For most hedge funds, 2016 was a difficult year. Although the stock market rose to all-time highs, hedge funds returned just 3%. This continued the trend of the previous five years, during which US hedge funds were outperformed by stock and bond markets. Some large clients, pension funds, and insurers started to pull out of hedge funds altogether; others reevaluated their allocations.

The causes of this underperformance are neither clear nor the same for all hedge funds. But market conditions did not help. Volatility was low (prior to the Brexit and US presidential votes), the growth of developing economies had slowed, and commodity prices were depressed.

If market conditions improve in 2017, performance may bounce back and the recent woes of hedge funds may prove to be little more than a blip in the funds’ extraordinary 25-year trajectory—during which their AuM increased 74-fold, from $40 billion in 1990 to $3 trillion in 2016.

But hedge funds are facing more than just subdued performance. The standard hedge fund business model is coming under pressures that will ultimately transform the way hedge funds operate—requiring them to be more integrated with their clients, more agile in adopting technological advances, and more attractive as employers of the new kinds of talent they will need. Whether market conditions improve, stay the same, or worsen, these trends will contribute to increasing industry polarization—and, particularly for hedge funds that are neither large nor niche focused, decreasing viability. Adapting now can help ensure survival.

Six Trends That Will Transform Hedge Funds

Six trends present important opportunities and challenges for hedge funds.

Blurring of the Lines. The lines that have traditionally distinguished hedge funds from their clients and competitors in adjacent spaces are blurring. Hedge funds’ largest clients, such as sovereign wealth funds and pension funds, are becoming more sophisticated, often using the same tools and technologies as hedge funds to execute their own investment strategies. Some clients are partially bypassing hedge funds, and some are seeking different arrangements with them. In a growing market, this trend may have a limited effect on hedge funds, especially the most sophisticated. In a flat or shrinking market, however, the consequences could be profound.

At the same time, competitors from adjacent spaces increasingly compete on hedge fund turf. Fifteen percent of the top four private equity funds’ AuM is now in hedge-fund-type investments. Asset managers are also encroaching, by investing directly in liquid alternatives or by acquiring or partnering with hedge funds.

Of course, the blurring of traditional lines also creates opportunities for hedge funds. Banks and broker-dealers are responding to burdensome new regulations and reduced returns by contracting their capital market offerings. This gives hedge funds the opportunity to enter new lines of business, such as lending, market making, and asset servicing.

Technological Arms Race. AuM in hedge funds reached $3 trillion in 2016, having increased by 150% since 2011. This new scale has made it harder for hedge funds to operate only in investment niches where they can generate alpha and to differentiate themselves from competitors. To stay ahead, leading hedge funds increasingly rely on superior technologies that provide access to new sources of data and the most advanced analytical and decision-enabling techniques.

Gaining access to the best technical expertise, however, is no longer a given for hedge funds. In the post-financial-crisis world, the talent that once went directly to hedge funds is instead going to leading technology companies, fintechs, and other digital startups. The finance industry is suffering from a damaged reputation and the perception that it is no longer “where the action is.” Ambitious and inspired graduates have shifted their gaze from Wall Street to Silicon Valley.

Increasing Complexity. Running a hedge fund is an increasingly complex business. Clients are becoming more sophisticated and demanding. They expect better value: tailored advice that goes beyond investing in the fund, bespoke mandates, more-differentiated investment strategies, and greater transparency. Competition to find new sources of alpha is driving hedge funds toward illiquid and private assets, putting further pressure on already strained technology and operations. And postcrisis regulation continues to grow in both volume and stringency, creating new compliance costs.

Fee Pressure. Hedge funds now face a buyer’s market in which large-asset owners are exercising their bargaining power. Many no longer pay hedge funds the traditional “2 and 20” but instead come to individual arrangements. Indeed, some funds have eliminated management fees altogether, relying entirely on performance fees. At the other end of the spectrum, funds that invest in liquid alternatives—promising returns similar to those yielded by traditional hedge funds (but, arguably, not yet delivering them)—are charging low or even no performance fees and management fees well below 2%.

