Global Asset Management 2014: Steering the Course to Growth is The Boston Consulting Group’s twelfth annual worldwide study of the asset management industry. Our research found that asset managers in 2013 finally recorded their second consecutive—and strongest—year of solid growth since before the crisis. Global assets under management rose to record levels, profits were strong, and net new flows made solid gains.

Global Asset Management 2014

- Steering the Course to Growth

- Differentiation Begins with a Target Operating Model

- Insurers Attack the Target-Operating-Model Opportunity

The results reflected the expansion of a real recovery from the year before, when the industry finally returned to growth after four years of inertia, as we noted in Global Asset Management 2013: Capitalizing on the Recovery. This was the case particularly in most developed markets, where asset growth gathered speed even as growth slowed in many emerging markets.

Yet, as this year’s report makes clear, now is not the time for complacency. Asset growth continues to be largely the result of rising equity prices on global financial markets. Net flows remain a modest part of total growth, and most of those new flows go to specialists, solution providers, and nontraditional asset managers. The global profit pool remains under pressure, while net revenues lag below the peaks achieved before the financial crisis.

As traditional actively managed core assets remain vulnerable to the market’s evolution, the future for all types of managers looks increasingly complex, costly, and constrained by waves of regulation. Managers need a long-term strategy that anticipates those changes.

For all these reasons, developing the right target operating model is crucial for steering a course to profitable growth.

A target operating model—beyond boosting efficiency—can provide the blueprint that managers need to unlock cash and free management attention for product innovation, entry into new asset classes, and development of client relationships. We believe it is a key to flexibility, scalability, and profitable growth.

This report, like its predecessors, is the product of comprehensive market-sizing research. We covered 43 major country markets (representing more than 98 percent of the global asset-management market) and focused exclusively on assets that are professionally managed for a fee. We also analyzed the external forces shaping the fortunes of asset management institutions worldwide.

In addition, this report includes insights drawn from a 2014 benchmarking study of more than 120 leading asset managers—representing 53 percent of global AuM. Our aim was to collect data on fees, products, distribution channels, operating systems, and costs in order to gain insights into the current state of the industry and its underlying drivers of profitability.

More than a decade after BCG’s first annual Global Asset Management report, the breadth of our market-sizing research and benchmarking studies has expanded. The goals of the report, however, remain steadfast: to probe beneath the surface of the market’s evolution, identify trends, and provide insights that help managers build strong and prosperous paths to the future.

A Snapshot of the Industry

The asset management industry has achieved its strongest year of growth since the onset of the financial crisis.

For the second consecutive year, in 2013, the value of professionally managed assets rose to a record high. Net asset flows recorded their strongest postcrisis gains—also for the second year in a row.

Industry profits surged to $93 billion, and profits as a percentage of revenues made gains.

