The US urgently needs a more aggressive approach to developing and adopting robotic technologies for manufacturing. Robotics will drive productivity enhancements, to compensate for a labor shortage and to counteract declining productivity growth. And a thriving domestic robotics industry will enhance America’s global competitiveness during a period of intensifying trade conflict. As a model for action, the US should look to China, where policymakers are pursuing such benefits for their national economy.

But technology by itself is not a magic bullet for enhancing productivity and competitiveness. The US must also build a skilled workforce capable of applying the new technology. Achieving these complementary objectives will require a targeted strategic approach that engages all stakeholders: manufacturers, academic institutions, and government agencies.

To provide a knowledge base for decision making about robotics in manufacturing, BCG recently undertook a study. (See “Deriving Insights into Robotics Adoption.”) The study identified the most important opportunities to target and offers actionable insights for those seeking to reinvigorate US manufacturing and facilitate the workforce’s transition into a new era.

DERIVING INSIGHTS INTO ROBOTICS ADOPTION

DERIVING INSIGHTS INTO ROBOTICS ADOPTION

The study sought to identify the priorities and enablers for robotics adoption in US manufacturing. We applied a broad definition of robotics; it includes such enabling technologies as artificial intelligence and robotic manipulation.

To identify which manufacturing sectors would benefit most from the productivity improvements generated by robotics, we evaluated sectors in terms of market size, relative growth rate, trade balance, and cost-competitiveness. By cross-referencing the US manufacturing jobs that have the highest labor costs against the high-priority sectors, we identified the jobs for which robotics solutions can best support US workers. We then looked more deeply at each of these high-impact jobs, analyzing occupational survey data, conducting more than 30 interviews with experienced operators from relevant industries, and engaging in discussions with a variety of robotics and automation experts from both industry and academia. On the basis of these inputs, we determined:

- The specific tasks for which robotics could drive the greatest improvements in worker productivity

- The robotics technologies that the US must advance to create commercially viable solutions that can perform each of these tasks

- The enablers that stakeholders must put in place to accelerate the pace of robotics adoption, including how the manufacturing workforce can best support adoption

BCG conducted the study in collaboration with Advanced Robotics for Manufacturing (ARM), a Manufacturing USA Institute. Dr. Howie Choset, a professor of robotics at Carnegie Mellon University and a coauthor of this article, was ARM's CTO during the study.

What’s Driving the Imperative?

Stakeholders must take a coordinated approach to capturing the productivity and competitiveness benefits of robotics. This imperative is driven by several developments:

- A Shortage of Labor. US manufacturing sectors are facing the most significant labor shortage since the late 1990s. Recent data highlights the severity of the challenge: in June 2018, the Federal Reserve Bank of St. Louis reported that job openings in US manufacturing sectors had reached 482,000 nationally, a 17-year high. To compensate for the deficit in manpower, stakeholders must find ways to improve workforce productivity or, in some cases, substitute for human workers.

- Declining Productivity Growth. The labor shortage is occurring as critical manufacturing sectors have experienced declines in productivity growth. (See “Productivity Now: A Call to Action for US Manufacturers,” BCG Focus, December 2016.) From 2011 through 2015, the pharmaceutical sector experienced the sharpest decline, with a median productivity growth rate of −2.8% per year. Indeed, negative growth was seen in nearly all sectors, including electronics (−0.9%), capital equipment (−0.8%), and aerospace (−0.5%). Only the automotive and consumer goods sectors saw positive growth during this period, but at a mere 1% and 0.4% per year, respectively.

- A More Competitive Export Market. Eking out small improvements in productivity each year will not be sufficient to compete in a global market characterized by rising trade barriers. Like all companies everywhere, US manufacturers must assess how they will be affected by the escalating trade conflict among some of world’s largest trading relationships. (See “How Much Will a Trade War Hurt Your Company?,” BCG article, August 2018.) To maintain leadership in a more competitive export market, US manufacturers will need to achieve step-change increases in productivity in key cost areas.

- Bold Moves by China. To improve productivity and regain its manufacturing-cost advantage, China is already making aggressive moves to accelerate robotics adoption. It plans to invest more than $350 billion as part of its Made in China 2025 initiative, which includes significant subsidies for robotics. Chinese manufacturers installed approximately 140,000 new robots in 2017, representing approximately one-third of the worldwide total and a nearly 60% increase over 2016 installations. To spur the growth of robotics manufacturing, the government’s Robotic Industry Development Plan sets an annual production target of 100,000 Chinese-branded robots by 2020. Additionally, at least 21 cities and five provinces have offered industrial robotics subsidies, with the total value reaching nearly $6 billion.

