Computing’s locus of activity is continually changing, from mainframes to desktops to the cloud and now to the edge. This outward push often goes by the name Internet of Things, but IoT does not fully capture the revolutionary shift that is transforming how we work, live, and play.

The 20 billion connected sensors and devices that make up the IoT are not just things. They are enablers of a new world of decentralized intelligence that will unleash new business models (such as remote health care), new behaviors (resulting from fully automated homes, for instance), and new forms of disruption. Edge computing accelerates the ability of companies to become bionic by giving them access to massive data sets, many of them related to human activity, and the means to understand this information in new ways through artificial intelligence.

Edge computing will generate winners and losers, just as prior shifts have. Compared with cloud computing, however, competing at the edge requires a more complex set of skills and capabilities, so today’s winners may not be tomorrow’s.

Before exploring the contest, we need to understand the battlefield: what exactly is edge computing, how fast is it growing, what are its most popular uses, and which companies are positioned to win?

The Edge Defined

Edge computing has gained currency in the past few years, but the idea of moving processing and intelligence closer to the physical world is a couple of decades old. At the turn of the century, for example, content distribution networks (CDNs) started to bring computation and storage closer to the edge, with regional data centers able to speed up the crawling World Wide Web.

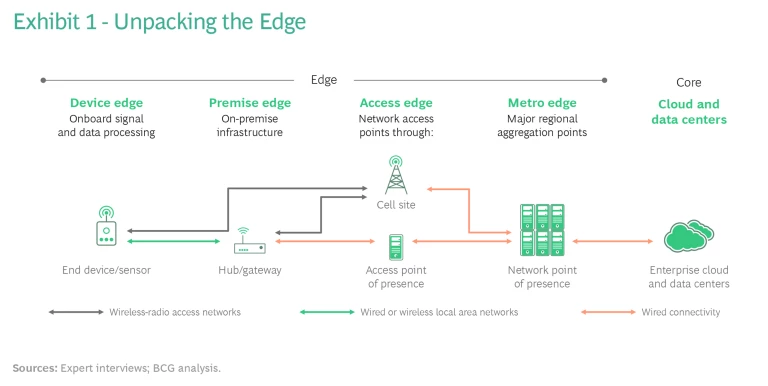

According to many definitions, the edge is limited to, or is close to, IoT devices themselves. But that narrow focus misses the connectivity and data flows that bring edge computing to life, as well as the hardware and infrastructure that link the edge to the cloud. To provide an end-to-end view, we divide the edge into four stages, as shown in Exhibit 1, according to where computation and storage occur:

- Device Edge: Onboard signal and data processing at the device

- Premise Edge: On-premise infrastructure in the enterprise, car, or home

- Access Edge: Network access points that connect to large aggregation centers

- Metro Edge: Major aggregation points, including Internet service providers and data centers, covering traffic within a region

A self-driving car, for example, depends on more than its sensors and onboard computer. The car is continually processing data onboard (at the premise edge), but it is also delivering training data (via the access and metro edges) to a centralized machine-learning algorithm. Traffic-monitoring and accident detection systems increasingly have machine-learning chips embedded in the camera at the edge. When data is processed at the far edge of the network, latency and bandwidth costs are radically reduced, with no sacrifice in the ability to report accidents and traffic tie-ups to a central service.

