Appendix: Detailed Methodology

The focus of this report is to assess the economic benefits of the public cloud across the APAC region, while identifying key learnings and best practices that can be employed in order to unlock these benefits. We conducted both qualitative and quantitative studies to develop the findings in this report.

Analysis Conducted

Qualitative: Qualitative assessment through Interviews

The qualitative research conducted as part of this report took the form of in-depth interviews with senior IT and business leaders in order to understand their perspectives on the public cloud. BCG researchers interviewed over 80 industry experts, policy experts and senior leaders from each of the six markets, representing digital native businesses (DNBs) alongside all key industry verticals such as education, banks and financial services, manufacturing, media and gaming, public sector, retail and consumer, systems integrators and telecommunications.

Among the key questions discussed were the evolution of spending and use cases being deployed on public cloud, key benefits and challenges faced during deployment of public cloud in the organization, and the steps taken to mitigate the challenges. Other focus areas included how decision makers predict that spending on public cloud would evolve, and the newer use cases and applications of interest for their organizations on public cloud in the near future.

Quantitative: Quantitative assessment through Surveys and Econometric analysis

Three kinds of quantitative analysis were used: quantitative assessment through surveys; detailed econometric models to assess the impact of public cloud deployment in each of the six markets; and scenarios analysis to assess the impact of various drivers for public cloud adoption.

1. Quantitative assessment through surveys

A survey of senior IT and business decision makers asked them to verify the hypothesis established through the qualitative interviews, and share their perspectives on the public cloud. The survey covered questions about the key benefits and challenges in their business due to deployment of public cloud, relevant use cases of interest, and the most pressing concerns from a regulatory perspective.

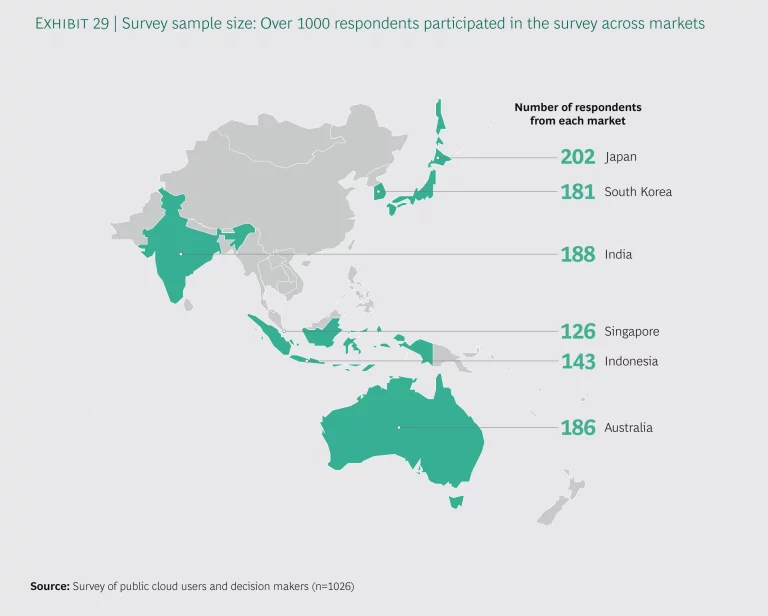

Over 1,000 respondents from across the markets answered the survey questions (See Exhibit 29). Respondents included business leaders and IT decision makers, including chief technology officers, chief information officers, and chief data officers who are responsible for technology spending.

The respondents came from verticals in a range of industries that included financial institutions such as banks and insurance, internet startups and digital native businesses, manufacturing, retail and wholesale, healthcare and life sciences, public sector agencies, educational institutions, telecommunications, media and gaming, and information technology.

2. Econometric model to assess the impact of public cloud deployment

Using input from the interviews and surveys, we developed an overall econometric model using input-output table methodology to assess the impact that use of the public cloud by the relevant industry verticals would have upon GDP and employment growth in each of the six markets.

Econometric modeling methodology

We utilized publicly sourced data, with additional inputs from our interviews and surveys, which we combined with our analysis to arrive at the estimated impact that spending on public cloud service is likely to have upon the six selected economies (Australia, India, Indonesia, Japan, Singapore, and South Korea) over the five year period of 2019-2023.