Targeting Sectors and Tasks for Maximum Impact

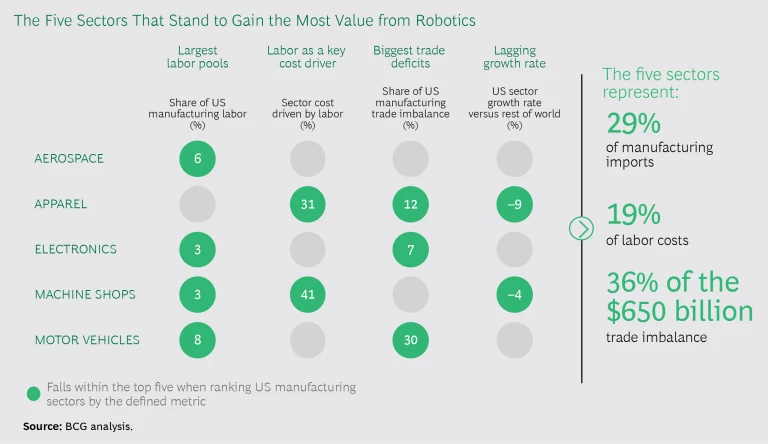

To maximize the benefits of a coordinated response to these developments, stakeholders must target the highest-value manufacturing sectors. Our analysis pointed to five sectors in which robotics can promote the greatest improvements: aerospace, apparel, electronics, machine shops, and motor vehicles. (See the exhibit.) In 2016, these five sectors collectively represented 29% of US manufacturing imports, 19% of US manufacturing labor costs, and 36% of the country’s $650 billion trade imbalance in manufacturing. Further, in each of these sectors, many workers—such as assemblers and machine operators—manually perform repeatable tasks that would strongly benefit from robotics support, creating significant opportunities for productivity gains.

To drive productivity improvements and job creation in the high-priority sectors, robotic solutions will need to support a wide variety of tasks, including the following.

Identification, Tracking, and Movement of Components, Parts, and Tools. Workers in diverse sectors (such as aerospace, logistics, and motor vehicles) spend a significant amount of time tracing or retrieving items as they move across a shop floor or warehouse. Collaborative-robot (or “cobot”) solutions have been developed to assist with some of these tasks, such as retrieval. However, these solutions are not mature enough technically to execute processes under dynamic circumstances or support end-to-end task execution. If and when cobots become capable of taking on the related tasks by themselves, workers will be able to devote time to more-productive tasks.

Supervision and Training. Frontline supervisors represent the second largest category of labor cost for US manufacturers. They manage workers on the shop floor to monitor quality and safety, providing real-time feedback. Many of their tasks (for example, ensuring that workers use safe techniques for heavy lifting) could be partially automated or abetted by robotics, helping to create more efficient and safer work environments.

Routing and Connecting Wiring. Wiring and wire harness assembly are highly time-consuming tasks in several manufacturing sectors, including aerospace, electronics, and motor vehicles. Human workers apply their dexterity and maneuverability to complete these tasks. Existing robotics technology cannot come close to replicating these human capabilities. A breakthrough advance will unlock significant value.

Precision Handling and Assembly of Small Components. In some sectors, such as electronics manufacturing, many device components are extremely small. Robots are adroit at handling tiny uniform components, such as those typically used in semiconductors. But handling components of varying sizes and shapes—as is commonly required in manufacturing communications products—poses significant challenges for robots. Technological advancements that enable robotic handling of a broader range of small components would deliver productivity gains in multiple sectors.

Translating Schematics into Production. US manufacturing workers commonly cite “reviewing blueprints” as one of their most frequent tasks during both assembly and inspection. Today, the systems used for developing schematics and blueprints do not interface with those used to program robots. As a result, workers require lengthy amounts of time to review schematics and then program robots accordingly. Advanced and interoperable systems will enable robots to accurately translate schematics directly into actions with precision, eliminating the need for workers to serve as intermediaries.

Where Is Technical Progress Needed?

