Over the past four years, The Boston Consulting Group has published a series of industry reports on chemical distribution.

METHODOLOGY

Suppliers of chemicals can outsource sales to three types of players: third-party distributors, agents, and traders. In our market analysis, we defined the chemical distribution market as the gross revenues of third-party distributors.

This definition excludes direct distribution from chemical suppliers, as well as net revenues through agents and traders. (Some third-party distributors obtain a small portion of their revenues as agents, yet that amount is assumed to be negligible.) Physical market sizes are defined in terms of the country or region in which the chemicals are consumed or processed.

Market sizes are shown in nominal euros. In order to show underlying growth, we have corrected market growth rates for exchange rate effects using Economist Intelligence Unit (EIU) average annual exchange rates, with fixed rates as of 2008.

For our analyses, we used data from the following sources among others: Chemdata International; Verband der Chemischen Industrie; European Chemical Industry Council; “Manufacturing,” by Oxford Economics; EIU, for foreign exchange rates and industrial production change; World Input-Output Database; American Chemistry Council; Eurostat; United Nations Industrial Development Organization; ICIS; Orbis; and companies’ annual reports, websites, and filings with the U.S. Securities and Exchange Commission.

In general, the chemical industry can be categorized into commodity and specialty segments. Commodity chemicals are produced (and consumed) in bulk, with relatively transparent pricing and minimal variation among suppliers. By contrast, specialty chemicals are typically produced in smaller volumes and are, in many cases, proprietary formulations that customers use in specific applications. These categories, though, are not black and white; changes in the life cycle of chemical products lead to a gray zone.

In practice, this is a spectrum with multiple potential operating models for each segment. To develop the segmentation used in our reports, we have classified approximately 175 chemical products and product groups.

