“COVID-19 is climate on warp speed,” said Gernot Wagner, a climate economist at NYU. Indeed, both trends show exponential growth—in infected people and CO2 emissions, respectively—while the capacity to fight them remains limited. The consequence is simple: a significant risk of sudden overwhelming, be it of the health care system or of our collective ability to manage consequences for the environment.

In both cases, we are aware of mechanisms to prevent or at least ease adverse effects. Bill Gates, among others, highlighted back in 2015 the necessary elements of preparedness to avert a global pandemic. And humanity is aware of the need to reduce CO2 emissions and remove excess CO2 from the atmosphere. But while governments enforce emergency measures around the globe in response to the pandemic, little action on climate has been taken. Therefore, the question is not “What can we do?” but “Why not now?”

As happened with the ozone depletion crisis, a top-down approach with supranational coordination might have addressed climate inaction. But the latest UN Conference (COP 25) resulted in few action-oriented outcomes. And the current lack of alignment among countries in the fight against COVID-19 shows the unlikelihood of a globally coordinated government response to climate change. A bottom-up approach—through financial incentives to adjust behaviors, like carbon pricing—has not been fruitful to date, either. We need an alternative, rigorously structured approach to finding practical and truly effective solutions. We used the concept of Smart Simplicity, successfully applied to solving complex problems in business and beyond, to explore a new approach to climate change inaction. (For a description of Smart Simplicity and its relevance to climate change, see “Applying Smart Simplicity to Climate Inaction.”)

Applying Smart Simplicity to Climate Inaction

Applying Smart Simplicity to Climate Inaction

Too often, our efforts to address complex problems—creating new structures, processes, systems, scorecards, committees, layers—are counterproductive. These traditional management techniques can turn complexity into “complicatedness.” BCG research has found that the organizations that deal successfully with complexity don’t focus on structures and procedures but instead on context and on the ways people interact within it. They consider why people do what they do, and then they seek to change that context.

We used this approach, which BCG calls Smart Simplicity, to explore the actions that could help address the complex problem of climate inaction. Smart Simplicity is based on insights from multiple disciplines, such as economics, organizational sociology, and game theory, and is governed by two principles:

- First, behaviors should be analyzed as “rational strategies” that people deploy within a context of problems they are trying to solve, of resources they can mobilize, and of constraints they must sidestep. This is the legacy of Nobel Laureate Herbert Simon’s notion of “bounded rationality”: the idea that individuals make decisions that are rational within the limits of their individual knowledge. In the case of climate change, people might base purchasing decisions on a rationale (such as a quality-to-price ratio) without considering how their decisions relate to other elements of the system.

- Second, individuals’ behaviors can become aggregated into collective outcomes that may not be what the individuals intended. Therefore, it is important to understand how individual behaviors influence and compound with one another. This idea stems from the work of Nobel Laureate Thomas Schelling. In the case of climate change inaction, the efforts of individual companies to demonstrate good management practices (prioritizing efficiency ratios or increasing short-term shareholder returns) lead to unintended collective outcomes, such as the inability of an industry to shift to renewable energy.

The exhibit below lays out how we have applied the “six simple rules” of Smart Simplicity—rules that help us understand the context and enlist integrators in helping to change it—to the complex problem of climate inaction.