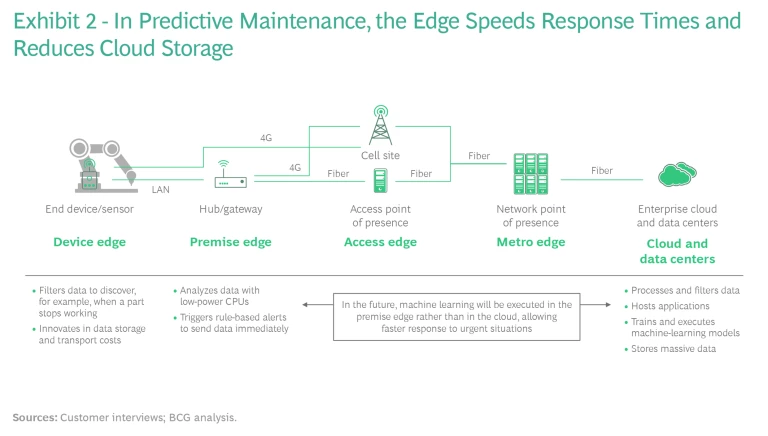

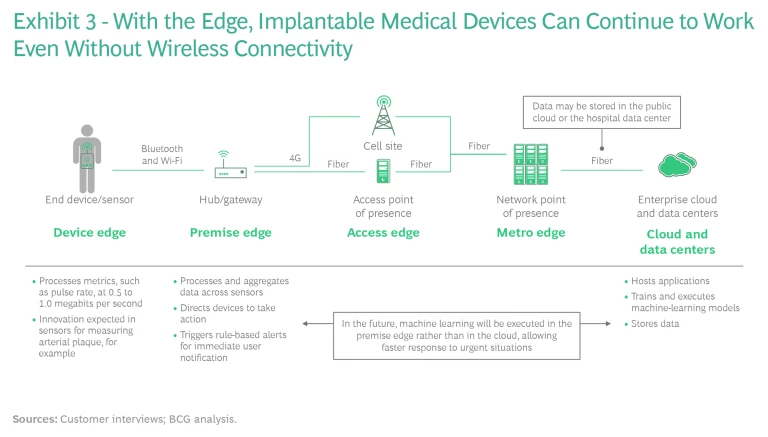

Self-driving cars are perhaps the most prominent example of edge computing in action, but there are many others, ranging from predictive maintenance to implantable medical monitoring devices. Each use accesses and benefits the edge in slightly different ways. (See Exhibit 2 and Exhibit 3.)

The Projected Size of the Edge

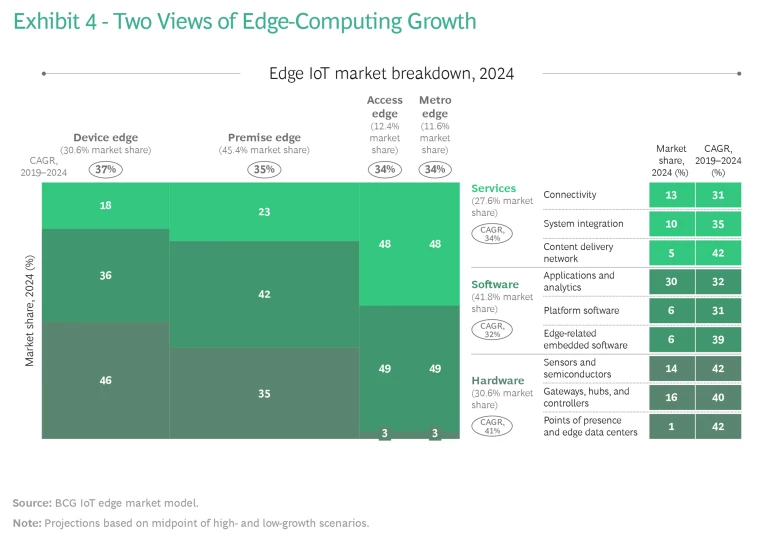

The overall IoT market is expected to continue its strong growth, doubling from 2019 to 2024 and driving significant growth in the edge IoT market. As more uses cases and new technologies emerge, we expect the edge to grow by 35% annually and the top edge use cases to represent over 20% of the IoT market in 2024, compared with less than 10% in 2019. (See “Our Methodology.”)

Our Methodology

Most current use cases depend on computation and storage capabilities in or close to the device that increase speed or reduce dependency on connectivity. Accordingly, the device edge and the premise edge currently make up about 75% of the market. Beyond 2024, as 5G and other advanced networks roll out, we expect growth in the access edge and the metro edge to accelerate.

If the edge is viewed as a stack of services, software, and hardware, each of these layers is likely to grow by at least 30% a year. The applications and analytics sublayer will continue to be the largest slice of the market through 2024, while the hardware layer is likely to be the fastest growing. (See Exhibit 4.)

Where the Edge Will Be Hot

The edge will complement the cloud but not replace it. In fact, the edge depends on cloud infrastructure. But edge computing has the benefits of low latency, better reliability, potentially improved security, lower cost, and greater convenience, which give companies a powerful incentive to move some of their processing to the periphery. (See “Why the Edge Will Be Hot.”)

Why the Edge Will Be Hot

- Low Latency. The cloud is too far away from the action for many uses. Self-driving cars, for example, will require most real-time computing to happen at the edge.