Market Context

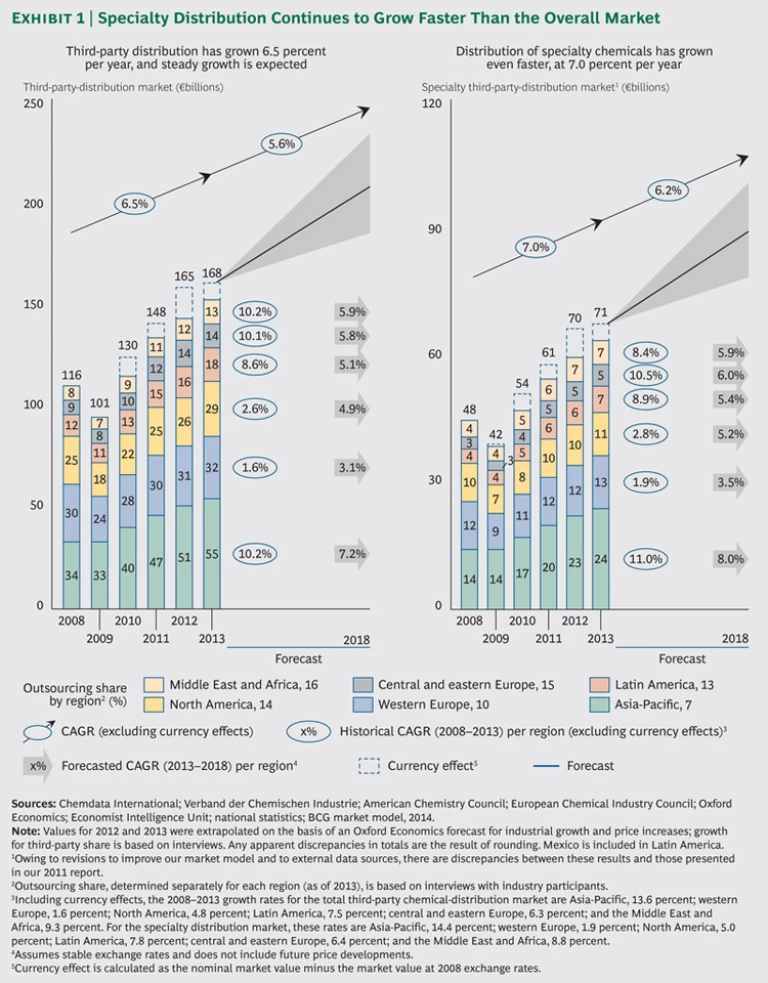

The chemical distribution market continues to grow. From 2008 through 2013, the compound annual growth rate (CAGR) was 6.5 percent, resulting in an overall market size of approximately €168 billion as of 2013. The overall market-growth rate is driven mainly by the underlying growth of chemical consumption, which averaged 4.4 percent during the same period. Furthermore, the share outsourced to third-party distributors grew from 9.1 percent in 2008 to 9.7 percent in 2013.

Chemical distribution is growing fastest in emerging markets. In some regions—particularly emerging economies—the distribution market has expanded more rapidly than others. For example, growth rates in the Asia-Pacific region, the Middle East and Africa, and central and eastern Europe all averaged around 10 percent from 2008 through 2013, followed by Latin America at 8.6 percent.

Currently, a significant part of Asia’s chemical-distribution market is only partially accessible to Western distributors. In many cases, local suppliers work with captive distribution subsidiaries or local relationships. However, we expect the Asian market to become professionalized, making it even more accessible to Western distributors. Asian distributors with a trading heritage, such as Sinochem International’s distribution subsidiary, are also developing their capabilities through international supplier relationships that will strengthen their position in Asia’s third-party-distribution market (primarily in China).

Specialty chemical distribution is outpacing overall market growth. Third-party distribution of specialty chemicals grew 7.0 percent annually from 2008 through 2013 to a total market size of €71 billion in 2013 (compared with a 6.2 percent CAGR and a €97 billion market size for commodity distribution). That outpaced the 6.5 percent CAGR in the overall market. (See Exhibit 1.) The force behind the higher growth rate for the distribution of specialty chemicals relative to commodity chemicals is the underlying growth of the end markets. For example, from 2011 through 2013, European specialty-heavy markets such as pharmaceuticals (6.1 percent annual growth in total production), food (4.0 percent), and personal care (4.7 percent) grew at higher rates than European end markets that rely more on commodity chemicals, such as coatings (0.7 percent), wood and wood products (2.0 percent), and machinery (3.1 percent).

Growth in the specialty segment is driven mainly by volume, and price increases are less of a factor. The pricing of specialty chemicals is based primarily on the added value to the customer—less on raw-material prices. Therefore, apart from general inflation, structural price trends are much less relevant; in the medium term, prices are driven by the life cycle of specialty chemical products. Furthermore, distributors of specialty chemicals typically carry a broad range of products, serving the needs of many different end markets. Given this, standard volume-versus-price-split analyses are not applicable. By contrast, prices of commodity chemicals are typically more volatile and move in tandem with underlying macroeconomic growth, supply-demand balances in specific markets, and oil prices.

The regional patterns of the industry as a whole are reflected in specialty chemical distribution as well. The market grew fastest in the Asia-Pacific region (11.0 percent from 2008 through 2013), followed by central and eastern Europe (10.5 percent), Latin America (8.9 percent), and the Middle East and Africa (8.4 percent). The growth in mature markets is comparatively slower: 2.8 percent in North America and 1.9 percent in western Europe.

Continued market growth is expected, but it will be slightly slower. The third-party- distribution market will likely continue to grow as the chemical industry expands. Further growth of underlying chemical consumption worldwide will remain critical. The growth rate will, however, slow slightly (to 5 to 6 percent per year), largely owing to a flattening of growth rates in chemical consumption in China, which represents approximately 30 percent of global chemical consumption, and other emerging markets. An increase in the growth rate is expected only in North America and western Europe, driven by the ongoing economic recovery in these regions.