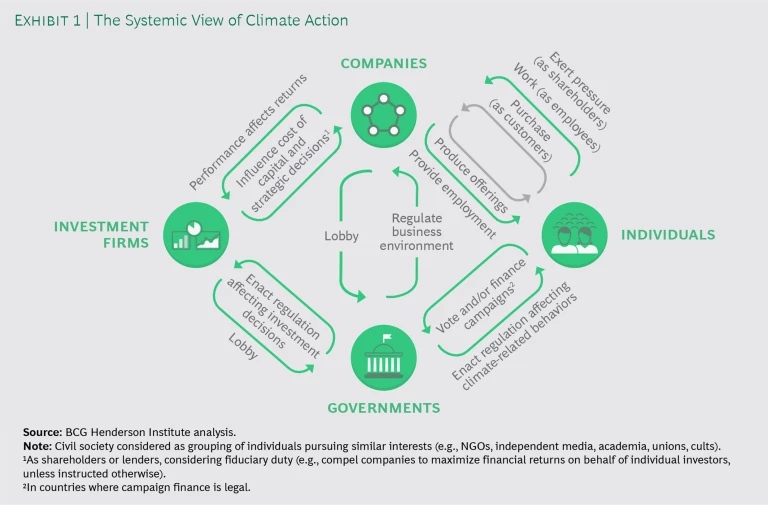

Two Views of Climate Inaction

As a complex problem, climate change inaction needs to be looked at from both strategic and systemic angles. From the strategic view, individual behaviors can be analyzed as “rational strategies” that are deployed by people within a context of problems they are trying to solve, with resources they can mobilize and constraints they have to cope with. From the systemic view, one can analyze how individual behaviors combine to produce collective outcomes that cannot directly be traced back to individual motives.

Climate change is a societal challenge, hence it is critical to understand how a collective construct perspective influences the way actors (individuals, government leaders, corporate leaders, investors) behave, combine with, and influence one another. (See Exhibit 1.)

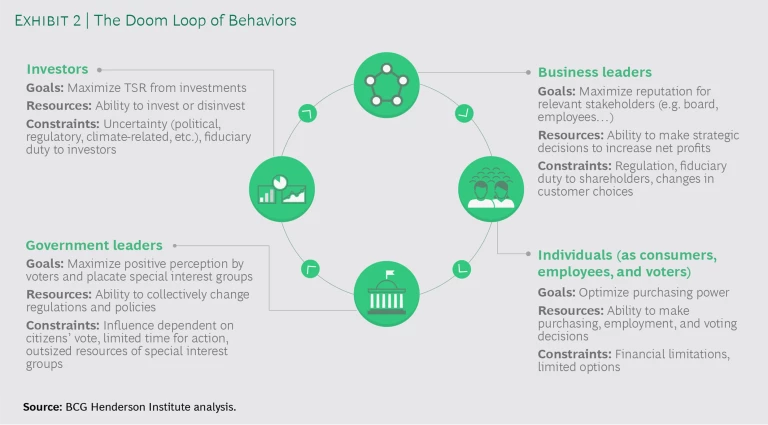

We Are Stuck in a Doom Loop

Looking at climate change from the systemic angle, we can see that current behaviors are negatively influencing one another while having a negative overall impact on climate change. Today, fossil fuels are cheap and easily available, and there is no requirement to assess rigorously the risk of climate-related impacts on companies’ assets and business models. Hence, most companies today have little rationale to adopt environmentally friendly measures, such as manufacturing with green energy or limiting superfluous travel. Family businesses with a multigenerational time horizon may be the exception here. In addition, the overall growth in aggregate demand for energy driven by the overall growth of the population aggravates this even further.

As a direct consequence, consumers face higher prices in many product categories when they seek to make climate-friendly purchases, like an electric car or energy-saving home upgrades. One may argue that the COVID-19 crisis could encourage more-sustainable habits, yet we may see a further polarization of consumption driven by health fears and consequences of the economic downturn. For example, car traffic in China was back to normal a few days after the end of the lockdown, while the use of public transportation remained low.

So, for now, companies can maintain investors’ returns with legacy nonsustainable business models, and investment firms do not have any incentive to adjust their portfolios to favor environmentally friendly companies. And this cycle goes on and on. (See Exhibit 2.)

Government could play a central role in addressing this inertia, as it has the power to shift regulations across the industries that are most essential to reaching the goals of the Paris Agreement. However, the ability to exert this influence is constrained by political dynamics—notably, by vested interests through campaign finance, lobbying, and efforts to galvanize opposition to action on climate change.

As a result, when governments introduce ESG regulations, they focus especially on financial institutions, like Article 173 of the French Energy Transition Law. There is a reason for this: acting on investors’ portfolios can indirectly influence other industries, albeit with more limited impact, while preventing direct effects on end customers, who are also voters. Indeed, when individuals are anxious about their purchasing power, it is difficult for them to advocate for climate-friendly regulatory changes. All of this generates a paradoxical situation: in the era of increasing grassroots mobilization of individuals on climate change (millions of people show up to march for climate action, for instance), we still see policy inaction. Regulatory capture by special interest groups is part of the explanation, but the “end of the world vs. end of the month” dilemma for lesser-privileged people is another.

