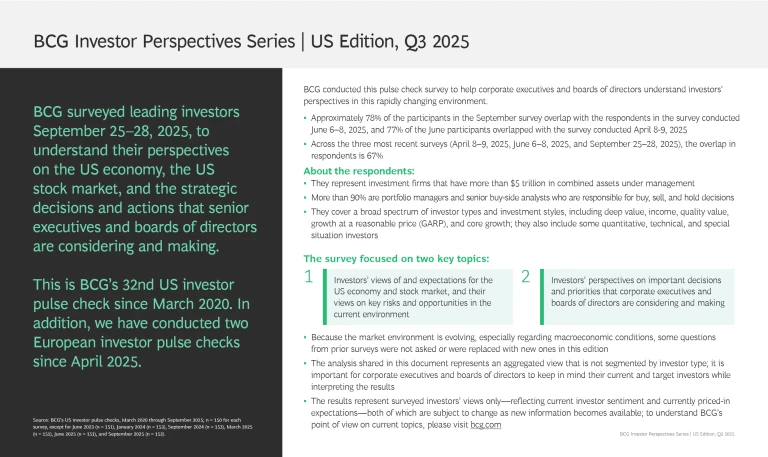

October 23, 2025

As we navigate a rapidly changing and uncertain world, how do US and European investors view the economies and stock markets? And what do they expect from the companies they invest in?

The BCG Investor Perspectives Series brings the voice of the investor to business leaders and board members. We gather the perspectives of US and European investors and present our findings in two editions, drawing comparisons among investors’ views and highlighting the insights and implications for companies.

BCG Investor Perspectives Series, US Edition

BCG Investor Perspectives Series, European Edition

BCG Investor Perspectives Series | Past US Editions

BCG Investor Perspectives Series: Q1 and Q2 2025 | March 24–25, 2025 and April 8–9, 2025

After the new US tariffs were announced and markets took a sharp downturn, only 20% of US investors described themselves as bullish for 2025. However, 66% are bullish for the next three years.

BCG Investor Perspectives Series: Q4 2024 | November 8–10, 2024

In the wake of the US elections and the S&P 500 setting several all-time highs, investors are optimistic despite slowly receding inflation and other risks.

BCG Investor Perspectives Series: Q3 2024 | September 20–23, 2024

Investors’ 2024 outlook remains muted, reflecting concerns about persistent inflation, the US elections, and geopolitical risks. Still, investors continue to expect companies to invest in long-term growth and value creation while protecting short-term performance.

BCG Investor Perspectives Series: Q2 2024 | June 14–16, 2024

Despite all-time-high S&P levels, only 41% are bullish for the remainder of 2024. More investors—73%—emphasized balance sheet health in this survey, reflecting a relatively risk-averse mindset.

BCG Investor Perspectives Series: Q1 2024 | January 16–18, 2024

A smaller share of investors—52%, down from 72% in October 2023—expect a recession by year-end, but they are still bearish. Investors’ priorities for companies include delivering on near-term EPS guidance, investing for long-term growth, and maintaining a healthy balance sheet.

BCG Investor Perspectives Series: Q4 2023 | October 10–13, 2023

Few investors—38%—are bullish for 2024, while 65% are bullish for the next three years. However, investors expect the S&P 500 to return only 6% over that time frame. Interest rates remain investors’ top concern, and 73% have reduced their exposure to companies with higher leverage.

BCG Investor Perspectives Series: Q2 2023 | June 5–8, 2023

Investors remain bearish, with 78% expecting inflation to remain elevated through the end of 2023. Investors are also increasingly conservative about capital allocation, especially for M&A and share buybacks.

BCG Investor Perspectives Series: Q1 2023 | February 13-22, 2023

Investors are less bearish than they were in Q4 2022, but they remain concerned about elevated inflation and a potential recession in 2023. At the same time, optimism for the next three years is at a series high—73% of investors are bullish, compared with the series average of 61%.