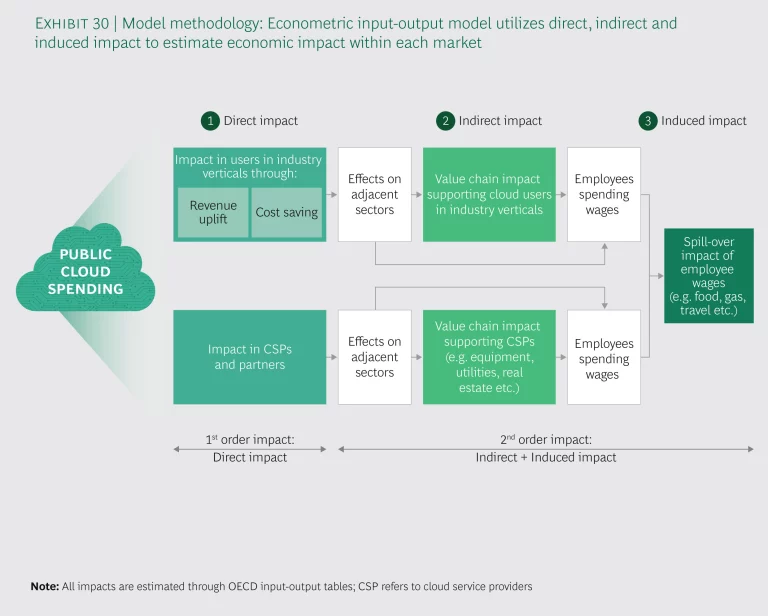

We began by breaking down the impact into direct, indirect, and induced impact. This was followed by an analysis of all three of these categories of impact from the perspectives of both cloud services providers and cloud users in various industry verticals (See Exhibit 30). BCG has used this methodology in multiple economic impact assessment studies earlier (See Capturing the Data Center Opportunity, Digital Infrastructure and Economic Development). It is a globally recognized and accepted methodology combining rigor and practicality.

Direct Impact

As noted, our estimation of the direct impact produced by public cloud services spending comes from two main segments—cloud service providers and cloud users in industry verticals.

Direct impact is the impact that can be approximated as the product of public cloud service spending, domestic supply, and public cloud value-added ratio. Data is obtained and synthesized from various sources, including but not limited to industry and market reports, publicly available financial data, Organization for Economic Cooperation and Development (OECD) statistics, and expert interviews and surveys.

The calculation can be further segmented into four sources of direct impact: digital business creation, revenue uplift, cost savings in IT functions, and cost savings in core business and non-IT functions or the productivity benefit. While the first two sources incur indirect and induced impact, cost savings would have no further spillover effect.

• Digital Native Business: Estimated as the product of the size of the digital native business economy, public cloud attribution, and value-added ratio of profits and salaries.

• Revenue Uplift: Estimated as the product of public cloud service spending, revenue uplift per cloud spend, and value-added ratio of profits and salaries.

• Productivity Benefit: Estimated as the product of public cloud service spending and non-IT cost savings per unit of cloud spending.

• IT Cost Reduction: Estimated as the product of public cloud service spending on replacement of traditional IT spending and IT cost saving as compared to that of non-public cloud.

Indirect and Induced Impact

In order to capture the full economic impact of cloud services spending, we also need to look at two categories that reflect the spillover effects from the direct impact: indirect and induced impact.

• Indirect impact: Also known as supply chain impact, this is the impact created by the direct suppliers of the public cloud users as they, too, spend money on their supplies.

• Induced impact: This is the impact generated in industries such as retail and travel as a result of the increase in total household income created by the establishment of new business.

To quantify both the indirect and induced impacts of public cloud services, we leveraged the commonly-used econometric model using OECD input-output tables. This helped us identify the relations of inter-industry and inter-sector transactions, i.e. how many units of each sector’s output are required to produce a unit of another sector’s output. With the input-output tables sourced from OECD and other national statistics authorities, we were able to assign the indirect and induced multipliers that result when cloud service providers and cloud users in industry verticals increase their spending in other sectors of the economy.

