In many industries, the changes brought about by digital technology are already evident. Industries as diverse as entertainment, travel, and retail have been disrupted by the emergence of new players using technology to create products and services that offer something new or better. These digital-only players have staked out a valuable position with consumers—and traditional companies are feeling the impact. Just ask the TV companies competing with Netflix, the travel companies competing with Travelocity and Expedia, and the retailers competing with Amazon.

The insurance industry has taken longer to join the rush to a universe of bits. The sales model of agents helping consumers figure out which products to buy has largely remained intact in Western countries, and most insurers haven’t yet felt a big impact from digitization on their revenues.

That is changing as more and more consumers begin to handle their insurance transactions online. A new ecosystem is taking shape, and it will affect every part of the insurance-industry value chain. Companies that don’t adapt will become increasingly vulnerable.

The good news is that digitization doesn’t necessarily mean that traditional insurers will be “Amazoned.” In every area of insurance, all over the world, traditional insurers can use the Internet, mobile technology, and social media—as well as some reworked legacy technologies—to fend off new rivals and get ahead of long-time competitors. The challenge lies in coming up with a roadmap for digitization: where to start, what to change, how much to invest, and how to make it all happen.

Consumer Attitudes

Consumer attitudes toward insurance are changing. In its most recent survey of consumer sentiment, The Boston Consulting Group (BCG) found that approximately 15 percent of consumers in Western nations would, if possible, conduct all of their transactions with insurance providers remotely. That was up from roughly 5 percent two years earlier. Another 50 percent or so would prefer their dealings with insurers to be a hybrid of online transactions and interactions with sales or service people, up from 30 percent two years earlier. In our opinion, the percentage of remote-only users would be higher if the interfaces for common transactions—such as buying a policy, submitting a claim, and modifying an existing policy—were easier to use and more intuitive. But the shift in attitude, which is happening across all socioeconomic groups and applies to every type of insurance, should be enough to get the industry’s attention all by itself.

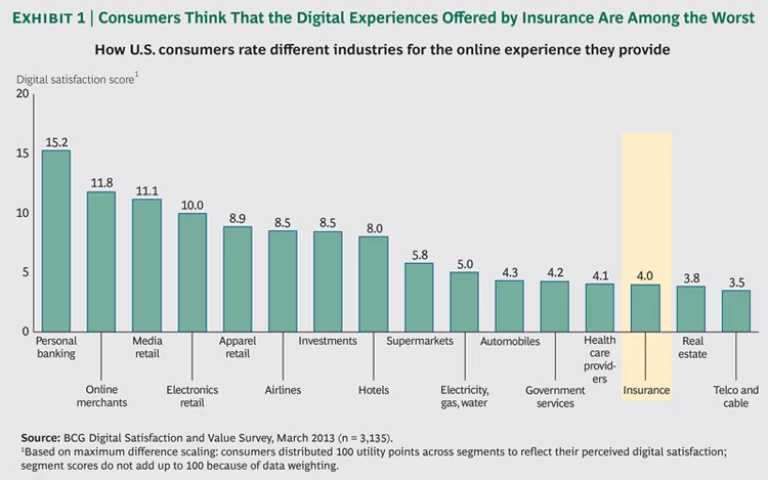

The trend of consumers handling more of their insurance needs on their own is already evident in the early stages of the insurance-buying process. The vast majority of consumers do the bulk of their initial research online, using tools such as search engines and comparison engines, over which insurers have little control. Most of these customers do still turn to agents to finalize their purchases, and that may lead some insurers to think that their traditional networks retain their old relevance. But in many cases, the only real utility provided by insurance agents lies in clarifying and confirming the many policy details that are confusing online. Indeed, in the eyes of consumers, insurers’ websites are among the worst of any major industry. Recent research by BCG in the U.S. highlights the dissatisfaction that consumers feel when they interact digitally with their insurers. (See Exhibit 1.) But this dissatisfaction is not limited to the U.S.; consumers in most other parts of the world feel it, too. (See Evolution and Revolution: How Insurers Stay Relevant in a Digital Future, BCG report, September 2014).