Specialty distribution will continue to outpace the overall market for two reasons: continued strong growth of the underlying end markets and suppliers’ greater reliance on third-party distributors to gain access to small clients in local regions and to secure the knowledge required to serve customers in specific application domains.

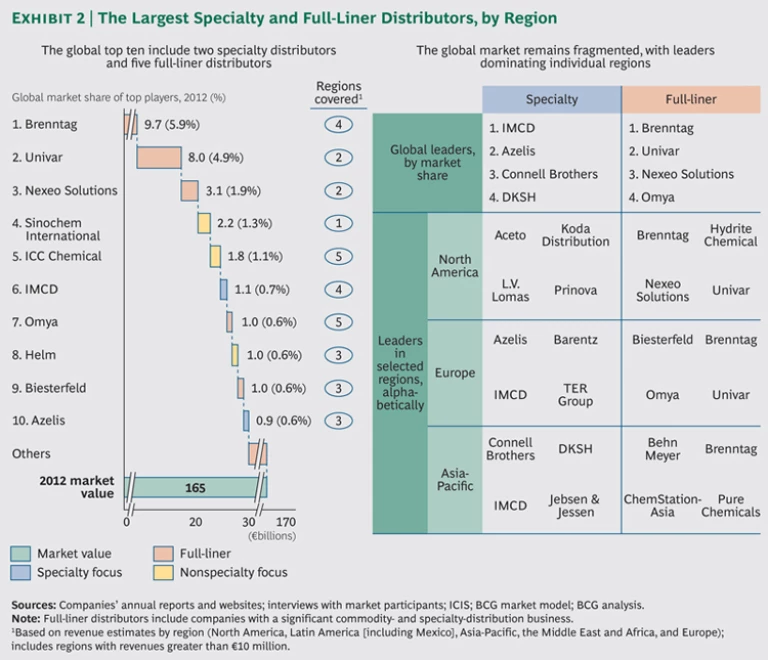

The distributor landscape remains highly fragmented. The chemical distribution market is characterized by fragmentation, which is most pronounced in emerging markets: in the Middle East and Africa and the Asia-Pacific region, the top three players collectively hold 6 to 10 percent of the market. By contrast, in North America and Europe, the top three players hold 30 to 40 percent and 15 to 20 percent, respectively. As shown in Exhibit 2, Brenntag is the clear global leader in the mixed-model segment, which includes both specialty and commodity chemicals. Companies in this category are also called full liners. In the specialty segment, IMCD and Azelis hold leading positions, but they are significantly smaller than Brenntag.

More and more, suppliers are professionalizing their sales-channel strategy, rationalizing their distributor base, and strengthening the management of individual distributors. Suppliers are developing more sophisticated distribution-channel- management models in order to reduce structural costs and deepen their product knowledge regarding specific applications. They are increasingly focusing their direct sales on large strategic clients while outsourcing distribution to smaller clients. This effect is strongest in the specialty segment, given the more challenging aspects of market access and the segment’s need for more technical knowledge. Suppliers, which expect that this trend will lead to further rationalization of their distributor bases, aim to focus on a small group of large distributors. Furthermore, they indicate that they intend to professionalize the way in which they manage their distributors.

Selected distributors have outgrown the market by combining organic growth with selected acquisitions. Successful players combine organic growth with acquisitions to fill gaps in their regional footprint and product lines. For example, Brenntag made 28 acquisitions from 2008 through 2013, IMCD made 20, and Univar, 6. (See Exhibit 3.) These offered a basis for above-market organic growth through cross-sales of products from the extended supplier base.

Further consolidation of distributors is likely. Chemical distributors are expected to continue targeting inorganic growth to build out their product portfolios and extend their regional coverage. Further professionalization in emerging markets will increase demand for panregional third-party distributors, which will replace in-house supplier activities and local distributors and will, therefore, act as a catalyst for inorganic growth. This is particularly true in the specialty segment, in which exclusive contracts between suppliers and distributors—specifically with respect to “anchor products”—are an important mechanism (as described in the next section). Such contracts might limit the potential attractiveness of M&A targets if, for example, an acquisition led to conflict among several suppliers working with the same distributor.