BCG Investor Perspectives Series: Pulse Check #21 | October 7-11, 2022

Only 5% of investors are bullish for 2022, and many think a US recession is around the corner. The number one macro concern for 87% of investors is inflation and the Federal Reserve’s policy.

BCG Investor Perspectives Series: Pulse Check #20 | June 17-21, 2022

Investors are the most pessimistic they have been since the Global Financial Crisis. However, the majority of investors are bullish for the next three years, which is reflected in an average annual TSR of 8.5%.

BCG Investor Perspectives Series: Pulse Check #19 | March 18-22, 2022

Investors are more bearish on the economy, with 65% expecting a recession in 2022 or 2023. The importance of geopolitical risks has grown, and many—71%—want companies to disclose their exposure to Russia.

COVID-19 Investor Pulse Check #18 | January 28-31, 2022

Investors are more bearish on the economy and the stock market—especially for 2022. And while they see a company’s long-term growth outlook as the primary investment criterion, a series high of 86% expect companies to deliver on guidance.

COVID-19 Investor Pulse Check #17 | October 29-31, 2021

Investor concern about the business impact of the pandemic is waning—with 55%, down from 63% in June, seeing it as an important investment consideration. But investor concerns over inflation, interest rates, and macroeconomic growth are on the rise—and investors increasingly expect management to deliver on forecasts.

COVID-19 Investor Pulse Check #16 | June 19-20, 2021

While investors are more bullish on the US economy, they are less optimistic on the stock market, with 39%—down from 50% in April—bullish for the rest of 2021. And 63% continue to view COVID-19 as an important consideration in their investment decisions.

COVID-19 Investor Pulse Check #15 | April 29-30, 2021

Investor expectations may be starting to return to prepandemic norms. While 88% of investors (down from a series high of 95% in February) want management to invest in building advantage even at the expense of EPS, a series high of 79% expect management to deliver EPS that at least meets guidance or consensus.

COVID-19 Investor Pulse Check #14 | February 6-7, 2021

A majority of investors expect the pandemic’s economic impact will extend through Q4 2021. And 95% of investors believe companies should build capabilities now, even at the expense of short-term results.

COVID-19 Investor Pulse Check #13 | December 12-13, 2020

Most investors still offer management unprecedented flexibility to invest for long-term advantage. But they also expect management to deliver EPS that at least matches revised guidance.

COVID-19 Investor Pulse Check #12 | November 13-14, 2020

Investors are more bullish on the US economy and stock market than they were just one month ago. And while investors continue to offer management exceptional latitude, more expect companies to maintain their dividend.

COVID-19 Investor Pulse Check #11 | October 16-17, 2020

Investors are more bearish on the duration of the pandemic and the outlook for 2021. In addition, 74% think management teams should move quickly to revise plans after the US election.

COVID-19 Investor Pulse Check #10 | September 18-19, 2020

A majority of investors expect the S&P 500 to return to earnings growth by the end of Q2 2021. And 70% support reinstating dividends at some level for COVID-resilient companies by the end of Q1 2021.

COVID-19 Investor Pulse Check #9 | August 7-9, 2020

A majority of investors expect either a W-shaped or U-shaped recovery. And 71% believe management should actively pursue acquisitions to strengthen the business, preferably using tuck-in deals.

COVID-19 Investor Pulse Check #8 | July 17-19, 2020

Investors expect the pandemic’s impact on the US economy to last longer—through Q2 2021. In addition, only 11% of investors think management is seizing the moment to build advantage.

COVID-19 Investor Pulse Check #7 | June 26-28, 2020

Investors are more pessimistic on the timing and shape of the recovery. This edition also includes investor perspectives on management incentives in the current environment.

COVID-19 Investor Pulse Check #6 | June 5-7, 2020

Investors are more bullish than they were in April—and still willing to offer management significant flexibility to invest for the long term. They also want discretionary investment focused on financial health and future growth.

COVID-19 Investor Pulse Check #5 | May 15-17, 2020

Investors are less bullish on the market than they were one month ago, and they want honest and transparent communications from management.