Digitization Is Critical in Three Parts of the Value Chain

Most insurance companies understand that digitization is starting to have an effect on the way they do business. But very few of them have devised a roadmap for how to change. Perhaps the best place to start is with the three parts of the value chain on which digitization is likely to have the biggest impact: internal operations, go-to-market strategies, and risk.

Internal Operations. Insurers have made the most headway here. The benefits stem partly from straight-through processing, which reduces insurers’ use of paper processes and lowers their transaction costs. Digitization of operations also involves developing interfaces for providers such as physicians and hospitals—again, with the goal of streamlining processes and reducing costs.

In many cases, the new guard of digital-only competitors already has paperless processes and highly efficient approaches to handling transactions, which has allowed them to build a significant advantage in terms of variable costs. The per-policy processing costs of one digital-only automobile insurer who shared this information with us, for example, are 30 percent lower than those of traditional insurers, with which the digital-only insurer is starting to compete. If traditional insurers are to remain competitive, they must move faster to make their legacy systems more flexible and better able to operate in real time. This is a significant implementation challenge that will require a lot of planning and investment.

Another way to increase efficiency is by introducing self-service portals. Such portals could allow policyholders to do certain transactions online, without any paperwork or assistance. Insurers face a challenge with the self-service approach, however—which is how to go beyond the mere digitization of existing processes and offer an experience that truly takes advantage of the medium. If insurers believe that providing self-service means simply allowing their customers to access forms online and send those PDFs back via an electronic process, they will be missing both the point and the larger opportunity.

Even insurers that have a clear sense of what they should be offering in the way of self-service need to figure out how to make such investments pay off. In the current structure of the industry, independent agents develop customer relationships and, in many cases, handle customer service as well. More self-service options could reduce the burden on these independent agents without necessarily increasing customers’ loyalty to the insurers themselves. This is an unintended consequence that insurers should take pains to avoid.

Go-to-Market Strategies. By far the biggest go-to-market opportunity for insurers involves the development of direct sales, which usually take place online and are not brokered by an intermediary. These sales have been slow to materialize in the industry because of resistance from traditional sales channels and because of the inherent complexity of insurance products. Perhaps not surprisingly, insurers that have seen early success with direct sales haven’t had any channel conflicts to worry about; they sell insurance online or through telephone fulfillment staffs and don’t rely on agents to generate business. One example is CosmosDirekt, a German insurer that surmounted the complexity issue by putting the application and approval process for term life insurance entirely online. The company has since built on its success in term insurance and is now offering other kinds of insurance.

CosmosDirekt is not alone; other innovative insurers have also gotten over the complexity hurdle and are using a simplified interface to sell directly to consumers. Another good example is Oscar, a start-up health insurer serving residents of New York State in the U.S. With its intuitive graphics and easy-to-use search tools, the company’s online service is bridging the gap that has traditionally separated consumers from insurers.

Direct sales are destined to take significant share from traditional insurance channels, making investments in this area not just an add-on source of revenue but a competitive necessity. However, direct sales are only going to work for insurers that rethink how they build, develop, and market their products. The experience needs to feel new, not like the same old interaction transferred to a new medium.

The second big go-to-market opportunity for insurers lies in giving their full-time salespeople digital-sales tools. Such tools include customer-relationship-management systems that help with some aspects of lead generation and customer service, and that make it easier for sales agents to up-sell and cross-sell. The tools also include portable devices. For instance, the German insurer Allianz started a pilot project in Italy in which agents bring iPads on their visits to clients’ homes and places of work. The agents are able to display benefit information and generate price quotes on the spot, eliminating the inconvenience of follow-up meetings and increasing the likelihood that customers will make impulse buys. When programs involving portable devices are properly implemented, insurers can realize significant productivity gains, with agents managing as much as 25 percent more business than they did previously.

Another very important thing for insurers to learn is how to gain more visibility when consumers are researching which insurance products to buy. Affinity marketing—the tactic of teaming up with a well-known brand in order to bring an offer to a prospect’s attention—can play a big role here. In the U.S., for instance, New York Life Insurance has a deal to sell life insurance and annuities to members of the AARP, an organization with a membership of 37 million retirees. In China, the online insurance company Zhong An has started out with some can’t-miss affinity partners, including the shopping site Alibaba, for which Zhong An will insure property and cargo; the Internet gaming company Tencent; and Ping An Insurance, one of China’s largest insurers. Most of the new digital insurers that have captured significant premiums have done so with the help of an affinity partner. Affinity marketing helps insurers show up on consumers’ radars at an earlier stage of the research process.

