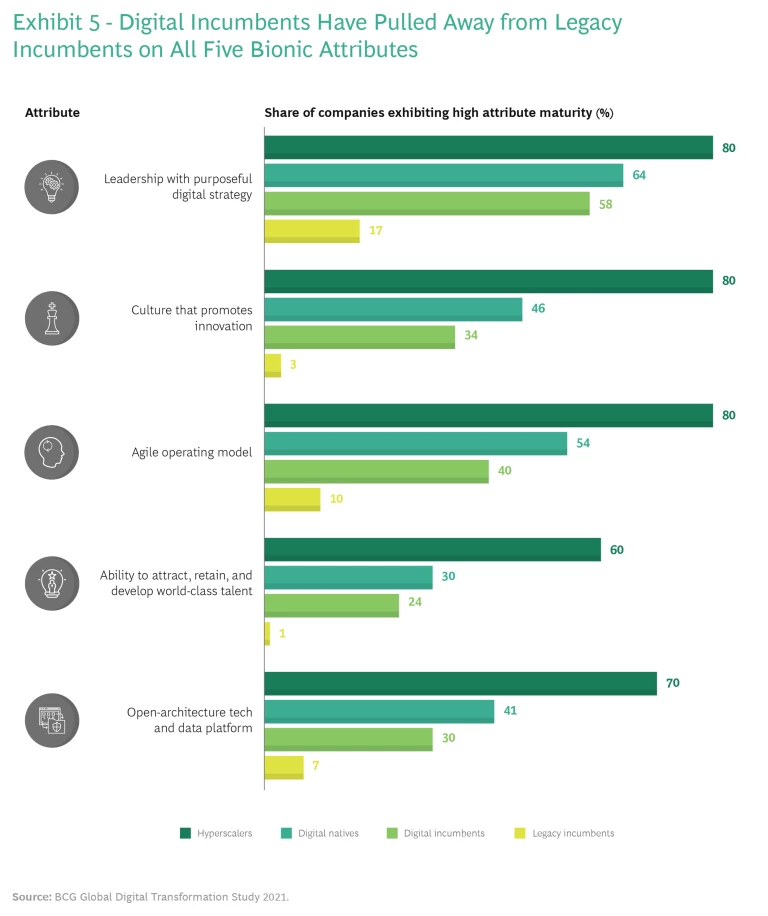

Half of hyperscalers exhibit strong adoption of all five attributes, with scores of 9 or 10 on each one. (These scores are all the more notable given the size and geographic spread of these companies.) But the really significant new dynamic is how digital incumbents are pulling away from their legacy competitors and catching up with digital natives. (See Exhibit 5.)

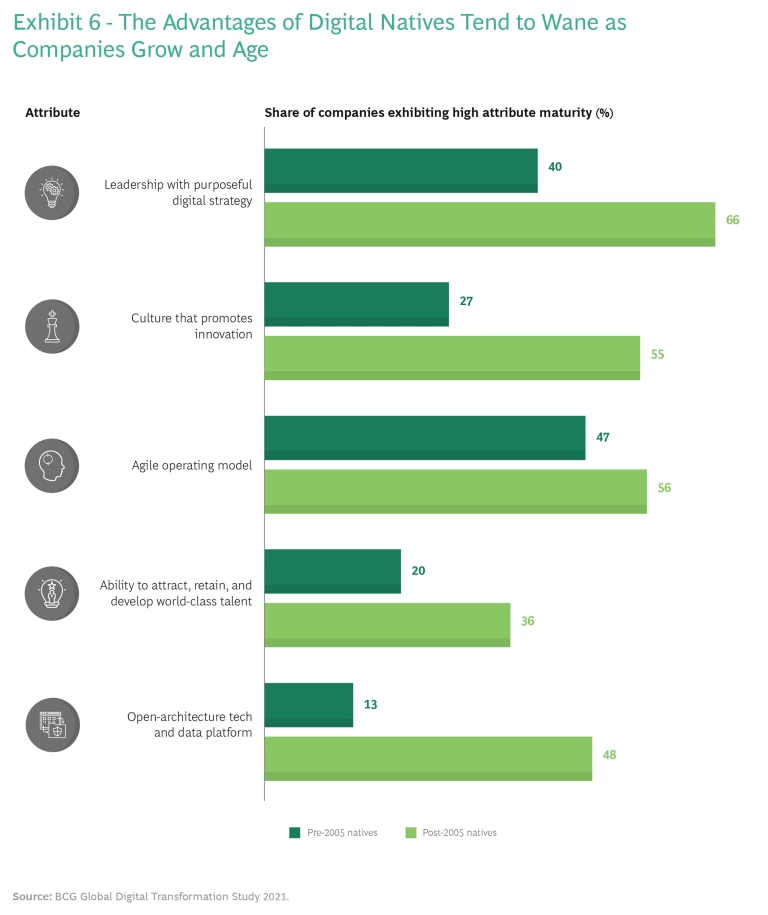

Some digital natives have allowed aspects of legacy behaviors to creep into their organizations. Those that were established before 2005 tend to have more legacy attributes, suggesting that as companies mature over time, there is some erosion in their digital attributes as it becomes hard to fight off legacy mindsets and technology debt. These companies will need to undertake their own digital transformations to regenerate their digital capabilities. (See Exhibit 6.)