COVID-19 Investor Pulse Check #4 | May 1-3, 2020

Investors expect the pandemic’s impact on the US economy to continue through the end of 2020, and less than half of them are bullish for the market in 2021.

COVID-19 Investor Pulse Check #3 | April 17-19, 2020

Investors are increasingly negative on the economy in 2020 and on the stock market in 2021. See the results from the investor survey conducted April 17–19.

COVID-19 Investor Pulse Check #2 | April 3-5, 2020

Investors are bearish now, but they are increasingly bullish for 2021 and 2022—and willing to offer executives unexpected flexibility to navigate the crisis.

COVID-19 Investor Pulse Check #1 | March 20-22, 2020

BCG’s ongoing survey provides insights on the US market and economy direct from the portfolio managers and senior analysts making buy, sell, and hold decisions right now.

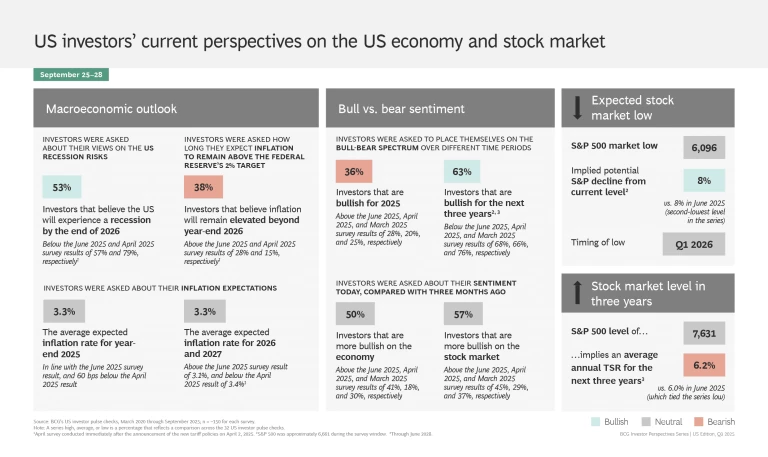

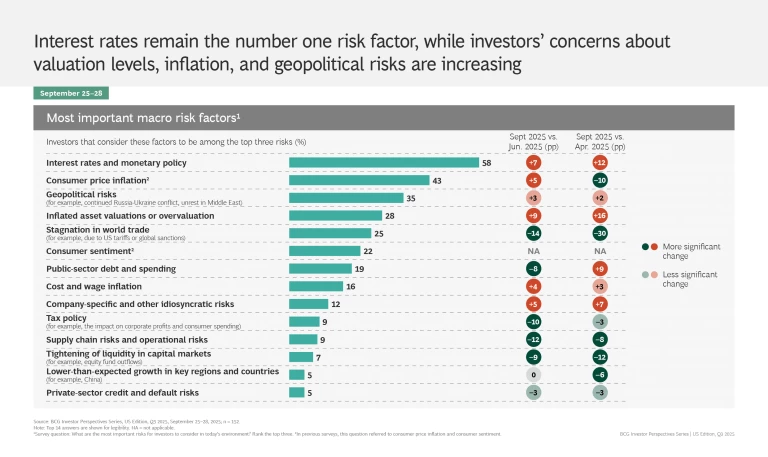

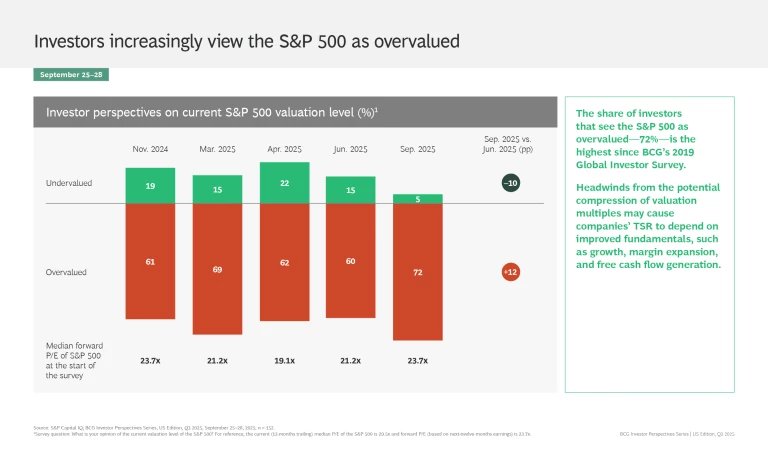

After the new US tariffs were announced and markets took a sharp downturn, only 20% of US investors described themselves as bullish for 2025. However, 66% are bullish for the next three years.

BCG Investor Perspectives Series: Q4 2024 | November 8–10, 2024

In the wake of the US elections and the S&P 500 setting several all-time highs, investors are optimistic despite slowly receding inflation and other risks.

BCG Investor Perspectives Series: Q3 2024 | September 20–23, 2024

Investors’ 2024 outlook remains muted, reflecting concerns about persistent inflation, the US elections, and geopolitical risks. Still, investors continue to expect companies to invest in long-term growth and value creation while protecting short-term performance.

BCG Investor Perspectives Series: Q2 2024 | June 14–16, 2024

Despite all-time-high S&P levels, only 41% are bullish for the remainder of 2024. More investors—73%—emphasized balance sheet health in this survey, reflecting a relatively risk-averse mindset.

BCG Investor Perspectives Series: Q1 2024 | January 16–18, 2024

A smaller share of investors—52%, down from 72% in October 2023—expect a recession by year-end, but they are still bearish. Investors’ priorities for companies include delivering on near-term EPS guidance, investing for long-term growth, and maintaining a healthy balance sheet.

BCG Investor Perspectives Series: Q4 2023 | October 10–13, 2023