A recent illustration of this is the election of a climate-skeptic politician in Australia just a few months before an environmental catastrophe. In contrast, in places where climate change was already a significant concern for citizens, like in California, legislation had been amended following voters’ will. However, overall, governments tend to postpone policy updates on climate: even France, in spite of significant contributions during the treaty design, has not achieved its COP 21 target, partially because of the Yellow Vests’ advocacy against an increase in fossil fuel taxes. All this strengthens investment firms’ belief that returns from non-climate-friendly companies are not at risk.

Creating a Virtuous Cycle

Still, there is room for hope: individuals—for example, within top management teams in companies—are the ones who drive these organizations, within their fiduciary duties. Therefore, the first step to unlock action is to understand individual behaviors using the strategic view.

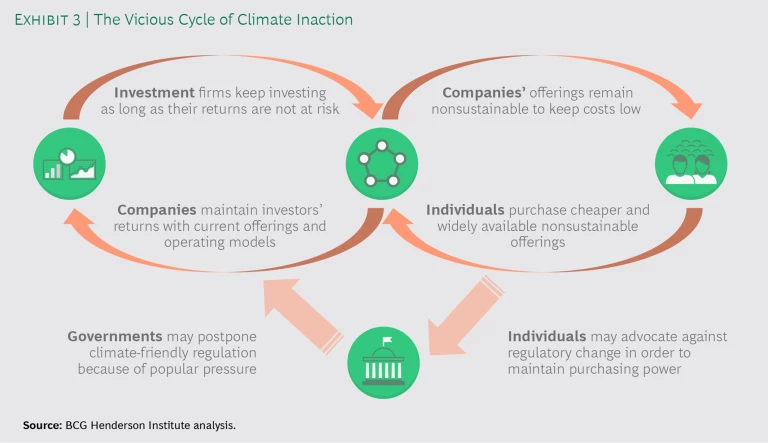

Step 1: Understand the Rationale for Individuals’ Actions

In talking about individuals’ behavior, “rational” does not mean “selfish” or “utilitarian.” According to social sciences analyses, rationality is considered relative to a context of individual goals, resources, and constraints. Exhibit 3 helps us understand why individuals do not act in ways that break the doom loop.

Ultimately, the mass adoption of climate-friendly behavior can happen only when most customers have access to widely available sustainable purchase options at an equivalent price per quality as nonsustainable ones. This typically takes time even with significant government incentives, as it did for electric vehicles in Norway.

This is why immediate action to start and accelerate this process is critical, and integrators are the keys to unlock it.

Step 2: Identify the Right Integrators to Trigger Action…

Today, climate change is an externalized adjustment cost of uncooperative behaviors: those causing climate change generally do not bear its worst consequences. Instead, the cost is externalized onto third parties, be it the next generation or the fraction of citizens in exposed areas, like in the Maldives or US coastal regions. Behaviors will change only if this cost becomes a constraint for those who generate it; and this is where “integrators” come into critical play. Integrators are actors in the ecosystem that can make other agents change behavior and cooperate. They can do so because they combine two characteristics: a personal interest in making other agents change and a capacity for action, based on knowledge and influence. In the climate change problem, we identified three potential integrators as worthy of focus: institutional investors, young talents, and environmentally conscious customers.

Institutional Investors. These integrators have an interest in seeing other actors change. Indeed, even if long-term value creation is the top priority for 63% of investors, according to a 2020 BCG survey, institutional investors have long time horizons. Research shows they hold an investment for an average of approximately five years, and they are increasingly shifting portfolio allocation toward direct private equity investments. This means that climate-related uncertainty, typically visible over the longer term, affects them negatively because the performance of their portfolio is driven by the valuation of assets in it—some of which are at risk from climate change, from regulatory and/or physical standpoints. In fact, the Bank of England estimates that climate change could affect as much as $20 trillion of assets. In addition to a strong interest in addressing climate change, institutional investors have a strong potential for influence, considering the approximately $100 trillion in assets under management. If they were to adjust their investment according to climate impact, companies and governments would bear the cost (or, rather, pre-emptively try to avoid it).

