It’s a well-known fact: a significant gulf exists between the need for new or improved infrastructure globally and the projected delivery of that infrastructure. But the critical reasons for the infrastructure gap—and the means of closing it—are less understood.

Although the lack of available capital is often blamed for the problem, the truth is more complex. No doubt, the system for financing infrastructure around the world can be improved. But on the basis of extensive research, The Boston Consulting Group has determined that the key to closing the gap is not simply to improve the flow of capital to projects but also to implement changes in the way projects are developed and executed. Governments that want to generate better returns on their investment in infrastructure must examine how projects are developed from the start and how the public sector and private sector can work together to execute those projects.

Certainly, some countries are doing better than others on these fronts. But our work reveals that no nation has mastered the process completely. In the end, those countries that figure out how to invest in and effectively manage their infrastructure stand to reap significant rewards.

The Infrastructure Challenge

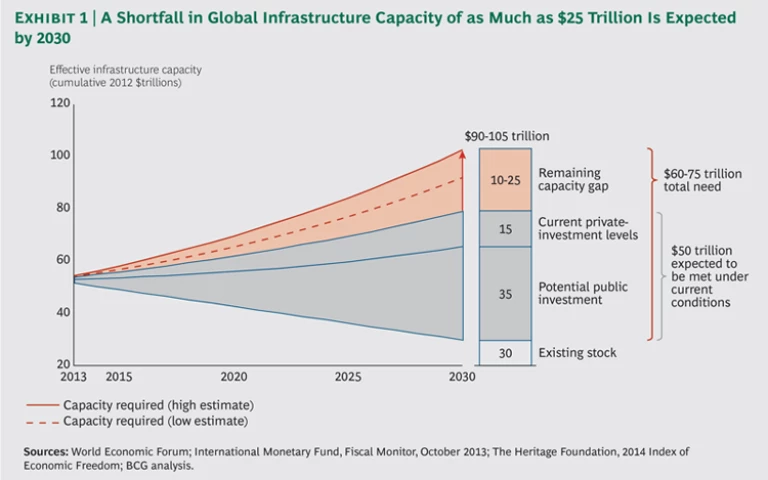

The global infrastructure investment shortfall is staggering. (See Exhibit 1.) By 2030, an estimated $60 trillion to $75 trillion in additional infrastructure capacity will be needed globally. But with the balance sheets of most governments already stretched to the limit, only about $50 trillion in spending is likely to materialize, leaving a gap of up to $25 trillion. And this is not a problem concentrated in a few regions: nearly every country in the world is facing the need to improve its infrastructure.

Of course, private capital could potentially address that shortfall. But institutional investors express widespread frustration at the lack of opportunities to invest in well-designed infrastructure projects that are likely to generate solid returns.

The repercussions are far reaching, with the infrastructure gap threatening to limit gains in living standards and undermine global growth. It is clear that countries that figure out how to drive effective infrastructure improvements in the face of pressured government balance sheets will emerge as winners. According to BCG analysis, every $10 invested in additional infrastructure capacity can produce up to $3 in additional annual economic activity.

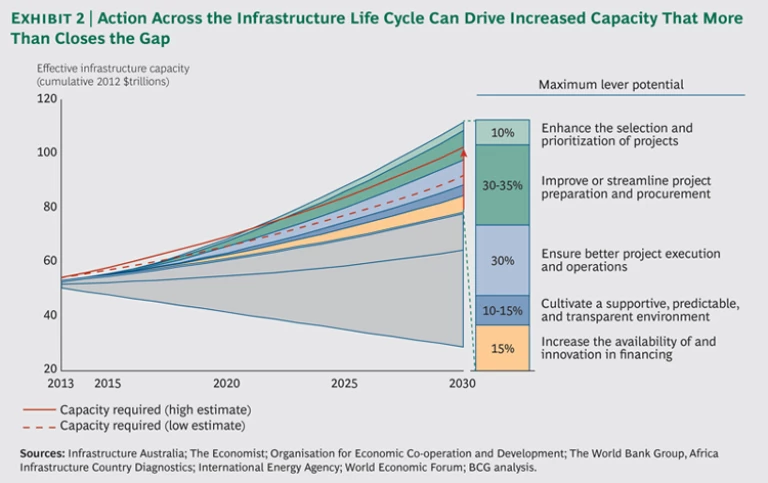

So, what is the answer? Certainly, increasing the availability of either private or public financing will help. (See the sidebar “The Capital Solution.”) But our analysis finds that the greatest impact will come from transforming the efficiency of the entire infrastructure life cycle. (See Exhibit 2.)

THE CAPITAL SOLUTION

When it comes to the financing piece of the equation, the infrastructure gap is less a problem of a capital shortage and more an issue of a lack of solid, bankable projects. While there is no doubt that governments could do more to prioritize long-term investment in areas such as infrastructure over short-term spending, there is also much that can be done to boost the flow of private financing for infrastructure.