Few investors—38%—are bullish for 2024, while 65% are bullish for the next three years. However, investors expect the S&P 500 to return only 6% over that time frame. Interest rates remain investors’ top concern, and 73% have reduced their exposure to companies with higher leverage.

BCG Investor Perspectives Series: Q2 2023 | June 5–8, 2023

Investors remain bearish, with 78% expecting inflation to remain elevated through the end of 2023. Investors are also increasingly conservative about capital allocation, especially for M&A and share buybacks.

BCG Investor Perspectives Series: Q1 2023 | February 13-22, 2023

Investors are less bearish than they were in Q4 2022, but they remain concerned about elevated inflation and a potential recession in 2023. At the same time, optimism for the next three years is at a series high—73% of investors are bullish, compared with the series average of 61%.

BCG Investor Perspectives Series: Pulse Check #21 | October 7-11, 2022

Only 5% of investors are bullish for 2022, and many think a US recession is around the corner. The number one macro concern for 87% of investors is inflation and the Federal Reserve’s policy.

BCG Investor Perspectives Series: Pulse Check #20 | June 17-21, 2022

Investors are the most pessimistic they have been since the Global Financial Crisis. However, the majority of investors are bullish for the next three years, which is reflected in an average annual TSR of 8.5%.

BCG Investor Perspectives Series: Pulse Check #19 | March 18-22, 2022

Investors are more bearish on the economy, with 65% expecting a recession in 2022 or 2023. The importance of geopolitical risks has grown, and many—71%—want companies to disclose their exposure to Russia.

COVID-19 Investor Pulse Check #18 | January 28-31, 2022

Investors are more bearish on the economy and the stock market—especially for 2022. And while they see a company’s long-term growth outlook as the primary investment criterion, a series high of 86% expect companies to deliver on guidance.

COVID-19 Investor Pulse Check #17 | October 29-31, 2021

Investor concern about the business impact of the pandemic is waning—with 55%, down from 63% in June, seeing it as an important investment consideration. But investor concerns over inflation, interest rates, and macroeconomic growth are on the rise—and investors increasingly expect management to deliver on forecasts.