Risk. This is the dimension in which digitization has the greatest financial potential, and some insurers have already begun pilots in this area. But the business models involving risk reduction are embryonic, and there is no clear roadmap for moving forward. Very few insurers have had significant success in this area.

Underwriting is one area of risk in which insurers could capitalize on digitization. The science of using actuarial tables and other statistics to create and price insurance products has been around for well over a century and is quite mature. But information from social media, GPS systems, and big data could lead to improvements in insurers’ ability to assess risk.

For instance, auto insurers are starting to use data gathered by telematics devices and mobile-phone applications to determine premiums for new clients—a segment-of-one approach that could make it possible for demonstrably safe drivers to pay lower premiums. That data could also help the auto insurer adjust the prices of policies in subsequent years and more accurately assess the risk of each policyholder. (See “Big Data: The Next Big Thing for Insurers?,” BCG article, March 2013, and “Bringing Big Data to Life: Four Opportunities for Insurers,” BCG article, July 2014.)

Big-data analytics could help insurers more accurately assess other kinds of risk as well. For instance, a mortgage life company might be able to use data from social networks to estimate its loss reserves more accurately by spotting lifestyle changes and recognizing how they might increase an insured person’s risk. And in claims management, companies with more sophisticated approaches to data are already doing a better job of identifying outlier claims, thus reducing their exposure in an area that has historically accounted for a disproportionate percentage of payouts. For example, if an insurer is able to recognize that the injuries suffered by someone in a car accident are atypical, it could arrange for more effective early treatment—thereby lowering the total reimbursements it must make to hospitals and physicians.

The intersection of devices and loss prevention—the vaunted Internet of Things—presents another wide-open area of opportunity. It’s easy to imagine how payouts could be reduced if property and casualty insurers used sensor-driven devices to detect and respond to events such as water leaks, break-ins, and fires, for instance, or if health insurers equipped cardiac patients with heart-monitoring devices that immediately forwarded abnormal readings to the patients’ physicians. What’s harder to imagine is the business model: figuring out who to partner with, how to pay for the devices, and how to set up exclusive deals with device makers.

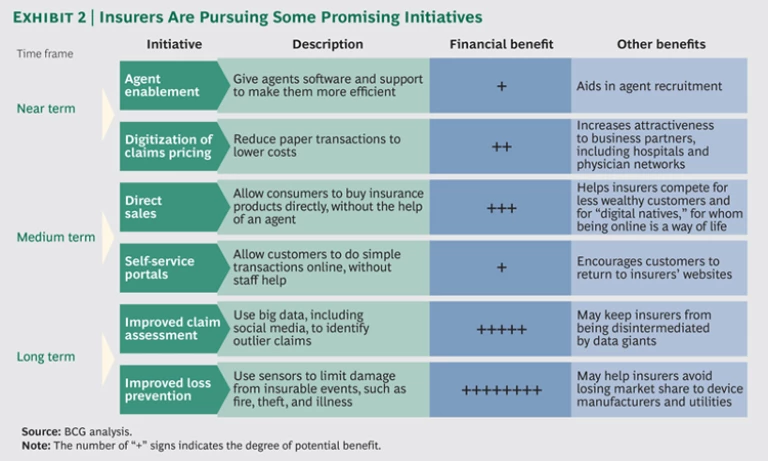

Early pilots are under way in all of these areas. The British insurer Aviva is using unstructured data, including online spending habits and public Facebook postings, to get a sense of its customers’ lifestyles, do predictive modeling, and set premiums for life insurance policies. Some companies—including Aviva and two U.S. insurers, Progressive Casualty Insurance and Allstate Insurance—are also experimenting with using data from mobile apps and in-car telematic devices to price automobile insurance. It’s too early to know how these initiatives will fare, but we think that, in the aggregate, risk initiatives have considerable promise. (See Exhibit 2.)