Continued Low-Yield Environment. With returns from traditional asset classes muted, investors continue to turn to alternative asset classes for the returns, diversification, and levels of risk balancing they require. Because many asset owners must meet a liability target, hedge funds have the opportunity to participate more actively in the growing solution space (outcome-oriented investment, such as target date funds), whose AuM reached $9 trillion in 2015.

Market Concentration. Institutional investors favor “big name” hedge funds, seeking security in their reputations and historical performance. As the hedge fund market matures and more institutional money flows in, the top players are picking up a disproportionate share of the business. At the end of 2008, hedge funds with AuM of more than $5 billion accounted for 56% of all industry assets; by the end of 2015, the figure had risen to 71%.

Three Scenarios: Same, Bad, Worse

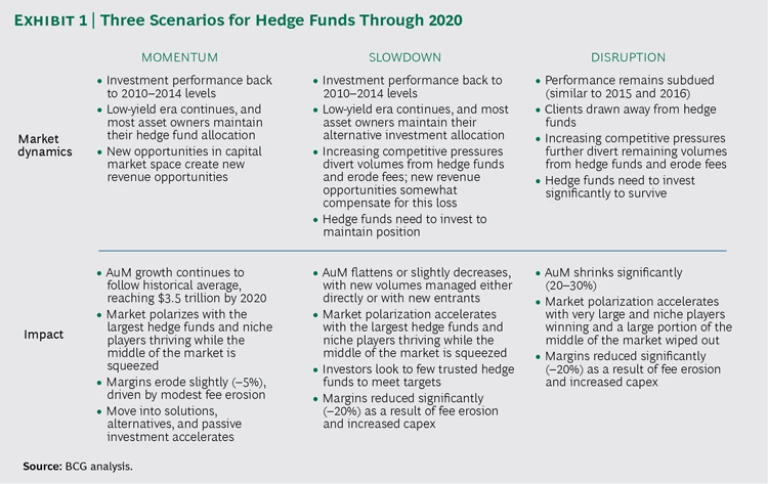

How the trends of recent years will unfold is uncertain, as is their significance for the hedge fund sector. Looking ahead through 2020, we see three possible scenarios for the evolution of the industry: momentum, slowdown, and disruption. (See Exhibit 1.)

None will be easy to navigate.

Even taking the most positive view, in which the industry regains the momentum of prior years, we foresee a transformation. The industry is likely to divide more sharply. Large hedge funds will get yet larger and come to resemble traditional asset managers in performance, pricing, and operational efficiency. Others will keep alive the original hedge fund spirit, with narrow offerings, high performance, and high fees. Hedge funds occupying the undifferentiated middle ground will stagnate, bleed talent, and progressively go out of business.

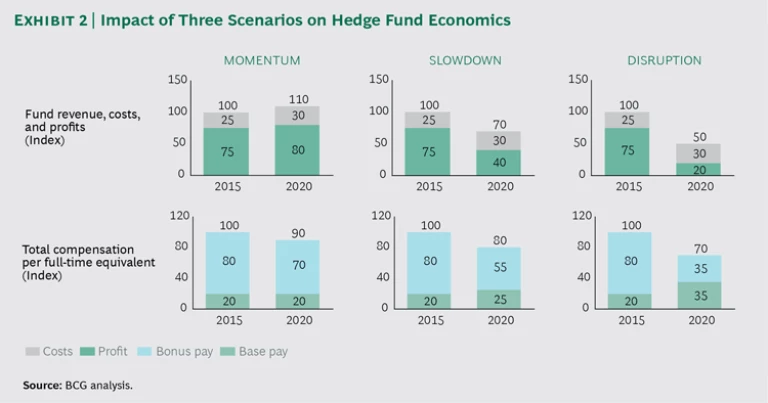

In the most dire scenario, disruption, the structure of the market would be wholly transformed and hedge funds would suffer significant reductions in AuM, margins, and employee compensation. (See Exhibit 2.)