Similar to the approach we took in measuring direct impact, we looked at two main segments for indirect and induced impact as well: cloud service providers (inclusive of their partners) and cloud users in various industry verticals. With inputs from each industry category and their respective value-added multipliers, we were able to apply the values accordingly to our models.

3. Scenarios analysis to assess the impact of various drivers for public cloud adoption

To define a base scenario, we used inputs from interviews and surveys to characterize each of the six markets by their current status in terms of public cloud deployment and penetration, organizational adoption and regulatory frameworks. We then analyzed the impact that would occur if any of these conditions were to change in ways that either accelerated or constrained public cloud adoption, using the resultant data to construct, respectively, a Big Bang Growth Scenario in which the economic impact would surpass the Baseline Scenario, and a Sluggish Growth Scenario that would result in a lower impact than the Baseline Scenario.

Scenario methodology

Three steps were used to estimate the economic impact under the three different scenarios:

Step 1: Define the conditions for Big Bang Growth, Baseline and Sluggish Growth Scenario for each market. We start qualitatively by constructing the potential growth drivers and inhibitors for each of the six selected economies. These narratives are country and context specific.

An archetypical baseline case entails the current natural progression, with policymakers adhering to their current stance and cloud service providers keeping their current pace of product launch. For the Sluggish Growth case, we envision more policy restrictions, less cloud-native talent and limited cloud uptake by both industry verticals and the public sector, while the opposite would occur in a Big Bang Growth case.

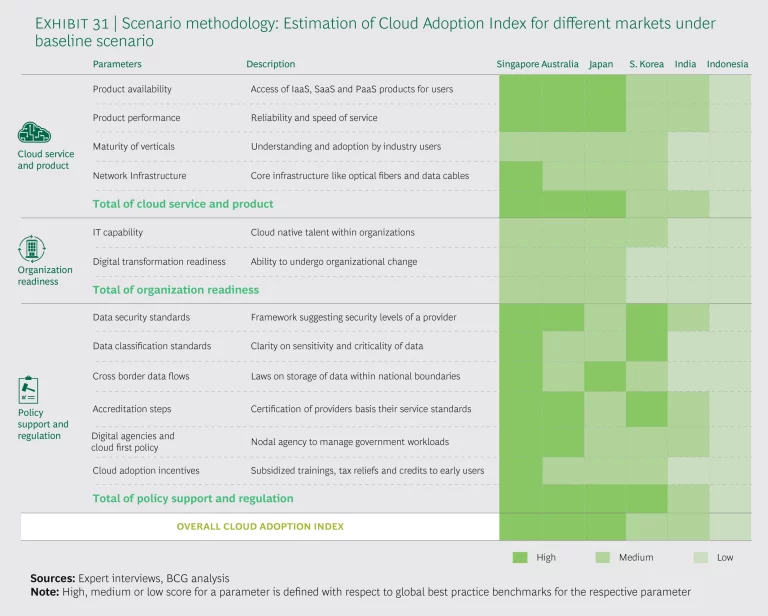

Step 2: Apply a cloud adoption evaluation framework to each market to assign an index score to different market conditions. We fed these qualitative scenarios into 12 metrics that are clustered into three groups: cloud service product, user organization readiness, and policy and regulatory support. With quantification, we are able to estimate a Cloud Adoption Index for each metric in accordance with the prevailing market conditions in the baseline scenario and the expected condition in each of the other two scenarios, and calculate a weighted overall cloud adoption index for each scenario for each country (See Exhibit 31).

Step 3: Translate the score into model assumptions. We regressed the cloud adoption index over the cloud market size as a percentage of GDP to estimate the cloud market size in 2023 under different scenarios. Consequently, we were able to estimate the range of CAGR under the three different scenarios for each country.

Projecting the market size under each of the three scenarios and the expected percentage of public cloud spend for growth applications, we estimated the economic impact and level of job creation using the econometric model.

Currency assumptions

All $ numbers mentioned in this report to US$. In analyzing the economic impact for Japan and South Korea, we have provided localized currency values using SK₩ (South Korean won) and JP¥ (Japanese yen) for the respective markets. This conversion is based on a five-year average currency exchange rate between the local currency and the US dollar (US$). For South Korea, that exchange rate is set at US$1 = SK₩ 1190. For Japan, that exchange rate is set at US$1 = JP¥ 110.