Consolidation has driven M&A in the chemical industry for decades. Now, though, the pace is accelerating, transforming many chemical segments as companies look to focus their portfolios and further optimize their business models. To survive in this environment, companies need more than functional M&A capabilities—to identify specific opportunities, they need to understand the consolidation dynamics within the different specialty-chemical segments.

Adding to the M&A environment’s complexity: stepped-up competition from ever-more-sophisticated private equity buyers (which benefit from fewer regulatory or antitrust concerns than strategic buyers), newly assertive competitors from Asia pursuing outbound deals across the globe, and the tricky balancing act many companies must manage as they diversify their offerings while consolidating their focus.

With these dynamics in mind, we have assessed the progress of consolidation in key chemical segments, examined several secondary drivers of M&A in the industry and the impact of private equity in chemicals, and identified a number of concrete steps that executives can take to establish and maintain a competitive edge in the pursuit of M&A deals going forward.

Consolidation on the March

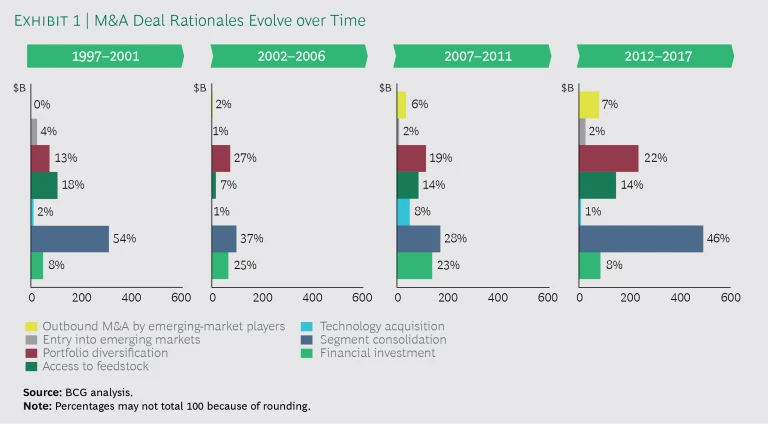

There have always been multiple deal rationales in the chemical industry, but consolidation has consistently been the number-one reason. (See Exhibit 1.) We don’t expect that to change; in fact, the pace of consolidation is likely to pick up. Our analysis of all deals announced in chemicals from 2012 through 2017 indicates that segment consolidation is the most popular deal rationale, accounting for almost 46% of all deal value. Portfolio diversification is the second most popular rationale at approximately 22%. M&A for geographic expansion contributes about 9%; technology acquisition accounts for just 1%.

The reasons for consolidation vary. Some companies, such as those in the agrochemical segment, are motivated to consolidate to gain scale and lower costs, which they can accomplish by acquiring related businesses and combining R&D, production, sales, and logistics activities. Others seek to strengthen a specialty, snapping up divisions or assets rather than entire companies. This rationale is particularly dominant among base-chemical players that want to go downstream into high-value and niche businesses such as compounding.

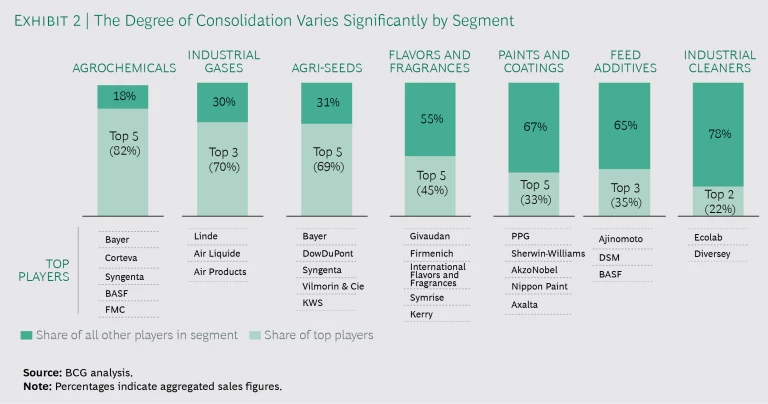

But the degree of consolidation in the different specialty segments varies greatly, and that creates some interesting dynamics and opportunities. In specialty segments where there are still many players—such as industrial cleaners and feed and food additives—we expect the volume of deals to remain strong. In segments that have already undergone significant consolidation—such as industrial gases, paints and coatings, agrochemicals, and flavors and fragrances—we expect fewer but higher-value deals for the simple reason that there are fewer but larger targets. (See Exhibit 2.)