The Suppliers’ Point of View: Distribution Excellence Is Critical

In a recent article, BCG described how optimizing sales force effectiveness represents a significant opportunity for most companies.

On the basis of the interviews conducted for this study, we found that suppliers are currently at different maturity stages relative to distribution excellence. Some have well-developed models that capitalize on the strategic role of outsourcing partners. Other suppliers rely on ad hoc, bottom-up decisions made by local business units, with little coordination across the enterprise. To achieve distribution excellence, chemical suppliers need a more coherent approach across all channels, comprising three components: developing the distribution channel strategy, selecting the right distributors and the right distributor-interaction model, and professionalizing distributor management.

Developing the Distribution Channel Strategy. Structural cost-effectiveness is the main reason chemical suppliers should use third-party distributors. Suppliers should consider structural distributor relationships when a specific set of customers in a specific market segment can be served more cost-effectively through third-party distribution. Whether to outsource is not a simple yes-or-no decision. Instead, it requires assessing whether particular components of the distribution value chain—such as marketing and sales, technical support, and supply chain activities—should be retained in-house or outsourced in order to reduce costs and complexity.

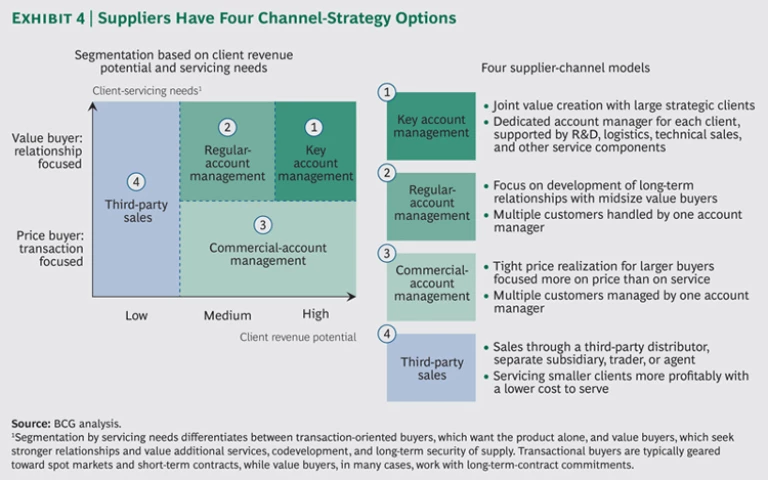

Designing the right channel strategy is critical. Suppliers need to segment the client portfolio, looking at both revenue potential and servicing needs. In this endeavor, they require an objective evaluation of the expected revenue potential and the priorities and needs of individual clients. On the basis of this evaluation, they can segment the optimal structural-channel strategy into four models. (See Exhibit 4.)

- Key account management is the desired model for large clients that represent strategic priorities for the supplier. The focus lies on cooperative value creation between suppliers and clients.

- Regular-account management is the model of choice for midsize value buyers, focusing on the development of long-term relationships with these clients.

- Commercial-account management is aimed at tight management of price realization for midsize to large price buyers.

- Third-party sales models should be used for smaller clients. These include price and value buyers in both the specialty-heavy and commodity-heavy client groups. On average, however, there will be more value buyers among specialty-heavy clients. Third-party sales models include third-party distributors, in-house distribution subsidiaries, traders, and agents. It is worth noting that over time, third-party distribution becomes increasingly cost-effective because rising in-house marketing and sales costs, in many cases, cannot be offset by efficiency improvements.

Suppliers can also use third-party distributors to obtain the coverage required to develop specific markets and segments in the short to medium term. Third-party distributors can provide an inroad to a specific market segment in which the supplier lacks sufficient market coverage. A lack of regional access is most typical for emerging markets in which suppliers may not have on-the-ground operations and must adhere to local regulatory constraints. Additionally, suppliers often lack application knowledge to serve highly specialized market segments such as oil and gas companies.