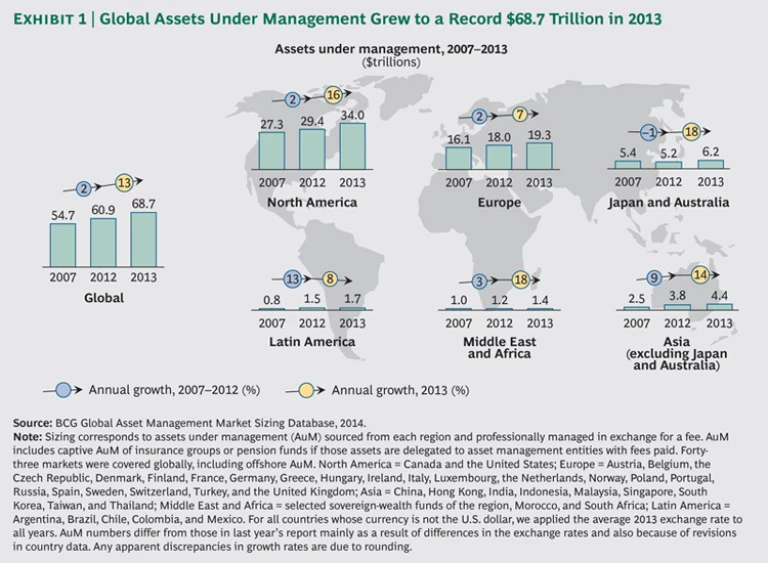

Managed Assets Rise to a Record $68.7 Trillion

Total assets under management (AuM) increased 13 percent to a record $68.7 trillion in 2013, after rising 11 percent to $60.9 trillion in 2012. By comparison, AuM stood at $54.7 trillion in 2007, the year before the financial crisis began. (See Exhibit 1.)

That said, most AuM growth in 2013 represented increased asset values produced by the global surge in equity markets, rather than new asset flows. Still, new asset flows recorded their strongest postcrisis gains for the second year in a row. They increased to 1.6 percent of prior-year AuM, up from 1.2 percent in 2012. By comparison, precrisis gains ranged from 3 to 6 percent. Net flows in 2013 were driven foremost by retail investors’ revived interest in rising equity markets, as well as by the continued resilience of institutional investors. Retail net flows averaged 2.5 percent of AuM, and institutional flows reached 0.9 percent, compared with 1.8 percent and 0.8 percent, respectively, the year before.

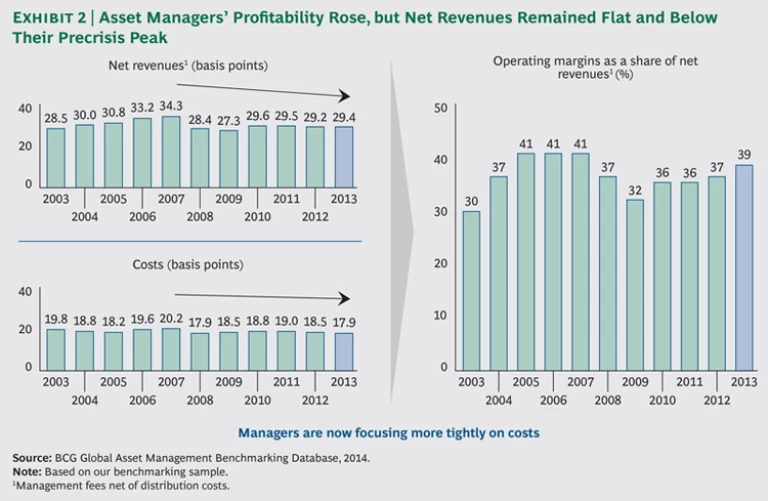

Asset management continues to rank among the most profitable industries. Operating margins, or profits as a percentage of net revenues, grew from 37 percent in 2012 to 39 percent, approaching the precrisis high of 41 percent, as costs grew less quickly than revenues. Indeed, in basis points—or on an asset-adjusted basis—net revenues remained relatively flat and below their peak while costs decreased from 18.5 basis points to 17.9 basis points. (See Exhibit 2.)