However, to truly understand the opportunities you need to dig a bit deeper into each specific segment.

- Industrial Gases. Consolidation is not new within industrial gases. But the latest deal in this area, the $82 billion merger between the Linde Group and Praxair Technology, is truly transformative—because it will leave only three other sizable global players in the industry. We expect that regulators will demand more divestures out of the Linde/Praxair deal, creating opportunities for smaller industrial gas players and PE firms. Already, Taiyo has agreed to buy $6 billion of Praxair assets in Europe that will help it compete head-on with industry leaders such as Linde and Air Liquide.

- Agrochemicals and Crop Protection. Years of strong competition and dynamic M&A activity have left just five key players in the industry. The battle among industry giants such as Bayer, ChemChina, and BASF has been fierce, and given the already consolidated state of the industry, any further M&A activity involving the top five companies is likely to face significant regulatory hurdles.

- Paints and Coatings. This industry is dominated by several large players including PPG Industries and The Sherwin-Williams Company, yet there are still several regional paint players such as Kansai Paint and Asian Paints. So, although the level of consolidation is already high, we believe there will be plenty of midsize M&A deals in the years to come.

- Flavors and Fragrances. Although the top five players control almost 45% of the market, this space is quite fragmented, leaving room for consolidation. In particular, we believe that leading players in mature markets will look for targets among the many small regional players in emerging markets. This has already started to happen: International Flavors & Fragrances acquired Frutarom, and Givaudan scooped up Naturex (specifically targeting its natural-ingredient business).

Other M&A Drivers

Motivations apart from consolidation contribute to M&A activity and have a significant influence on market dynamics.

Diversification. This is the second most powerful M&A motivator, which makes sense given the importance of opening up new revenue streams and diluting concentration risk. Diversification is particularly attractive for multispecialty players that aim to gain by adding customers and end industries.

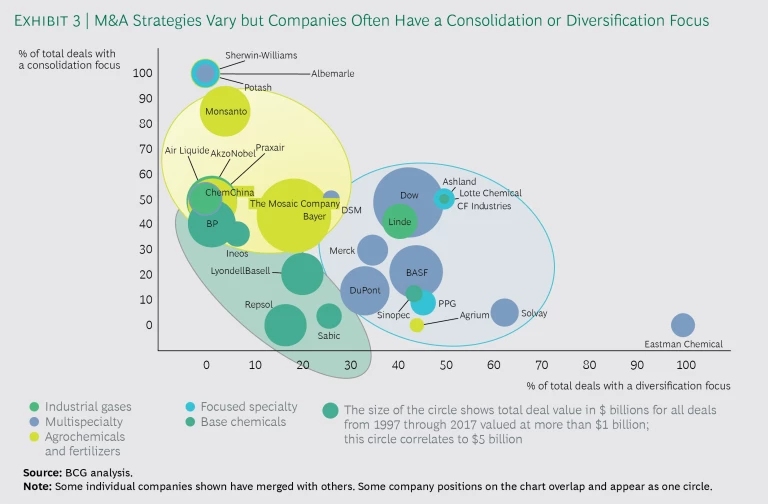

Over the years, players such as Dow Chemical, DuPont, BASF, DSM, and Solvay have pursued M&A deals to diversify their end industry exposure. But companies must carefully balance their diversification and consolidation goals. (See Exhibit 3.) However, by no means do portfolio diversification and market consolidation contradict each other. Portfolio diversification is intended to expand a company’s exposure to new end industries or new customers whereas segment consolidation is deployed to increase market share within the select few segments in which the player sees the highest value.