Unfortunately, risk is also one of the areas in which traditional insurers face the biggest threat of disruption. One need only consider the strategy followed by Rakuten, Japan’s largest online retailer, to understand the frontal assault that Internet companies can make on insurers. A couple of years ago, Rakuten bought AIRIO Life Insurance; Rakuten is now in a position to use the vast amount of data it has on Japanese spending habits—seven out of ten Japanese are repeat Rakuten customers—to price the life insurance policies that it sells to consumers.

Or consider what might happen if Google, whose footprint is considerably larger than Rakuten’s, decided to get into insurance. Given what Google knows about consumers, it’s not hard to imagine the company being able to offer a more innovative approach to risk assessment—and therefore to insurance pricing—than the one offered by traditional insurers. Regardless of how or where the Internet data giants might enter the insurance ecosystem, it is clear that they could alter it profoundly and irrevocably.

There’s also the possibility of competition from companies that haven’t traditionally been direct sellers of insurance, such as automobile original-equipment manufacturers, airlines, and telecommunications companies. In short, the threat to insurers’ business models could come from just about anywhere.

Developing a Roadmap for Digitization

For insurance companies, digitization is a complex equation with three variables: consumers’ evolving preferences, changes in insurers’ internal operations and technology, and emerging ways to assess, analyze, and manage risk. These changes create the possibility of a very different future. Direct players could become business process outsourcers, offering their platforms for others to use as delivery mechanisms for low-cost insurance products. Internet specialists and affinity marketers could alter traditional insurance-distribution channels. Data giants could become the engines behind risk assessment. Equipment makers and utilities could make off with part of the claims business. No part of the value chain is safe.

To best position themselves for success, insurers must develop a roadmap that takes into account four factors:

-

The Altered Ecosystem and New Partnership Possibilities. As new players emerge—in some cases with unique value propositions—traditional insurers will have to decide how to position themselves. This starts with an analysis of how their part of the insurance ecosystem will develop. In some areas, traditional insurers may remain at the center of the ecosystem and have an opportunity to federate within it. But this won’t be a natural role for many insurers. In other areas, traditional insurers won’t be at the ecosystem’s center no matter what they do, and they will have to find other ways of creating value.

Picking the right position in the ecosystem will require scenario analysis, fresh thinking, and the ability to place and manage multiple bets.

- New Innovation Models. Traditional players will need to become more flexible and make learning a priority. They may be able to achieve these goals by doing more of their product-development work outside of their core organizations, perhaps using a corporate venture-capital model. This could allow insurers to surmount some of the challenges inherent in their own organizations. The products developed by these spin-off ventures could be reincorporated into companies’ portfolios, or they could remain external and be marketed by a new entity, depending on which approach makes the most sense.

- Products and Services That Are More Consumer-Centric. While no one yet knows which new products will become popular, the insurance offers that consumers will have access to will clearly be very different from those available today. For insurers, the key is to reimagine the whole consumer experience. Companies that do this well may find that they are able to engage their customers in ways that have previously been impossible. With its Facebook-like features, Oscar’s website has achieved a level of “stickiness” that is rare in the insurance industry. Approximately 5 percent of Oscar’s customers return to the site on a daily basis—quite a feat in an industry where consumer interactions rarely occur more than once a month and sometimes happen as infrequently as once a year.

-

The Need to Modernize IT During a Period of Rapid Change. When it comes to their technology infrastructures, traditional insurers are caught in a difficult spot. On one hand, they need to be able to start delivering some of the benefits of digital technology to their customers quickly. On the other hand, they are sitting on top of legacy systems which, by their nature, can be changed only through a prolonged, multistep process.

The answer is a two-speed IT transformation, which means rolling out some new digital services even as insurers move toward a long-term overhaul of their legacy architectures. This is a difficult balancing act for most IT departments. IT orthodoxy often calls for investing in big-bang projects that can take years to complete. Given the current level of change in the industry, an insurer would be ill advised to pin all its hopes on one big-bang initiative. Instead, the company must have secondary and tertiary initiatives that are already producing returns.

While predicting the exact timing is impossible, we expect that the impact of digitization will hit the insurance industry with full force in the next three to five years. Developing a roadmap now will help insurers preserve flexibility and give them a chance of winning no matter what comes—and when.