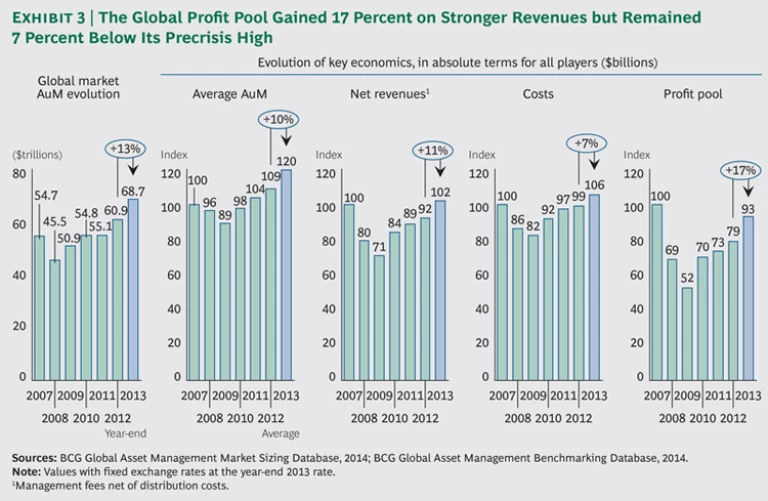

Profits in absolute terms grew to $93 billion in 2013, a 17 percent rise from $79 billion the year before. Despite this advance, the global profit pool still lagged about 7 percent behind its historic peak, before the crisis. Revenues have grown more slowly than assets, the victim of lower-than-historic revenue margins due to the shift away from higher-margin products and increased price pressure in some product categories. Since the crisis, costs have risen faster than revenues. Revenues were 2 percent higher in 2013 than in 2007, but costs were 6 percent higher. (See Exhibit 3.)

The “Two Speed World” Shifts to Multiple Speed Lanes

Asset management’s two-speed world shifted to multiple speed lanes in 2013. AuM growth slowed in many emerging markets, gathered speed in most developed markets, and advanced robustly in other emerging markets, particularly in Asia and in the Middle East and Africa. On average, AuM grew 14 percent in emerging markets and 13 percent in developed markets, compared with 18 percent and 10 percent, respectively, in 2012. As a result, developing markets did not expand their global share in 2013 and represent roughly 9 percent of AuM, compared with 6 percent in 2007.

Viewed regionally, AuM growth varied widely in 2013. In North America, the Middle East and Africa, Japan, Australia, and Asia, it increased from 14 percent to 20 percent. Europe and Latin America averaged 8 percent and 7 percent, respectively. As with AuM growth globally, growth regionally was driven largely by equity market performance. Differences in market performance were the main source of regional variation.

Net new asset flows also varied widely among developed markets, as they did among developing markets.

In most developed markets, net flows ranged from 1 to 2 percent. However, they reached 3 to 5 percent in Japan, Canada, and the Nordic countries—and even higher in Italy and Spain, driven by revived retail interest. At the same time, net flows were negative in Benelux and France.

In developing markets including Latin America, Eastern Europe, and Asia, and excluding Japan and Australia, net flows represented 4 percent. In the Middle East, net flows reached 8 percent.

Five “New New Normal” Trends Affecting Asset Managers

Despite recovery from the crisis and rising profits, asset managers continue to navigate the financial industry’s turbulent structural shifts. The challenge—for them and for other financial-services companies—is exacerbated by a new new-normal environment of heightened global competition, rapid change, and restricted room to maneuver.

We have identified five disruptive trends that asset managers must take into account in this environment: regulatory change, the digital and data revolution, more demanding investors with a growing preference for nontraditional assets, new competitors providing nontraditional assets, and globalization.

Regulatory Change. Since the onset of the financial crisis, all global financial institutions have been confronted with a tsunami of regulatory tightening and public pressure for change. Tightening regulations affect asset managers as well as clients and distributors, requiring managers to continually adapt to new rules in multiple markets. Greater compliance burdens increase operational complexity and pose strategic challenges on issues ranging from product innovation to international growth—for example, meeting regulatory reporting requirements in a new market. Asset managers must be able to build, evolve, and scale new functionalities in an accelerated way, typically within months—not years, as in the past.

The Digital and Data Revolution. At first glance, asset managers may seem less exposed than wealth managers to the escalating impact of digitization. Wirehouses, retail banks, independent financial advisors, and insurers are all expanding their use of digital channels and platforms.

Yet digital technologies and data innovation are quickly transforming operational aspects of asset management, becoming sources of competitive advantage.

Our research revealed a rapid increase in electronification. Among our benchmarking participants, 96 percent of equity trades were managed electronically in 2013, compared with about 90 percent in 2011. In fixed-

income and money market trading, 86 percent of trades were managed electronically in 2013, compared with 75 to 80 percent in 2011.

The benefits of more advanced enterprise-wide data management in particular have become an increasingly critical focus for asset managers. This became evident in our study of the data management practices of our benchmarking participants in four dimensions: organization and governance, advanced analytics and modeling capabilities, data definitions and standards, and processes and infrastructure.