First, steps should be taken to reduce unnecessary barriers to the movement of capital, including restrictions on foreign direct investment, which remains well below precrisis levels globally. At the same time, close attention should be paid to the unintended consequences of prudential financial regulation, particularly proposed regulations for institutional investors such as the Solvency II Directive, which sets rules for how much capital European insurance companies must hold. Such rules, if improperly implemented, could unnecessarily restrict the flow of capital to infrastructure projects.

In addition, in countries where capital markets are still evolving, it is crucial to encourage that development. This is particularly important in nations where currency-hedging costs are prohibitively high for foreign investors, because of either underdeveloped markets or heightened exchange-rate volatility. Valuable moves here can include promoting the development of sectors that provide a pool of capital well suited to infrastructure investment such as the private local insurance and pension industries, issuing long-term government bonds that can serve as much-needed benchmarks for an emerging private-sector bond market, and enhancing the credit quality of infrastructure projects through efforts similar to the Europe 2020 Project Bond Initiative.

This involves action in four key areas:

- Enhance the selection and prioritization of projects to focus on the right investments.

- Improve and streamline project preparation and procurement to set up projects for long-term success.

- Ensure better project execution and operations to guarantee efficient construction and to maximize the utilization and value of assets throughout their useful life.

- Cultivate macroeconomic, political, regulatory, and business environments that are supportive, predictable, and transparent when it comes to infrastructure investment.

Addressing these issues requires a coordinated and comprehensive effort involving both the public and private sectors. Such an approach will allow better targeting of investments as well as the harnessing of existing assets to maximum effect.

Enhance the Selection and Prioritization of Projects

Targeting the right investments is the critical first step from which everything else flows. But these initial decisions are often poorly made, a fact that underscores the need for a formal structure designed to drive the rigorous selection and prioritization of projects.

Obstacles to Rational Project Selection. The task of identifying the projects likely to deliver the greatest economic returns is inherently challenging. It requires, among other things, forecasting an uncertain future, assigning monetary value to things such as shortened travel times or reduced vehicle emissions (factors that are difficult to quantify in dollar terms), and establishing a process for evaluating an integrated program of investments rather than just isolated projects.

Certain factors magnify the difficulty. For one thing, forecasting the costs and benefits of infrastructure projects has proven problematic, with benefits typically being overstated and costs being understated. This gives politically motivated project proponents a convenient excuse for disregarding cost-benefit analyses in their investment decisions. A 2010 study of Scandinavian transport projects, for example, found that in 30 percent of projects selected, costs exceeded benefits. In fact, on average, the benefits of the projects selected were only marginally better than would have been achieved by picking projects at random and were only about a third of what might have been achieved with the available budget if the projects selected were those with the greatest long-term benefits.

This reflects a bigger issue: the existing institutional structure frequently does not encourage or incentivize good decisions. That stems from a combination of factors including incentives for project proponents to overstate project benefits, the lack of market repercussions for poor forecasting, the limited transparency of the decision-making process to the public, and the political tendency to favor large, highly visible projects over more-efficient investments including maintenance spending.

A System for Rational Planning. An institutional solution is required to address those challenges. At the heart of this effort is the need for a long-term vision for infrastructure investment, one that is based on solid evidence of costs and benefits and that deploys a consistent decision-making process.

Several components are needed to make this happen. For one thing, governments should undertake a rigorous, transparent, and independent review of all proposed investments. In addition to a cost-benefit analysis that helps identify the projects with the best projected returns overall, this review should include a value-for-money analysis of potential projects. This will determine the best approach for delivering them; that is, whether the project should be a government-run effort, for example, or a public-private partnership. And the performance of all projects should be tracked to measure the true costs and benefits.

Public-sector leaders should also identify any existing assets that would be more efficiently managed under a different ownership structure, whether that is a private enterprise or a state-owned entity. In addition, governments should establish regulatory arrangements to properly oversee those assets under their new structure—with those regulators focused on how the asset in question delivers on its broad objectives. And any decisions on whether and how to privatize government assets must be based on an analysis of the long-term benefit to society of making that shift—not simply short-term considerations such as boosting the government balance sheet.

Improve and Streamline Project Preparation and Procurement

An effective infrastructure strategy often calls for a fundamental shift in governments’ project-preparation and -procurement mind-set. Rather than focus narrowly on delivering a specific asset or financial outcome, they must aim broadly at meeting the needs of the public. It also means embracing new revenue models and better collaborating with the private sector.

Zeroing In on Outcomes. Many governments have grown more sophisticated in their development of infrastructure projects, focusing on the ultimate objective—the ability to transport a certain number of people annually in the most efficient manner, for example—rather than on building a new asset to meet certain specifications. This new approach allows for more creative and cost-effective solutions. Demonstrating clear improvements in outcomes can also help to address a major challenge for governments: public resistance to big infrastructure projects and, in particular, to privatization and public-private partnerships.