Legacy incumbents have lower average scores on all attributes. They underperform most on having an agile organization and being able to attract and retain the best digital talent. Most legacy incumbents score below 8 on adopting an innovation culture and are effectively unable to drive shareholder value creation from innovative growth.

The executives we interviewed in our research offered interesting insights about each attribute.

Leadership and Purposeful Digital Strategy. Hyperscalers perform extremely well on leadership. Executives spoke about having a powerful purpose—including environmental, social, and governance aspirations—and communicating this purpose as an aligned leadership team. These companies define stretch goals to encourage executives to rise above incremental thinking and the delivery of short-term results. They promote imagination and diversity in points of view. As one executive said, “Being great at my day job isn’t good enough. To be a top performer, you need to push the envelope; new ideas and breakout thinking is what is rewarded.”

Digital incumbents and digital natives are, on average, evenly matched. Digital natives often rely on the personal charisma of founders and the influx of new, digitally savvy talent to drive innovation and speed to market. Some legacy incumbents also score relatively well on this attribute, but leaders in those companies are often frustrated by the inertia in their organizations.

Culture That Promotes Innovation. Executives at leading companies described several elements of this type of culture, including customer-centricity, a digital-first mindset, comfort with fast test-and-learn iterations and taking risks, continuously exploring new technologies, an operating model that enables continuous innovation at scale (as opposed to in isolated R&D teams), and metrics and incentives that track and reward innovation.

Hyperscalers and digital natives are most likely to possess an innovation-centric culture. They are particularly adept at establishing continuous customer feedback loops that power rapid iterations. As one digital native executive said, “Innovation for legacy companies is the cherry on top, but for us, innovation is the cake. We strongly believe that if we do not keep innovating, we will become irrelevant.” The one aspect of innovation on which hyperscalers don’t perform very well involves collaboration, information sharing, and transparency across teams, which some ascribe to the combination of their organization’s sheer size and business diversity. Not surprisingly, legacy incumbents perform poorly on this attribute.

Agile Operating Model. Leaders also called out different aspects of this attribute, including achieving effective end-to-end, or cross-functional, collaboration in mission-oriented teams; integrated business and technology teams with strong product ownership that are empowered to make decisions and alter course (within clear guardrails); and effective ways to fund and resource teams and missions, including early funding and quick scaling.

Once again, hyperscalers outperform. Amazon’s notion of single-threaded ownership—a 100% dedicated and accountable team leader who is responsible for turning strategy into results—is a classic example. Many digital native executives stress the importance of product ownership in innovation. As one said, “When we are creating the first minimum viable products, decision making is strongly anchored in the product leaders, who have almost complete autonomy and can take high levels of risk.” Leading digital incumbents score well—especially versus legacy incumbents—on such aspects as having mechanisms in place for stable funding and small, autonomous multidisciplinary teams.

Attracting and Retaining Digital Talent. Executives stressed that talent has become a major differentiator. Digital talent and data analytics talent are scarce, and companies with strong employee value propositions are often seen as good places to get ahead and develop important skills. Companies also need to innovate in terms of talent sourcing, using multiple recruitment and training channels, acquisitions, and new employment models to ensure an adequate supply.

Digital natives are especially strong at talent acquisition. They are often perceived as “cool” places to work and can boost employees’ resumes when workers move on. Digital natives score far less well on training and upskilling, however, in large part because they typically rely on individuals to keep their skills up to date. Leading digital incumbents usually have made a concerted effort to attract scarce digital talent. One CEO said, “Three years ago we weren’t attractive to data scientists, scrum masters, agile coaches, and the like. But we worked hard to show that we are investing in innovation in areas like virtual reality, IoT, and advanced analytics, and we are now seen as a place to build really exciting stuff.”

Hyperscalers and digital incumbents are good, on average, at creating personalized employee learning journeys. Conversely, legacy incumbents lag far behind in the war for talent, a weakness that, if left unaddressed, could become structural as other, more talent-focused companies widen their lead in this critical attribute.