Institutional investors have two levers at their disposal. The first is their ability to increase the cost of capital to firms, especially to those whose business models will become less financially viable as the world moves toward greater action on climate. As lenders and investors reduce their exposure to these companies, their cost of capital will increase. Still, this is not an overnight shift—when responsible investors step away, less responsible ones will likely step in.

The second lever is their influence with management teams, which they can use to encourage changes to business models. Public blaming, such as Blackrock’s criticism of Siemens for its environmental record in February 2020, is one tactic, but investors may use a range of influencing models, like proxy voting and coalitions, to work collaboratively and constructively with firms. Again, this is not an immediate shift, and when responsible investors pull out of these sectors, less responsible ones generally take their place.

Young Talents. These integrators are aware of the tangible impacts of climate change, believe they will likely bear the cost of climate inaction in their own lifetimes, and have significant influence over companies as current and potential employees. Indeed, they can make firms bear the cost of climate inaction by prioritizing environmentally friendly firms in their employment decisions—a bold move, considering that many businesses face a talent shortage. Already, around 40% of millennials have chosen a job because of the employer’s sustainability record, according to a 2019 survey in the US. This may seem like a large group, especially compared with the employment choices of previous generations, yet there is still a 60% majority not taking action in this way.

Around 40% of millennials have chosen a job because of the employer’s sustainability record, according to a 2019 survey in the US.

Environmentally Conscious Customers. As buyers of products and services, such companies and individuals have the power to purchase climate-friendly offerings, sometimes even if those are more expensive than the alternatives. Customers’ actions along these lines have multiple amplifying effects: they push product and service providers to develop environmentally friendly offerings, they finance companies’ experience curves, and they can serve as inspirational benchmarks and examples for other firms, both within and beyond their industry. Today, only a fraction of buyers (governments, companies, and individual consumers) base purchasing decisions primarily on environmental impact, hence they have no effect on companies’ (sellers’) valuations. However, as soon as this fraction gets large enough, these buyers will become a prime determinant of market value. And such a shift can happen abruptly, as it did when coal industry multiples dropped suddenly in the US in 2008.

One may ask if governments and multilateral institutions could serve as integrators. As of now, they cannot. Central banks, for example, have a long-term view yet no direct means of influencing regulation beyond fiscal policy. Supranational organizations lack a clear interest in change. For example, the WTO could champion the creation of a Climate Club that would impose significant sanctions on nonparticipants, as suggested by Nobel Prize winner William Nordhaus, but such a step could be at odds with the organization’s mandate to facilitate global trade.

We strongly believe that the combined actions of the three integrators would increase companies’ willingness to invest in developing novel sustainable solutions. This would help climate-friendly options achieve enough scale to be affordable to the mass market. Albeit driven by different motives, a recent illustration of this process is the financing of the learning curve in solar panel development by German citizens, which ultimately turned this technology into a viable replacement for diesel generators in some areas.

… and Start a Virtuous Cycle of Behaviors

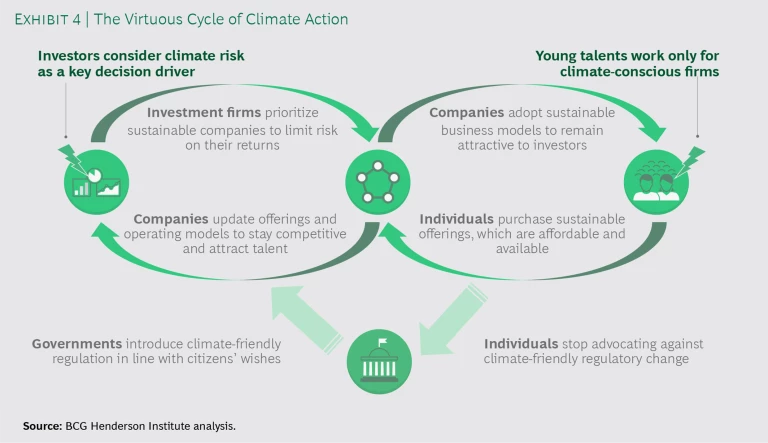

To understand how integrators can provoke dramatic change on climate action, we need to return to the systemic view. Indeed, the tighter the vicious cycle, the more dramatic the effect, in both speed and scale, of breaking that cycle. All the forces that preserved the current equilibrium are instantly reversed. Looking systemically, the integrators activate the virtuous cycle of climate action by reinternalizing the cost of uncooperative adjustments in the system.