COVID-19 Investor Pulse Check #16 | June 19-20, 2021

While investors are more bullish on the US economy, they are less optimistic on the stock market, with 39%—down from 50% in April—bullish for the rest of 2021. And 63% continue to view COVID-19 as an important consideration in their investment decisions.

COVID-19 Investor Pulse Check #15 | April 29-30, 2021

Investor expectations may be starting to return to prepandemic norms. While 88% of investors (down from a series high of 95% in February) want management to invest in building advantage even at the expense of EPS, a series high of 79% expect management to deliver EPS that at least meets guidance or consensus.

COVID-19 Investor Pulse Check #14 | February 6-7, 2021

A majority of investors expect the pandemic’s economic impact will extend through Q4 2021. And 95% of investors believe companies should build capabilities now, even at the expense of short-term results.

COVID-19 Investor Pulse Check #13 | December 12-13, 2020

Most investors still offer management unprecedented flexibility to invest for long-term advantage. But they also expect management to deliver EPS that at least matches revised guidance.

COVID-19 Investor Pulse Check #12 | November 13-14, 2020

Investors are more bullish on the US economy and stock market than they were just one month ago. And while investors continue to offer management exceptional latitude, more expect companies to maintain their dividend.

COVID-19 Investor Pulse Check #11 | October 16-17, 2020

Investors are more bearish on the duration of the pandemic and the outlook for 2021. In addition, 74% think management teams should move quickly to revise plans after the US election.

COVID-19 Investor Pulse Check #10 | September 18-19, 2020

A majority of investors expect the S&P 500 to return to earnings growth by the end of Q2 2021. And 70% support reinstating dividends at some level for COVID-resilient companies by the end of Q1 2021.

COVID-19 Investor Pulse Check #9 | August 7-9, 2020

A majority of investors expect either a W-shaped or U-shaped recovery. And 71% believe management should actively pursue acquisitions to strengthen the business, preferably using tuck-in deals.

COVID-19 Investor Pulse Check #8 | July 17-19, 2020

Investors expect the pandemic’s impact on the US economy to last longer—through Q2 2021. In addition, only 11% of investors think management is seizing the moment to build advantage.

COVID-19 Investor Pulse Check #7 | June 26-28, 2020

Investors are more pessimistic on the timing and shape of the recovery. This edition also includes investor perspectives on management incentives in the current environment.

COVID-19 Investor Pulse Check #6 | June 5-7, 2020

Investors are more bullish than they were in April—and still willing to offer management significant flexibility to invest for the long term. They also want discretionary investment focused on financial health and future growth.

COVID-19 Investor Pulse Check #5 | May 15-17, 2020

Investors are less bullish on the market than they were one month ago, and they want honest and transparent communications from management.

COVID-19 Investor Pulse Check #4 | May 1-3, 2020

Investors expect the pandemic’s impact on the US economy to continue through the end of 2020, and less than half of them are bullish for the market in 2021.

COVID-19 Investor Pulse Check #3 | April 17-19, 2020

Investors are increasingly negative on the economy in 2020 and on the stock market in 2021. See the results from the investor survey conducted April 17–19.

COVID-19 Investor Pulse Check #2 | April 3-5, 2020

Investors are bearish now, but they are increasingly bullish for 2021 and 2022—and willing to offer executives unexpected flexibility to navigate the crisis.

COVID-19 Investor Pulse Check #1 | March 20-22, 2020

BCG’s ongoing survey provides insights on the US market and economy direct from the portfolio managers and senior analysts making buy, sell, and hold decisions right now.

BCG Investor Perspectives Series | Past European Editions

BCG Investor Perspectives Series: Q2 2025 | April 9–10, 2025

The unprecedented shift in US trade policy influenced European investors’ views. Only 19% reported they were bullish for 2025, and 58% expected their home market to face a recession.

The unprecedented shift in US trade policy influenced European investors’ views. Only 19% reported they were bullish for 2025, and 58% expected their home market to face a recession.

Weekly Insights Subscription