Open-Architecture Technology and Data Platforms. Modern technology and data platforms enable agile, independent, small teams to operate at speed and scale without being bogged down by platform and data interdependencies. The technology architecture must also support access for external innovation partners, such as platform and infrastructure providers, and innovation in the application layer. In addition, executives mention the importance of being able to assess emerging platforms and technologies and determine how important they are in supporting business objectives, for example in risk management, regulatory compliance, and growth. Areas of particular interest include cybersecurity, AI-based decision support tools, emerging virtual- and mixed-reality solutions, blockchain, and cloud native applications. These requirements mandate modular, cloud-based architectures and a mindset that puts the application programming interface first. What’s more, effective technology and data governance must enable fast innovation in the experience layer and the prevention of technology debt.

Performance differences are again stark. Hyperscalers lead, with 80% describing themselves as having adopted cloud-based architectures at scale, smart business layers separating business logic from core transaction systems, and architectures that support personalization and omnichannel customer experiences. The comparable percentages on these elements for legacy incumbents are 38%, 22%, and 25%, respectively. On technology and data governance, hyperscalers and digital incumbents perform equally well, reflecting the intense focus applied in this area by transforming legacy companies. One executive from a digital incumbent said, “As you scale lots of agile teams, your data platform must enable them to work with the data autonomously and eliminate interdependencies, or nothing gets done as priorities clash across teams.”

Interestingly, digital natives score lower on data governance and tools. Often, they are prepared to sacrifice structure and scalability for speed. This tradeoff may become problematic as they grow. As one digital native executive told us, “You never really know who has access to what, and for how long. We have seen many knee-jerk reactions to changes in local data regulations, which may threaten our ability to scale.”

Tech + Us: Harness the power of technology and AI

More Change Looms

More technology advances are on the horizon. For example, Web 3.0 and the metaverse will mature. Decentralized finance, nonfungible tokens, and blockchain will continue to make inroads in various sectors. New device form factors will emerge. And waves of innovation associated with emissions reduction, synthetic biology, and low- and no-code software development platforms will arise.

Building an at-scale model of continuous innovation is hard, and companies in each category will face their own challenges.

Hyperscalers. These leaders look set to continue to enjoy the advantages of excellent digital attributes coupled with their advantages in platforms, infrastructure, and data. But they must take care to adapt and not to slide backwards as they deal with such threats as Web 3.0 decentralization. New entrepreneurs may try to circumvent their platforms, using open protocols, distributed platforms, and composable applications owned by their builders and users. Hyperscalers also need to be diligent about preserving their innovation cultures at scale across large and diverse organizations.

Digital Natives. The challenge for these companies is to continue to disrupt and innovate. They, too, must take care to stay on top of the five bionic attributes and not slide backwards into a more legacy mindset. For example, only 13% of pre-2005 digital natives report having small, nimble, multidisciplinary teams that own and run what they build collectively, compared with 44% of post-2005 natives and 70% of hyperscalers. Our data shows that 7% of pre-2005 natives constantly explore and adapt how the latest technologies can push the envelope for their businesses, behind 47% of post-2005 natives and 80% of hyperscalers. Sooner or later, all natives struggle with attracting strong talent and face an increasing need to build out “upskilling” programs, and only a third of pre-2005 natives have a strong employee value proposition for digital talent, trailing both post-2005 natives (58%) and hyperscalers (90%).

Digital Incumbents. Companies building significant digital capabilities should take heart from the findings of this research and develop and monetize their emerging advantages. They must continue to develop the five bionic attributes, which requires making the transition from successful digital reengineering to generating growth from innovation. For those that manage to build the necessary attributes at scale, the rewards of being both digitally capable and having the incumbent advantages of scale, scope, customer relationships, and data, will be substantial.

Legacy Incumbents. These businesses must act with urgency, because they are being left behind. Many of these companies have tried to achieve some form of digital transformation, but they have not yet prevailed. Some are declaring success prematurely as change fatigue sets in. They need to reapply themselves to the transformation agenda, starting with the six critical success factors we have identified: developing an integrated strategy with clear transformation goals; ensuring leadership commitment from CEO through middle management; deploying high-caliber talent; establishing an agile governance mindset that drives broader adoption; enabling effective monitoring of progress toward defined outcomes; and setting up business-led modular technology structure and data platform. Legacy incumbents need to quickly follow their digital incumbent counterparts in implementing the digital reengineering that will give them the digital capabilities they need to compete for growth.

The race is on to see which companies emerge as successful bionic enterprises. Incumbents, in particular, need to assess whether they are still dominated by legacy attributes or whether they are successfully developing at-scale digital capabilities. The required attributes, scorecards, and playbooks are now clear. The challenge for executive teams is to implement their digital agendas faster and better than others.