If a supplier falls short in terms of either regional presence or market insights, it will have to invest both time and money to scale up. In this situation, third-party distribution may be the most attractive option. It offers immediate market access, which could lead to greater growth in the target market. Third-party distribution also limits the need for suppliers’ one-off investments, allowing suppliers the possibility of preserving margins. In this model, the supplier-distributor relationship matures over time: once the business is at scale, the supplier and the distributor should reassess the role of the distributor in the market.

Selecting the Right Distributors and Developing the Right Distributor-Interaction Model. Suppliers should periodically review their sales-channel strategy. By actively monitoring the distributor landscape, suppliers can ensure that they team up with strong distribution partners. In assessing the distributor universe, suppliers should look at all relevant parameters, including performance to date (in terms of financial strength, market share, and growth projections), breadth of operations (number of salespeople, warehouse space, and product portfolio), number of customers and the segments they are in, historical relationships with suppliers, and the distributor’s strategic outlook (including potential opportunities and threats).

Suppliers should also periodically evaluate the alternatives for their current distributors—including the possibility of bringing outsourced distribution in-house. This requires adopting a longer-term view of how the distributor landscape will evolve and identifying future winners. In other words, suppliers should create a plan B for each distributor. Actual switching rates will be limited by sizable barriers such as historical investments in joint business development, strong relationships of a distributor with a specific client base, and required investments in, for example, logistics and training.

Suppliers should strive to rationalize their distributor base over time. Once a supplier clarifies its thinking on the critical future distribution partners, it should seek to rationalize the distributor base. In doing so, a supplier can focus on a smaller number of larger distribution partners. A number of suppliers in our study indicated that rationalization was indeed part of their plan for the future.

There are two distributor-interaction models. The right interaction model for a supplier and a distributor is one that aligns incentives for both organizations, ensuring that the distributor operates in line with the commercial interests of the supplier. Broadly, there are two approaches: mutually exclusive partnerships and a multidealer model (in which a supplier works with multiple distributors for a given product).

Mutually exclusive partnership models are generally applicable when the third-party distributor offers specific expertise and structural cost advantages. Such partnerships are most commonly used for specialty distribution, which requires intensive product knowledge and in which market access can be more challenging. In many cases, the mutually exclusive aspects of such arrangements stipulate information transparency between the two sides, agreements on revenue targets, and rules for the transfer of customers (when order size exceeds a critical-volume threshold).

Under the right circumstances, such a relationship can help both sides create value. For example, the supplier might strengthen the distributor’s operations by providing services that require specific expertise such as marketing and after-sales service. Or it may provide infrastructure support—such as sharing a warehouse—in situations where this would lower costs, offering the potential to improve sales volume.

Absent the above conditions, suppliers should opt for a multidealer model, in which they work with several distributors on the same product or products. The principal advantage of this model is that it puts competitive pressure on distributors to earn the supplier’s business.

Professionalizing Distributor Management. Suppliers should professionalize the management of their distributors. This requires setting clear objectives for outsourcing partners and continually reassessing their performance against those objectives. It is critical that the distributor feel the carrot-and-stick effect. In a partnership, the supplier and the distributor should cooperate to develop new business and create value for both entities. By contrast, in a multidealer model, suppliers should manage their distributors through “tough love,” focusing on cost-effectiveness through lean processes.

Key indicators in assessing distributor performance include sales performance against targets (for each product and market segment on a monthly, quarterly, and annual basis), growth of the business through new customers, and specific objectives linked to the supplier’s strategy and tactics.