- Reliable Connectivity. The cloud can be too unreliable for 24/7 uses, such as connected medical devices, or in places that are subject to poor connectivity, such as remote oil rigs.

- Improved Security and Privacy. The cloud has fallen victim to data security and privacy breaches. In manufacturing 4.0, companies can process and store data daily on the edge and rely on the cloud for more periodic algorithm training. This hybrid model is especially attractive in regulated industries such as health care and banking.

- Lower Bandwidth Cost. The cloud can be too expensive for bandwidth-heavy uses such as video streaming. This is what led to the creation of content delivery networks, one of the first uses of edge computing

- Greater Convenience. The cloud will increasingly become a less convenient option as edge processing units become cheaper and more efficient through fanless chip sets and other breakthroughs.

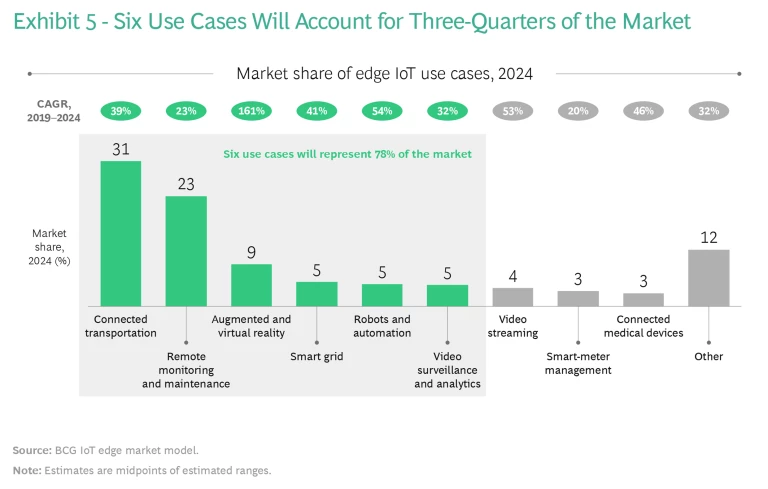

By mixing and matching these five benefits in various combinations, companies can add capabilities that are more efficiently provided on the edge. We anticipate that six use cases will likely account for more than three-quarters of the edge computing market in 2024. (See Exhibit 5.) The first two of them will be far larger than the rest.

- Connected Transportation. This includes private vehicles, public transit, trucks, and bicycle and scooter sharing.

- Remote Monitoring and Maintenance. Manufacturing 4.0 depends on low latency, high reliability, and security. Remote monitoring and maintenance are likely to grow by 23% annually, powered by a wide range of customers. Many large manufacturers are already fairly advanced in automation and are pioneering edge architectures built around real-time machine-learning algorithms. Other companies with legacy assets are much less advanced in adoption but are laying the groundwork for rapid growth.

- Augmented and Virtual Reality. Proponents of augmented reality and virtual reality have overpromised and underdelivered for years, so skepticism is to be expected. However, intelligence at the periphery could unlock AR use cases in retail, manufacturing, or health care and unleash consumer VR products. We project this segment to be the fastest growing, partly because it is starting from such a small base.

- Smart Grid. The smart grid—connected power plants, infrastructure, and systems used for outage detection and energy routing—is one of the most mature components of the edge, especially in developed markets.

- Robots and Automation. Driven by manufacturing 4.0 and advances in machine learning, robotics and automation depend on both human-like latency and always-on connectivity. The edge can help ensure both.

- Video Surveillance and Analytics. Remote video cameras are inexpensive, but sending live video streams to the cloud can be expensive. By processing data within the device or on premises, the edge can help lower costs and reduce latency.

Technologies with meaningful benefits are not preordained to win. The successful integration of technology into large organizations with legacy hardware and software, uneven digital skills, and established business practices is never a given. It will take hard work for the edge to win a meaningful place in corporate computing. (See the sidebar “What Could Hold Back the Edge.”)

What Could Hold Back the Edge

- Business Barriers. The business case embedded in a use case can be more complex to create than is often apparent. Executives need to both understand the technical benefits of edge computing and translate them into business opportunities that fit within the company’s larger IoT and digital strategy.