Most participants cited the significant potential for improved data-management practices. In particular, they noted the benefits of migrating from current practices of local management divided among silos to more enterprise-wide management and sharing.

This evolution allows for greater companywide integration and optimization of investment strategies, portfolio analytics, business processes, and data usage.

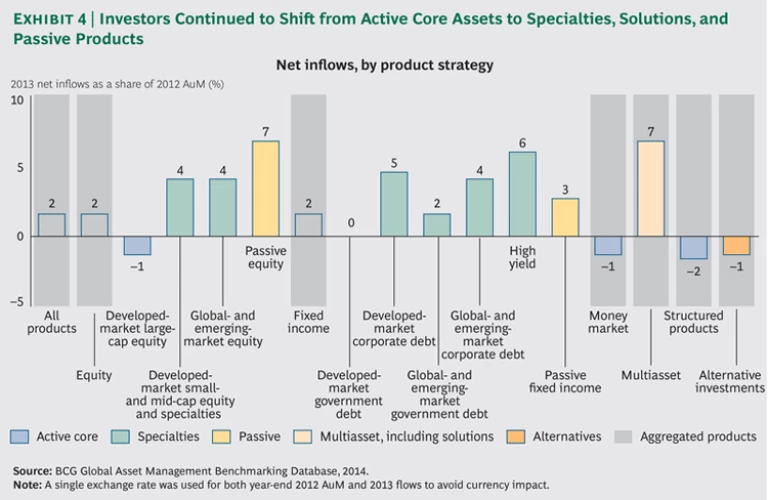

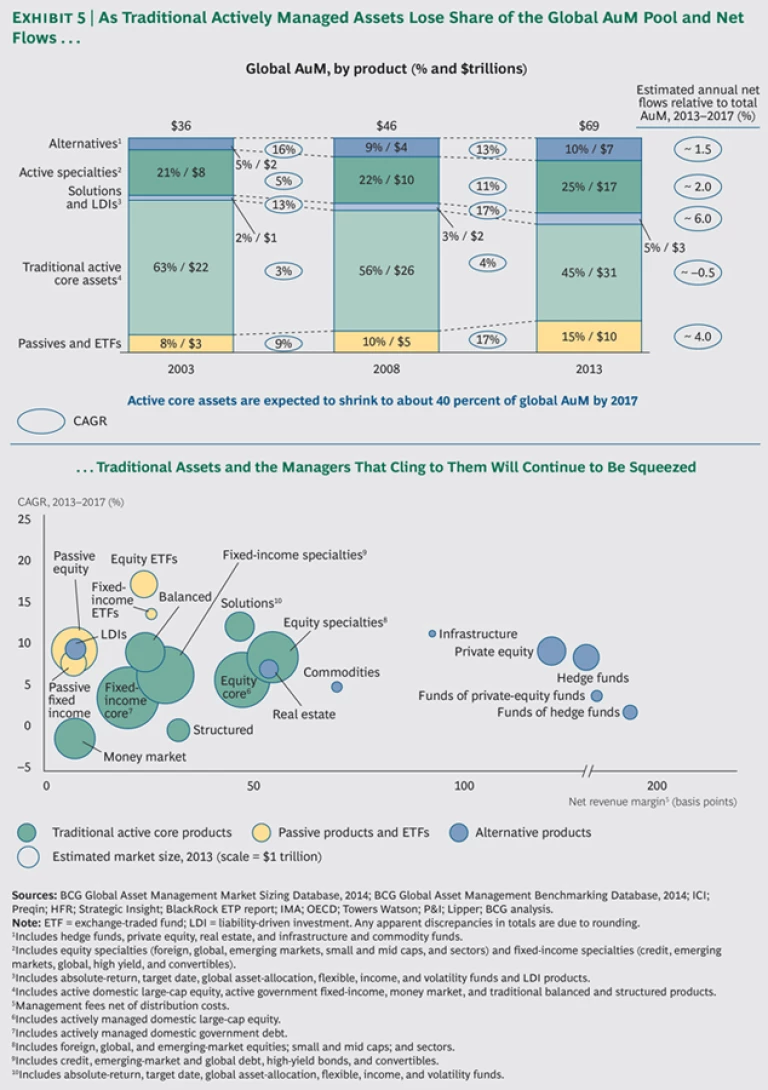

More Demanding Investors with a Growing Preference for Nontraditional Assets. Persistently lower interest rates and a shift in investor preferences have boosted the growing appetite for specialties, solutions, multi-asset capabilities, and passive products. Investors have become more demanding and more likely to prefer particular outcomes or solutions that are specifically oriented to their needs, beyond performance relative to a benchmark. (See Exhibit 4.)

The market shift away from actively managed core assets continues to erode the share of traditional assets in the global AuM pool—which was 45 percent in 2013, compared with 56 percent in 2008—and among net flows. The continuing rapid advance of solutions and specialties in 2013 confirms a structural shift in the market. Managers that cling exclusively to traditional assets will continue to be squeezed. (See Exhibit 5.)

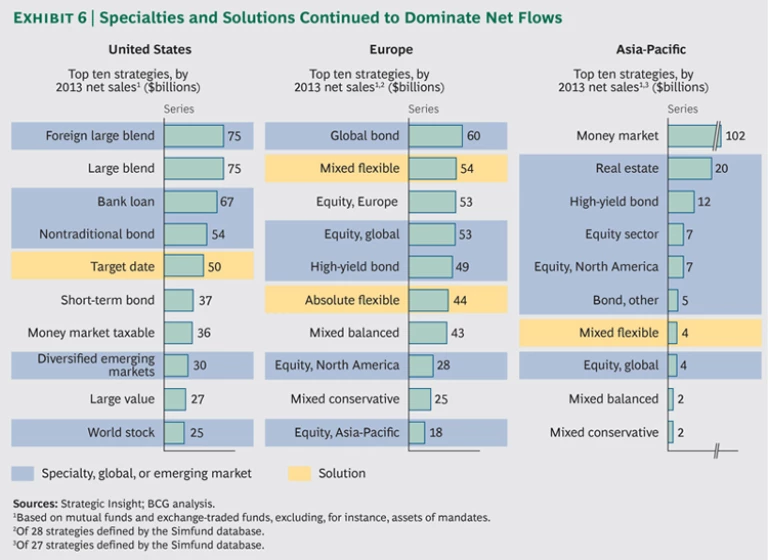