The Distributors’ Point of View: Market Dynamics and Winning Business Models

Specialty and commodity distribution have different market dynamics. Operating models for distributors range between two extremes: pure specialty versus pure commodity distribution, each of which has different market dynamics and strategic imperatives. Yet in practice, as noted above, there is a sizable gray zone between these two extremes. Most distributors carry products from both segments, while the largest global chemical distributors (such as Brenntag, Univar, and Nexeo Solutions) typically carry a full product line. These companies aim to offer a one-stop value proposition that meets all the chemical needs of their customers, simultaneously achieving critical mass in serving smaller customers and regions.

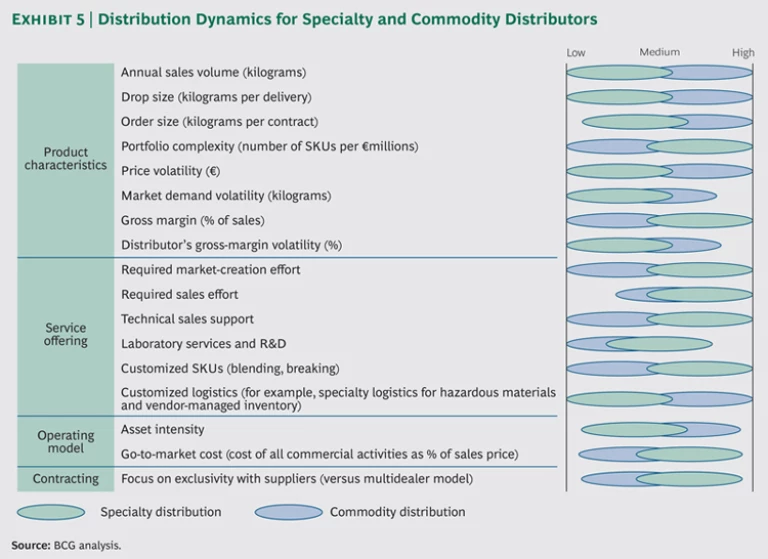

The different market dynamics for commodity and specialty chemicals can be categorized along four dimensions. (See Exhibit 5.)

- Product Characteristics. Specialty chemicals, which are highly functional, are sold in lower volumes, whereas commodity chemicals are, in many cases, sold in bulk. Price and volume volatility tend to be lower for specialty distribution.

- Service Offering. Distribution of specialty chemicals generally requires a higher market-creation effort (contacting potential clients to turn them into interested prospects) and additional services such as technical sales support. Within commodity distribution, the focus is, in many cases, more on logistics excellence. So specialty distribution sales can require greater effort.

- Operating Model. Go-to-market costs are usually higher for specialty distribution owing to a combination of deeper sales relationships, higher knowledge intensity, required technical sales support, and smaller drop and order sizes.

- Contracting. As described in the previous section, mutually exclusive supplier-distributor partnerships are more typical in the specialty segment.

Specialty distribution is a more resilient business than commodity distribution. Compared with suppliers, third-party distributors are, by nature, more sheltered from price fluctuations: the purchase and sales prices of third-party distributors fluctuate in parallel.

Market demand volatility, measured as the uncertainty (that is, the standard deviation) of the year-on-year market growth in the period from 2004 through 2013, is lower in specialty-heavy end markets (4 percent) than in commodity-heavy end markets (8 percent). This is because production in specialty-heavy end markets such as pharmaceuticals, personal care, and food is not so strongly linked to the general economic cycle. By contrast, commodity distribution has a volatile nature: price and volume are more susceptible to macroeconomic swings.

Distributors carrying both segments need a clearly differentiated business model. Suppliers see differentiation as a prerequisite to developing an optimally focused service model in both segments. And distributors indicate that business optimization for both segments requires a different approach.

Winning in specialty distribution requires seven success factors. At a baseline level, all chemical distributors have must-have requirements, such as financial stability; a solid track record in health, quality, security, safety, and environment; a sales force with sufficient local coverage; and efficient logistics and supply-chain activities. However, in the current market, even all that is not enough to win. Given customers’ complex buying criteria and the increasingly sophisticated approach that suppliers now use to select and manage distributors, specialty players will need to differentiate themselves in the market. They should focus on the following success factors.