- Technological Barriers. The edge stands apart from the cloud but is dependent upon it. To successfully deploy edge architecture, companies need a cloud architecture that can efficiently manage different types of edge computing, aggregate data, and train and deploy algorithms. Many companies are still early in their cloud journey. Even worse, many companies still rely on legacy architectures and systems and on siloed data.

- Human Barriers. People are often the most important ingredient in the success or failure of technology. The edge is no different. Companies need the right cloud, IoT, edge, and data science skills. Just as important, they need executives conversant in both technology and business.

How the Battle Is Shaping Up

The edge is attracting the usual suspects: technology vendors seeking to extend their current product line and startups looking to break into a high-potential market. These aspirations are drawing on companies’ core strengths and building new ones. The natural approach is to seek to build an ecosystem, given that the sweet spot of edge combines capabilities in hardware, software, and connectivity that are hard to pull together within a single company.

Public Cloud Providers. The edge is a natural extension for these platforms, combining the cloud’s computing and storage capacity with the edge’s hardware and connectivity into a “hybrid cloud.” Cloud providers are investing outside their core by following three approaches. They are extending their businesses vertically into hardware and chips, partnering with other companies to create ecosystems, and taking advantage of their scale to continue their horizontal expansion.

Microsoft, for example, is expanding into edge-enabled hardware such as sensors and gateways. Its Azure Sphere chips, developed with hardware partners, include a built-in Microsoft security and operating system. Microsoft has also entered the connectivity layer of the stack by acquiring Affirmed Networks.

Hardware and Chip Manufacturers. These companies have a natural and nearby opportunity to develop sensors, gateway, and other devices for the edge. Some of this equipment, such as oil wells and farm implements, will be installed in harsh conditions in the field—potentially new environments for manufacturers.

The edge also gives them an opportunity to move upstream into industry-specific applications and platforms, taking advantage of the AI processing capabilities of new chips. The Qualcomm Vision Intelligence platform, for example, is built around systems on a chip that run intensive video workloads, such as AI-enabled surveillance and facial recognition.

Hardware manufacturers will likely need to utilize both hardware and software to compete against public cloud providers and cooperate with them in developing ecosystems. Getting this balance right will be key.

Industrial Goods Companies. These companies are pursuing approaches similar to those of hardware manufacturers. They are embedding edge capabilities into their products and expanding into applications and platforms by working with existing customers and partners. Their success depends on their ability to demonstrate that they have the software capabilities, either in-house or in partnership with others, that the edge requires. These companies may have a narrow opportunity to build end-to-end solutions, a strategy being deployed by Tesla, the electric-car maker.

Content Distribution Networks. CDNs have been in the edge business longer than most companies. They have an opportunity to move beyond their core capability of caching video streams to offer other services, such as cloud management and security for customers. The rollout of 5G will create additional opportunities to provide local-access computing capabilities close to the edge. CDNs have natural ecosystem or partnership opportunities with telecom operators.

Telecom Operators. While operators have struggled to make money from IoT, the rollout of 5G could fundamentally change their trajectory. They will build business cases around such technologies as mobile edge computing (placing servers near 5G cell towers), narrowband IoT (a low-power networking technology), and ultrareliable low-latency communication (for mission-critical uses such as remote surgery and self-driving vehicles). Operators also have an opportunity to partner with public cloud providers and others to create edge ecosystems. Verizon, for example, has partnered with Amazon Web Services in Boston to offer ultra-low-latency services, while AT&T is working with HPE on multiaccess edge computing that brings the cloud closer to devices.

Startups. The venture community has been actively investing in the Internet of Things and edge computing—specifically, in companies offering applications and analytics that provide convenient solutions and are easy for customers to adopt.

Samsara, a startup with about $1 billion in funding, has created an end-to-end solution to connect the operations of fleets, equipment, and warehouses. Its cloud platform uses sensor data and an open API to provide analytics and insights into operational efficiency, safety, and sustainability. Its edge-powered AI dash cam, for example, detects distracted or aggressive driving, tailgating, and rolling stops to minimize accidents.

More than five years ago, our colleague Philip Evans described a world where “sensing, connectivity, and data merge into a single system,” where “every person and object of interest is connected to every other,” and where “the world and our picture of the world are becoming the same thing: an immense, self-referential document.” Edge computing brings us closer to that world. The battle between tech and telecom companies is still taking shape. The companies that bring that intelligence-everywhere world to life will emerge triumphant.