The demand for specialization and solutions in 2013 was again evident in the ranking of mutual-fund product strategies that received the highest net flows. In the U.S., the top ten strategies included specialties such as foreign large-blend funds, bank loans, nontraditional bonds, and solutions such as target date funds. In Europe, the strategies included specialties such as global bonds, global equity, high-yield bonds, and solutions such as flexible and absolute-return funds. (See Exhibit 6.)

This ongoing shift in investor preferences helped maintain the industry’s winner-takes-all trend again in 2013, although it has begun to slow, particularly in Europe. (See Exhibit 7.) The top ten managers, in mutual-fund net flows in the U.S. and Europe, captured 73 percent and 42 percent, respectively, of all net new asset flows, compared with 94 percent and 51 percent in 2012.

The trend is driven partly by the higher concentration of competitors in specialties and passive products, compared with the slower-growing traditional products, as noted in Global Asset Management 2013: Capitalizing on the Recovery. It is not surprising that out of the top ten fund providers in 2013, seven had already been among the top ten in either 2011 or 2012 in both the U.S. and Europe.

Tougher competition is raising the bar on service, as customers become more demanding. Asset managers need to shift their focus from selling products to solving client problems—addressing, for example, the growing demand for yield or retirement income—on both the institutional and retail sides. Institutional investors are demanding greater transparency, which requires more flexible real-time data and analytics, and the ability to demonstrate stronger risk-management skills.