-

Strong Expertise Regarding Products and Applications to Drive Market Development. In addition to merely fulfilling orders, distributors that truly understand the product—in the context of broader formulations—can provide functions such as technical sales support, cementing a stronger relationship with customers.

-

A Product Portfolio with the Right Chemicals—Anchor Products and Brands—That Reflect Market Demands and Trends. Distributors with deep knowledge of local-market demand and trends can excel at category management. Such knowledge enables them to select the anchor products of leading suppliers in particular applications and to develop a full portfolio of the chemicals needed to dominate related market segments.

-

Strong Access to Local Clients Through High Coverage and Scale Within the Distributor’s Sales Network. For suppliers, the challenge in specialty chemical distribution is reaching customers in target markets while reducing cost and complexity to serve. Accordingly, specialty distributors can differentiate themselves with superlative sales networks that can facilitate the distribution of goods to local customers with a minimal cost to serve.

-

Close Collaboration with Suppliers to Provide Input for Product Offerings and Development. A distributor that has established a strong presence in its individual market—and deep ties to its customers—can provide critical intelligence and insights to suppliers regarding shifts in the marketplace. At a more detailed level, a specialty distributor can serve as a conduit of information on specific products and applications, helping suppliers strengthen their product development and offerings. This requires establishing platforms to provide regular feedback to suppliers.

-

A Homogeneous Approach to Support Panregional Supplier Relationships. As suppliers continue to professionalize their approach to distribution management, they increasingly aim to collaborate with a small group of select distribution counterparts in each region. Each distributor will need to work toward becoming the distributor “of choice” within a target region. For many players that have focused on localized individual markets, this entails an organizational shift to coordinate and manage projects over a larger footprint while providing suppliers with points of contact on the regional level. Distributors must manage the organization on a panregional level while preserving the entrepreneurial and flexible nature of local operations in different subregions. Given the difference in business dynamics, the optimal approach for this differs for commodity and specialty distribution.

-

Process Quality and IT Excellence. As in virtually all other industries, the right technology can streamline logistics and reduce overhead for specialty distributors, allowing them to reduce working capital and costs to create a cost advantage that differentiates them from competitors. In addition, the right processes and IT can enable distributors to share commercial and marketing data with suppliers and can improve suppliers’ ability to track the status of shipments to various customers.

- Winning in the Consolidation Game Through a Combination of Organic and Inorganic Growth. Given current consolidation opportunities, specialty distributors should target both organic and inorganic growth to fill in regional and product gaps in their portfolios. In doing so, they will need to successfully balance the benefits (such as process quality and financial stability) of panregional scale with local-market presence and local entrepreneurship. Successful inorganic growth will require a careful approach in which the risk profiles of M&A targets are diligently assessed.

We are confident that distributors that serve specialty chemical segments and excel in these seven areas will become winners in their markets.

In summary, the chemical distribution market is growing, yet it offers a range of challenges and opportunities.

For suppliers, the priority is to professionalize distribution management through a coherent approach across all direct and indirect channels. This entails developing the distribution channel strategy, selecting the right distributors and the right distributor-interaction model, and doing a better job of managing distributors’ performance.

For distributors of specialty chemicals, the opportunity is to capture sufficient organic and inorganic growth in a fragmented landscape while securing structural relationships with suppliers. As distribution shifts to a regional model, distributors can achieve scale through both organic and inorganic growth while maintaining a strong local-market presence. Most important, they must continue to provide value to suppliers through deep knowledge of products, applications, and local markets.

Acknowledgments

The authors are grateful to all the industry experts involved in this study for their broad participation and their contributions to the research. In particular, they would like to thank their BCG colleagues Stefan Scholz, Maarten Bekking, and Aico Troeman for their contributions to the analysis. In addition, they want to thank Jeff Garigliano for his help in writing this report.