Access to Feedstock. Another popular and sensible reason for M&A, gaining access to feedstock allows a company to protect a competitive position and prepare for possible shortages of critical raw materials. This rationale is prevalent in the base-chemical segment. A prime example is Ineos, which acquired multiple upstream oil and gas assets in the North Sea in order to integrate them into its downstream businesses.

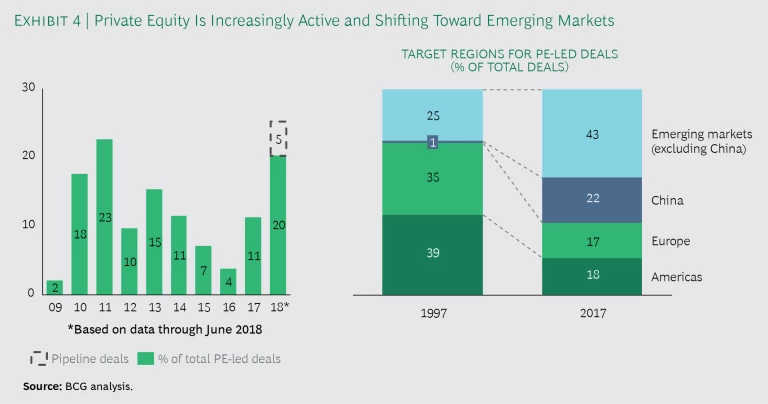

PE Investment. Over the past 20 years, some PE players have developed a deep understanding of chemical assets. That insight, along with their appetite for deals, makes them a force to be reckoned with. Amid the financial crisis in 2009, only 2% of chemical M&A deals were led by PE firms. But much has changed since then. In 2017, 11% of all M&A deal volume in chemicals was led by PE firms, and we expect that momentum to carry forward with another strong year in 2018. By mid-2018, PE players accounted for about 20% of deals including the biggest of the year, Carlyle Group’s $12.6 billion acquisition of AkzoNobel’s specialty-chemical business. Some global PE players in chemicals (such as Carlyle, Arsenal Capital Partners, and Apollo Global Management) focus on the Americas, while others (such as Advent) focus on mainland Europe.

Historically, PE players have tended to shy away from emerging markets, preferring targets in mature markets.

However, strong growth in emerging markets, an improved regulatory environment, and a stable growth outlook are turning the tide. (See Exhibit 4.) PE players usually hunt for independent assets that are easier to value, manage, and, ultimately, sell. And because PE firms’ participation generally raises few if any regulatory or antitrust concerns, they often enjoy a built-in advantage over strategic buyers.

Asian Competitors. These newly assertive firms are pursuing outbound deals to globalize their footprint and broaden their portfolios. From 2002 through 2006, outbound deals made up just 2% of total global activity; in the period from 2012 through 2017, that share jumped to nearly 7%.

Historically, Chinese firms have looked at players in China or Southeast Asia as acquisition targets. But this changed in the last ten years: Chinese chemical companies, including state-owned enterprises, are now approaching targets in Europe and the Americas to access key technologies and IP and to establish themselves as global players. ChemChina’s emergence on a global scale with its acquisition of Syngenta and Sabic’s investment in Clariant point to a trend that will heat up in the years ahead.

Roadblocks to M&A

The environment for chemical industry M&A activity is quite favorable. The global economy is chugging along, interest rates are still low, and many companies have cash on hand. Moreover, pursuing focus through acquisitions is a well-grounded strategy with a track record of positive returns for shareholders; in other words, it is a strategy that executives can explain clearly to stakeholders and pursue with confidence.

But companies must navigate some formidable roadblocks as they pursue the M&A strategy. Low interest rates are contributing to high valuations, making acquisitions quite expensive. Political tensions, most notably the trade situations involving the US, Europe, and China, must be considered. To varying degrees, import tariffs affect the ways in which chemical companies conduct business and thus their attractiveness as M&A targets.