Enhanced competition also means continued pressure on fees. We observed a drop in fees after the crisis, as both the product mix and the business mix shifted. Lower-margin prod-ucts such as fixed-income and passive prod-ucts grew more quickly, and the institutional share of business grew faster than retail.

In 2013, overall revenues rose by only 0.2 basis points—from 29.2 to 29.4—despite the retail segment’s slightly faster growth than the institutional segment, the strong market impact in equity rather than the negative impact overall in fixed income, and strong net flows in product categories such as specialties. Examining fee evolution by product and client segment, we observe some fee decrease in equity (both active and passive), money market, and structured products and also alternatives (especially hedge funds). Fee pressure will not abate as a result of the regulatory push toward more transparency and bans on commissions, as well as increasing power and concentration in distribution.

New Competitors Providing Nontraditional Assets. A structural shift in products is under way, to the detriment of traditional managers. More and more, providers of nontraditional assets are serving traditional clients. Most hedge-fund, private-equity, infrastructure, and private-debt business is still provided by specialized alternative managers. Traditional managers are now investing in and slowly building the specific capabilities required for these new product categories. But building those capabilities will take time. Meanwhile, the alternative-product providers are expanding into products historically provided by traditional asset managers—for example, specialties—and taking advantage of the relationships and reputation they have built in alternatives.

Globalization. We see more global competitors and more global products in the new new normal. Demand for greater diversification has helped accelerate globalization, as investors increasingly seek exposure outside their home markets.

U.S. and UK asset managers, in particular, have succeeded in growing significantly beyond their domestic markets. This is especially notable in continental Europe, where strong specialty capabilities have helped U.S. and UK asset managers advance, while local managers have lost market share.

The AuM of continental European managers in 2013 did not regain levels achieved in 2007, even though continental European AuM reached $13.8 trillion—15 percent above its 2007 level. Meanwhile, UK managers’ overall AuM grew 50 percent while their domestic market grew just 32 percent.

Global competitors also keep investing in developing markets: even if those markets are still small, they offer higher medium- to long-term growth prospects.

Presence in multiple markets—whether through manufacturing or distribution—creates operating-model complexity. Asset managers must adapt their product offerings to local regulations, distributors, and the needs of local investors. We are seeing development of shared-operations platforms across regions with specialization by function: the goals are to achieve scale and enable managers to operate in smaller markets with more promising growth prospects. The global scale and complexity of a multicountry organization require a carefully designed operating model.

A Target Operating Model for the New New Normal

After four years of stalled recovery, the global asset-management industry has finally recorded two consecutive years of solid growth. Global AuM has risen to record levels, profits are strong, and net new flows have achieved solid gains, albeit from a small base.

At the same time, AuM growth for traditional managers has largely been the product of rising equity prices. Net new flows remain a modest part of total AuM, and the lion’s share goes to specialists, solution providers, and nontraditional asset managers. The profit pool remains under pressure, as net revenues stay flat and lag below their precrisis peaks.

Meanwhile, as traditional active core assets continue to lose share, navigating a differentiated growth path looks increasingly competitive, complex, costly, and constrained by waves of regulation.

For all these reasons, developing the right target operating model is crucial for asset managers if they are to steer strategically, safely, and efficiently.

Acknowledgments

First and foremost, we would like to thank the asset management institutions that participated in our current and previous research and benchmarking efforts, as well as the other organizations that con-tributed to the insights contained in this report. In addition, we want to thank Gaicha Saddy for her research expertise.

Within BCG, our special thanks go to Eric Bajeux, Nacer Bengelloun, Frieder Hack, Jérémy Haziza, Rodrigo Reynel, Cristina Rodríguez, and Andrea Walbaum. In addition, this report would not have been possible without the dedication of many members of BCG’s Financial Institutions and Insurance practices, in particular Jay Venkat, Martin Ouimet, and Achim Schwetlick.