This virtuous cycle is sketched out in Exhibit 4. Once investors know the extent to which a company’s business model is vulnerable to climate change—this is the key tipping point—all will have to take this into account in their NPV calculations. As a result, companies that make non-climate-friendly decisions will not be favored by investors. Thus, firms have an incentive to become more sustainable, especially from a production standpoint (such as adopting renewable energy), even though this may hurt their short-term financials. Companies that adjust their operating models then attract not just investors but also environmentally conscious customers and young talent.

As companies move up the learning curve, climate-friendly production becomes cost-competitive, and sustainable offerings become the norm. This benefits all customers by making obsolete the tradeoff between the short term (optimize purchasing power) and the long term (ensure the planet is livable for future generations). One must note that, in parallel, wealthy individuals—not necessarily prone to the “end of the month vs. end of the world” dilemma in the first place—can act as an additional accelerator by adjusting their purchasing behaviors toward climate-friendly options, even while those are still more expensive.

Companies are thus pushed to focus on developing climate-friendly options to remain attractive to customers and maintain returns for their investors. This itself strengthens the rationale for investment firms to prioritize sustainable investments in their portfolio. And in this way the cycle continues.

In this new dynamic, government influence can significantly increase because there is no tradeoff between citizens’ and consumers’ priorities. Policymakers can increase their effort to regulate the financial industry, driving reporting regulations and ensuring transparency for investors. As financial institutions typically abide by the law, and sometimes help shape it, this can have a very positive snowball effect on other industries. And as the availability of affordable climate-friendly options grows, citizens’ advocacy against regulatory changes should decrease. Governments can thus plan to update regulation and enforce climate-friendly behaviors (such as disincentivizing CO2-intensive activities and banning certain items) with full buy-in from citizens, while investment firms should in turn welcome such change.

Step 3: Ensure That Integrators Start Acting Now

While young talent is already influencing companies to act on climate change, the immediate priority should be to catalyze investors’ intervention. This requires increasing both their knowledge and their influence, at two levels: across investment firms, to ensure that all are considering climate in their portfolio management practices (by, for example, making strong commitments to carbon neutrality) as well as within investment firms, to ensure all investment managers abide by this change. Leading investors have started moving in this direction, as demonstrated by Blackrock CEO Larry Fink’s 2020 letter to CEOs, which states that “Climate Risk Is Investment Risk.” Yet there is potential for much more.

Investors need climate-related information that aligns with their goal (and fiduciary obligation) to maximize TSR. They need robust evidence that climate-friendly investment decisions have a net positive impact on the financial performance of their portfolios. As Frédéric Samama made explicit during his March 2020 testimony before the US Senate’s Special Committee on the Climate Crisis, “Traditional backward-looking risk models do not capture future risks. We need to work with new models.” Indeed, investors need access to accurate, standardized information, especially on physical risks (financial losses due to the increasing frequency and severity of climate-related weather events, for example) and vulnerability to transition (such as the uncertain financial impact of changes in regulation or in social norms that may result from a rapid transition to low-carbon energy sources).

An important first step here would be companies’ adherence to principles laid out by the Task Force on Climate-related Financial Disclosures (TCFD). Indeed, in line with the logic of Smart Simplicity, TCFD can turn the vicious circle into a virtuous one. The faster companies coalesce around this standardized disclosure of climate-related indicators—by, for example, publishing them in annual reports—the sooner their climate actions will be rewarded more fully by investors. Why? By adhering to TCFD principles and respecting this commitment, firms increase transparency into the environmental impact of their activities, which in turn helps shareholders identify and reward climate leaders. Once enough companies are participating, TCFD can significantly reshape investors’ expectations, potentially leading to significant capital reallocation across asset classes. All this happens while further empowering other valuable ESG frameworks. For example, indicators disclosed as part of TCFD could even be leveraged to develop a “climate risk rating” for firms and countries, and allow for stress tests of companies’ climate resilience, inspired by DNB’s energy transition stress tests for financial institutions in 2018. And such additional initiatives would further encourage the flow of capital to companies that are the most transparent and doing the most to address climate change.