Deploying New Revenue Models. The financial payoff from infrastructure projects can be enhanced by the development of sustainable revenue models based on user charges or other new revenue sources. For example, Singapore’s Changi Airport offers a range of free services, such as guided city tours, that are supported by pay-per-use services including showers and rest zones. As a result, the airport not only has developed a valuable ancillary revenue stream but also has emerged as a world leader in customer quality, with a five-star Skytrax rating.

Of course, public buy-in is critical to the success of these new revenue models. In Stockholm, the city government introduced a charge for cars driving during peak traffic hours that led to a 20 percent reduction in rush-hour traffic. However, more than half of the city’s residents were opposed to the fee. To address that opposition, the city temporarily removed the fee—and rush-hour congestion spiked. That triggered a shift in sentiment, with a full 70 percent of the population ultimately supporting the congestion charge.

A New Era of Collaboration. Project preparation can also be improved by encouraging governments and the private sector to work together in more collaborative ways. This includes creating a mechanism for private-sector players to proactively submit infrastructure proposals; currently, governments request proposals for specific predetermined projects. A proactive submission process would require strict controls and checks and balances. But with the appropriate oversight, it would allow governments to tap innovative private-sector approaches that might otherwise go unconsidered. And the public sector should not have Bridging the Gap: Meeting the Infrastructure Challenge with Public-Private Partnerships, BCG report, February 2013.)

Ensure Better Project Execution and Operations

With better project selection and planning as a foundation, major gains can be found in improving the construction of new projects and the operation of existing assets.

A critical step in improving project execution is to embrace the systematic defect-prevention measures and lean processes that are typical of large, efficient manufacturing operations. This includes dividing construction into small subprojects, managing logistics to ensure efficient material and resource flow, and creating a process that detects defects early and allows for quick corrections.

In addition, data and newer technology can help maximize the utilization of assets. Take the case of the smart-parking pilot project in Los Angeles in 2012. With the installation of 6,000 high-tech meters, the system directs drivers to open parking spots through dynamic street signs and mobile-phone apps. And pricing for parking varies with demand, from 50 cents per hour to $6 per hour.

Similarly, technology can be harnessed to deliver integrated traffic management for large transportation assets. A centralized control department manages traffic along Hong Kong’s Route 8, for example, tapping real-time data from tools such as vehicle sensors and closed-circuit television to adjust traffic flow and lane signals in order to minimize congestion.

At the same time, maintenance and selective investments including the addition of capacity can extend the life of infrastructure assets. All too often, however, spending on major new projects takes precedence over such targeted investments.

Cultivate a Supportive, Predictable, and Transparent Environment

It can be challenging to execute the steps outlined here. But it becomes virtually impossible to do so in the absence of a stable macroeconomic, political, regulatory, and business environment. Building the right environment includes establishing strong governance of and coordination among public-sector institutions, facilitating the development of strong private-sector players, and supporting the development of robust capital markets.

In fact, investors frequently cite the stability of the environment as the first issue they consider when screening potential opportunities. After all, infrastructure typically involves heavily regulated industries and requires large fixed assets that cannot be moved in the event of instability. In addition, the revenue generation of infrastructure assets is closely tied to local economic conditions. As a result, these assets are particularly affected by the political and investment environments.

Among the most critical elements is the environmental- and regulatory-approval process for new projects. Certainly, a stringent approval process is required to safeguard public interests and mitigate any potential negative effects on the community from infrastructure projects. But when approval processes become excessively cumbersome and inefficient, valuable projects may stall and the returns on those infrastructure investments that do proceed may be jeopardized.

Approval times vary widely across jurisdictions. Many approvals can be completed relatively quickly, but for some major projects they have taken ten years or longer. Such delays come at a significant cost: a 2009 study found that a one-year delay in the approval for an oil and gas project, for example, can reduce the project’s net present value by up to 20 percent. Even in the UK, where average approval times are short by international standards, businesses have cited delays in planning approvals as the most significant barrier to increased infrastructure investment, according to a 2013 survey.

It is critical to address the risk and uncertainty surrounding approvals. One major difference between those countries that perform well in terms of both the length and the certainty of the approval process and those that perform poorly is that the former typically set specific time limits for major project approvals. Canada has done this and has halved the time taken for major approvals.

Of course, simply setting a time limit won’t solve the problem. An efficient process should also involve a single, properly resourced agency accountable for coordinating the overall approval process, a clear allocation of responsibilities, and the establishment of consistent requirements across the other agencies involved.

The infrastructure gap presents significant challenges to countries worldwide, both developed nations and countries with rapidly growing economies. The solution is not simply to throw money at the problem but to improve the management of infrastructure across the full life cycle, from planning to development to operations. Those countries that understand this and act accordingly stand to reap significant rewards, in terms of both economic gains and the quality of life of their citizens.