To develop commercially viable robotics solutions that can perform the aforementioned tasks, robotics manufacturers and academic institutions must achieve advances in a variety of technical capabilities.

Perception, Sensing, and Situational Awareness. By capitalizing on recent advances in robot vision, stakeholders can enable robots to support the rapid reconfiguration and tight integration of manufacturing systems. Specifically, they must replace precisely calibrated setups for sensing systems with new approaches that can accommodate a diversity of lighting conditions and material properties. New techniques are also required to enable sensing systems to accurately identify, track, and handle parts, so as to reach performance levels comparable to those achieved in controlled environments.

Dexterity and Adaptability. Most robotics-assisted tasks require the ability to securely grasp and manipulate diverse parts, including deformable materials in composites and textile manufacturing. Strategies for improving dexterity typically involve coordinating many degrees of freedom (for example, joints), developing end effectors and sensors, and integrating systems of core technologies. More dexterous, and thus adaptable, robots will create more use cases and opportunities for productivity gains.

Human-Robot Cooperation. Today’s industrial robots are not designed to work directly alongside humans. They operate without considering the conditions in their surrounding environment, which creates a safety hazard for human workers. Next-generation robots must be able to utilize their strength and speed while working collaboratively with workers to improve productivity, enhance quality, and reduce strain and injuries. Novel types of manipulators, motion planners, and obstacle detectors will enable robots to move safely and efficiently among workers. Such cooperation holds the potential to increase first-pass yield, reduce rework, enhance operational efficiency, and improve ergonomics. Algorithms will help to validate the statistical characteristics of safety-critical behaviors and test these new systems to guarantee workplace safety.

How Can Stakeholders Support Adoption?

Technological advances in robotics are not sufficient by themselves to bring the desired improvements to US manufacturing. To achieve the full impact of robotics, stakeholders must also devote greater resources to improving skills within the workforce and developing standardized solutions.

A Skilled, Adaptive Workforce. The skills profile of the manufacturing workforce is shifting dramatically, with regard to both the types of jobs that workers do and the skills required to do them. Alongside the growth of existing job categories—IT solution architects, industrial-data scientists, and field service engineers—new job categories, including robot coordinator, supervisor, and planner, will emerge. Many of these jobs will require “adaptive skills,” such as the ability to continually learn, adjust to new digital devices and software, and use virtual knowledge bases. (See “Building an Adaptive US Manufacturing Workforce,” BCG article, September 2017.) BCG estimates that among today’s skilled workers and those workers currently being trained, roughly half may not qualify for the jobs that will be in the greatest demand over the next decade.

To ensure that the workforce is prepared, it is essential to provide greater access to educational content that relates to working with new manufacturing technologies. Workforce participants should be introduced to this content in high schools, community colleges, and continuing-education programs. Additionally, other sectors have proven the value of establishing apprenticeship programs and supporting the efforts of small and midsize businesses to train workers. Government support will be important to the success of such initiatives.

Standardization. Metrics used for robotics suffer from a lack of standardization. The variability of metrics impedes efforts to benchmark best-in-class solutions and makes it harder for executives to evaluate technical solutions, thus slowing adoption. It also inhibits the coordination of research agendas, which makes investing in robotics R&D inefficient.

Similarly, given the diverse software and hardware platforms available, companies find it difficult to implement robotics systems one at a time; each additional robotic component must be individually programmed at great expense. The high switching costs mean that users are locked into their vendors, diminishing the opportunities to replace hardware or adopt entirely new systems.

The fragmentation and proprietary status of robotics software and hardware slows the progress of the entire field. Because employees need nonstandard skill sets and exposure to different systems, companies face difficulty hiring qualified, knowledgeable workers. The challenge is especially acute for small and midsize businesses with limited resources to identify and prepare talent.

Taken together, the key imperatives identified in our study—targeting the most valuable sectors, advancing technologies, and enabling adoption through skill building and standardization—represent a path forward for manufacturing and robotics stakeholders. Seizing this opportunity will require a unified effort. Essential initiatives include investment in R&D at leading universities to fuel technological breakthroughs, funding for job training and the reskilling of a 21st-century workforce via community colleges and innovative programs, and partnerships across sectors to fully leverage robotics’ industrial potential. With leadership, support, and coordination from federal and state governments, the US can bolster the cost-competitiveness of its manufacturing sectors and thereby achieve gains in productivity, job creation, and economic growth.