Investors thus have a key role to play in engaging with policymakers and regulators to ensure that disclosure schemes meet the requirements of investment analysis, and in leading joint investor actions (like Climate Action 100+, which includes more than 450 investors with over $40 trillion in assets under management) to build self-regulating guidelines for companies and assets in their portfolio. As a concrete example, the UK-based Investment Association has set a three-year deadline for companies to explain in their annual reports how they plan to measure and manage the threat of global warming.

All this novel information should allow investors to monitor their portfolios’ environmental score on a set of predefined metrics, like emissions targets, and monitor correlation with ROI. This change in mindset is also the key to unlocking financial innovation to support sustainable capital market growth. For instance, when Amundi launched the AP EGO fund, it monitored not only the fund’s financial performance but also its impact in meeting the United Nations’ Sustainable Development Goals (SDGs).

To complement such firmwide and industry-wide initiatives, individual investment managers within firms must be activated as well. As a prerequisite, they must understand the importance of climate in portfolio valuation, and they must be aware of climate-friendly and rarely used financial instruments, such as green bonds. For current investors, this education can happen within their firm; for future investors, it should be happening in educational institutions. The IFC’s partnership with the Stockholm School of Economics is a concrete example of how to overcome knowledge gaps, yet programs like this remain rare.

Investment firms need to change many of their practices to ensure that they can transform their knowledge into influence.

In parallel, investment firms need to change many of their practices to ensure that they can transform their knowledge into influence. Providing concrete KPIs and incentives at the portfolio level is a key step to ensure adoption of climate sustainability in portfolio management. For example, firms can set strategic climate targets (such as carbon reduction targets) for their entire portfolio, including all investing and financing activity. The individual investment manager’s contribution to the target can be assessed and linked to a performance bonus, within the constraints of the type of portfolio managed (such as geography or industry). In addition, it will be critical to anchor climate accountability all levels, business units, and regions within the investment firm, enforcing it with cross-functional taskforces, for example.

Finally, investors can use innovative structures to drive sustainable actions in their portfolio companies. For example, the coupon of the first sustainability-linked bond, introduced in 2019 by the Italian company Enel, was tied to the firm’s reaching at least 55% of its installed capacity in renewable energy sources by 2021. If the goal is not met, the coupon will increase until the bond matures. This was a success: it was oversubscribed by a factor of three, enabling Enel to expand its investor base.What Now?

In early 2020, before the COVID-19 crisis erupted, significant announcements were made, most of which would have been unthinkable a few months before. Investors (Blackrock’s CEO letter), businesses (Amazon’s Jeff Bezos pledged $10 billion to fight climate change), and governments (Orban’s official commitments to climate in Hungary in late January, driven partially by the election of a “green” mayor in Budapest) are starting to move. Still, this is not enough, and the pandemic must not be an excuse to postpone climate action. Recent news is concerning, such as reports that funds from a COVID-19 recovery package have been allocated to the coal industry in Canada, in spite of a pledge for a Green New Deal for the government only a few months earlier.

Still, we are convinced, there is hope. Beyond the urgent need to tax carbon emissions—which will adjust prices, impact corporate profitability, and support redistribution to the lesser privileged in order to “fuel” a fair energetic transition—social sciences tells us that more- dramatic change is possible. And it requires two simultaneous conditions: a doom loop of uncooperative behaviors and the existence of integrators to shift toward a virtuous cycle. Luckily, climate change abides by the definition: hence, paramount rapid change is possible, provided we immediately take focused actions to influence the most influential integrator: institutional investors. Although there is no guarantee the expected shift will happen overnight, it can only generate beneficial outcomes for the environment. And the cost for humanity of not succeeding would be high. Unlike COVID-19, the climate “pandemic” will not peak (there is no “herd immunity” to climate change), but we do know the vaccine (stop CO2 emissions) already.

The BCG Henderson Institute is Boston Consulting Group’s strategy think tank, dedicated to exploring and developing valuable new insights from business, technology, and science by embracing the powerful technology of ideas. The Institute engages leaders in provocative discussion and experimentation to expand the boundaries of business theory and practice and to translate innovative ideas from within and beyond business. For more ideas and inspiration from the Institute, please visit our website and follow us on LinkedIn and X (formerly Twitter).