Creating the Hedge Fund of the Future

The momentum scenario, though it is the most benign for hedge funds, is not a given. More profound challenges could be in the cards, and hedge funds must anticipate and prepare to meet them while still in a position of relative strength. The hedge fund of the future will need to do things differently.

Embrace the Technology Revolution. With investment technology advancing rapidly, superior alpha and client service will increasingly come from the skilled use of data mining, analytics, and market- and portfolio-modeling technologies. To gain proficiency in these areas, firms must change the ways in which they source technology, attract talent, and manage their in-house systems:

- Sourcing. Hedge funds will need larger “intelligence teams” to gain access to the best ideas and skills. They should build new partnership models to develop or source technology, often collaborating with tech companies or other investment managers that might otherwise become competitors.

- Talent. The traditional hedge fund talent model is poorly suited to attracting, developing, and retaining technology talent. Hedge funds need a new value proposition for employees, complete with a new breed of manager, a tech-style working environment, and even a tech-heavy location such as the West Coast. Hedge funds must become more team based and less founder driven, with a culture that encourages innovation.

- Operating Model. As technological progress accelerates, hedge funds will need to reorganize in ways that facilitate the adoption of new technology. This requires more flexible and scalable infrastructure and an ever-higher bar for security to protect client data and the hedge fund’s intellectual capital.

- Place an Unprecedented Focus on Clients. In a buyer’s market, clients will demand more from hedge funds: bespoke mandates, value-added advisory services that go beyond particular investments, and deeper integration between hedge funds, their clients, and their clients’ clients. To provide this improved service, hedge funds must change their business models, organizations, and tools:

- Business Model. We expect a proliferation of bespoke mandates. A growing number of large investors will demand co-investment in mandates as a way of lowering fees and acquiring capabilities.

- Organization. Improving advisory services will usually require bigger and more skilled sales and client service teams. Client-facing staff will need strong investment backgrounds so that they can engage with clients to tailor mandates. And they will need large supporting teams that can perform ad hoc analyses for clients and help to train clients’ in-house teams. Portfolio analysts and services staff must be able to act almost as extensions of their clients’ organizations.

- Tools. Hedge funds will need tools that provide clients with near-real-time access to key information, including market data, position analysis, and proprietary insights. These tools will help hedge funds influence a client’s investment processes while making the hedge fund more transparent to the client, creating a unique bond between the parties.

Build an Agile and Scalable Operating Model. Hedge fund operations must become flexible, or “agile,” so that the interface with new customers can be quickly established, mandates can be easily customized, and new technology can be installed in a matter of days rather than months. Yet efficiency also requires operations to be scalable, meaning that volumes can be increased or decreased at a minimal additional cost. Although scalability benefits from a simple offering, providing clients with a flexible and customized service inevitably introduces complexity. A tradeoff between flexibility and cost efficiency is inevitable. The better the hedge fund’s technology, the better the tradeoff that can be found.

The operations and technology of most hedge funds are now far from ideal. Most rely on systems that are developed and maintained in-house and that achieve only moderate agility at the high cost of throwing people at the problem. Overhauling the standard operating model will require radical choices and large investments:

- Choices. A large portion of many hedge funds’ support functions could be better built and operated by third-party suppliers, such as technology vendors. Only core activities—those required to truly differentiate the hedge fund’s core investment, client management, and risk management capabilities—should be built and maintained in-house.

- Investments. Transforming the operating model will usually require that the old technology and processes be ripped out and replaced. This is a massive, multiyear effort during which the new operations must be defined, built, tested, and rolled out even as day-to-day business continues. Though conceptually uncomplicated, the transformation involves considerable capital expenditure and execution risks.

Hedge funds that can make these changes and achieve the required scale or specialization will be positioned to meet the coming challenges. They will be able to retain their clients, and their improved operating efficiency will allow them to sustain margins despite likely reductions in fee income. Hedge funds that fail to reform their business models will be lucky to survive, unable to attract talent or investors.

Natural market momentum and low interest rates will continue to sustain the industry for a few years yet. But hedge fund managers cannot afford to be timid. The challenges they face should stir them into bold action, before it is too late.