Another challenge comes from the increased regulatory scrutiny of deals. The uptick in consolidation within certain chemical segments has made antitrust regulators cautious about approving large M&A deals for fear of monopolies that could hurt customers and consumers. As a result, several megadeals have been pending for almost two years. Indeed, almost all the most historically active acquirers—Bayer, Dow, Monsanto, Praxair, ChemChina, DuPont, Linde, and more—are bogged down in regulatory discussions.

This delay in approvals is getting more acute. In 2015, at the recent peak in M&A activity, 17% of deal volume announced during the year was left pending at year end. Pending volume jumped to 45% in 2016 and then 50% in 2017. With companies struggling to finalize deals, new activity has been subdued, especially the most ambitious megadeals (which are predominantly consolidation deals). No deal greater than $10 billion was announced in 2017 and just one appeared by midyear in 2018 (the Carlyle Group/AkzoNobel deal).

Be an Active Player

As consolidation continues to remake the chemical industry, companies need to hone their M&A capabilities, sharpen their outlook, and work through roadblocks to make certain they can be proactive and remain competitive in a very dynamic environment. To this end, we have defined six recommendations for active M&A players:

- Set reasonable downstream goals. Executives need to realistically assess how many end industries their company should play in. Companies that get too broad run the risk of losing focus and not getting deep enough in terms of customer centricity in all the industries.

- Continually pursue business “fit.” Maintain a fresh, unsentimental perspective on the business. Regularly analyze business units and assets. Identify those areas of the business that are no longer a good fit (and perhaps never were) and that other players, including private equity, might like to acquire. It is also important for players to connect and follow competitor moves and assess their own business performance on a continual basis.

- Scan for threats and opportunities. Proactively monitor trends and the competitive landscape to understand what is happening not only in adjacent markets but also in downstream markets to spot threats and opportunities from competitors. Be open to acquisitions to specialize operations and deepen capabilities. This will require institutionalizing processes to screen targets regularly.

- Be opportunistic. Sometimes the best opportunities are the ones you aren’t expecting, but if you can pivot quickly to consider them, especially at a time when regulators are likely to force a sale, you could score a good deal. For example, in April, BASF agreed to acquire seed and crop protection assets from Bayer valued at €1.7 billion as Bayer sought antitrust approval for its acquisition of Monsanto (which it finally won in May). BASF’s purchase came after it had already agreed to purchase €5.9 billion in Bayer assets in October 2017. Similar opportunities are expected to arise from the Linde/Praxair deal.

- Be flexible with M&A structures. The regulatory dynamic is likely to yield more complex agreements between regulators and acquirers—with carve-outs, asset sharing, asset swaps, and joint ventures—creating more M&A opportunities, albeit perhaps less conventional opportunities. Remain open to these deal structures to make full use of available opportunities. For example, both BASF (in 2017) and Clariant (in 2014) divested their leather chemical businesses to Stahl Holdings in exchange for cash plus a minority stake in the company—making Stahl the global market leader in leather chemicals. Meanwhile, the merger of Dow and DuPont required the divestment of crop protection businesses that resulted in an asset swap with FMC’s health and nutrition business in 2017.

- Don’t break what you buy. Institutionalize your integration processes so that each acquisition is fairly assessed and integrated correctly. That doesn’t mean each acquisition is integrated in an identical way. Sometimes it’s best to keep the target’s business model operating in parallel with the incumbent’s business model. This is especially likely in downstream businesses where models are tailored to meet the demands of an end industry or segment. Trying to completely integrate a downstream business model could easily destroy value.

Put the Future in Focus

Chemical companies need an active M&A strategy that is tuned to sense new business opportunities around the globe. This has never been more important, as the trend toward consolidation and deeper specialization to serve fewer end industries and chemical segments gathers strength and as companies involved in megadeals will increasingly spin off assets to gain regulatory approval.

Companies that want to leverage these trends for their own advantage will need to compete not only with other industry players but with a very active and expert PE community. Though the competition will be intense—and regulatory and political issues will invariably make structuring deals complex—companies can position themselves for long-term success by institutionalizing an M&A strategy and honing their expertise.