Hiltrud Werner, former head of integrity and legal affairs at VW, describes how BCG helped the company through a fundamental crisis.

Our Approach to Risk and Compliance Consulting

We believe in data-driven, technology enabled compliance risk management that puts talent and culture at the center while optimizing and maturing corporate compliance operations.

We help build advanced end-to-end credit processes to enhance clients’ efficiency while substantially improving the quality of credit decisions.

We work with clients to manage financial risk and compliance across the production supply chain. We start by quantifying the spectrum of trading-related, operational, and strategic risks.

We blend technical expertise with risk management processes and controls to reduce our clients’ vulnerability while boosting their capacity for rapid response and recovery.

We help clients accelerate their transition to net zero and ESG conformity. We support measurement and scenario analysis and integrate ESG principles into risk management and compliance practices.

We work with clients to develop best-in-class analytics solutions and support better risk management and compliance decision making.

Our risk and compliance consulting team uses a holistic approach to balance sheet, funding, and liquidity management to achieve superior results from a risk-return perspective.

We help clients establish clear guardrails to reduce the likelihood of reputational damage or regulatory penalties.

We provide strategic, transformational, and technical offerings in risk and compliance, which include—but also extend well beyond—financial risk consulting and compliance consulting. We take a comprehensive view of financial and non-financial risks, including operational and strategic risks. This enables us to help our clients grow their businesses while staying ahead of key risks, anticipating regulatory shifts, and instilling ethical practices—all of which helps earn the trust of employees, stakeholders, investors, and the public.

Client Success in Risk Management and Compliance

Automotive Industry

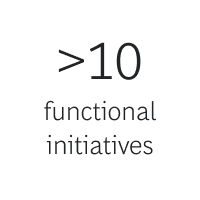

A world-leading automobile manufacturer engaged us to design and roll out their global integrity and compliance program. This tremendous transformation program was built on two key pillars: implementing processes and inspiring people. The program strengthened governance and processes: more than ten functional initiatives were rolled out across more than 500 legal entities across the globe. In addition, all company employees have been actively engaged along the journey via a diverse set of communication, training, information, and enablement initiatives—embarking on the path to achieving sustainable culture change.

A world-leading automobile manufacturer engaged us to design and roll out their global integrity and compliance program. This tremendous transformation program was built on two key pillars: implementing processes and inspiring people. The program strengthened governance and processes: more than ten functional initiatives were rolled out across more than 500 legal entities across the globe. In addition, all company employees have been actively engaged along the journey via a diverse set of communication, training, information, and enablement initiatives—embarking on the path to achieving sustainable culture change.

Payments and Transaction Banking

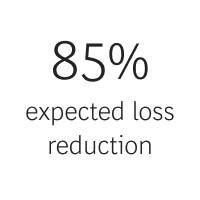

A market-leading merchant acquirer with a strong footprint in travel and airlines engaged our risk management and compliance and payments teams for immediate crisis response, gaining strength and resilience while continuing to onboard new clients even in the midst of the crisis. We reduced the client’s exposure by more than one-third and expected loss by approximately 85% during the crisis, while doubling the profitability per transaction volume in high-risk verticals.

A market-leading merchant acquirer with a strong footprint in travel and airlines engaged our risk management and compliance and payments teams for immediate crisis response, gaining strength and resilience while continuing to onboard new clients even in the midst of the crisis. We reduced the client’s exposure by more than one-third and expected loss by approximately 85% during the crisis, while doubling the profitability per transaction volume in high-risk verticals.

Energy

Utilities have been severely impacted by dramatically elevated market volatility in European gas and power prices. For a leading utility, BCG identified >€5B of reduced liquidity exposure through a rebalanced gas and power portfolio. We simulated and defined an adjusted hedging strategy, recalibrating the triangle of market, credit, and liquidity risk, and improved financing structures to significantly improve working capital.

Utilities have been severely impacted by dramatically elevated market volatility in European gas and power prices. For a leading utility, BCG identified >€5B of reduced liquidity exposure through a rebalanced gas and power portfolio. We simulated and defined an adjusted hedging strategy, recalibrating the triangle of market, credit, and liquidity risk, and improved financing structures to significantly improve working capital.

Insurance Industry

For a regional life insurer, we reworked the company’s balance sheet management framework and optimized the balance sheet and capital position through a targeted set of initiatives. The project took the company from losing money to profitable within a few months, and it set the firm up to earn a double-digit return on capital over the coming years.

For a regional life insurer, we reworked the company’s balance sheet management framework and optimized the balance sheet and capital position through a targeted set of initiatives. The project took the company from losing money to profitable within a few months, and it set the firm up to earn a double-digit return on capital over the coming years.

Video

May 26, 2023

Press Release

Experts provide clients with a holistic view of current and future policies and regulations, leveraging deep industry and tech expertise.

Our center brings clarity and action to the intersection of geopolitics and business, merging BCG's analytical strengths and geopolitical insights.

AI Transformation for Future-Ready Functions

We meet often with CEOs to discuss AI—a topic that is both captivating and rapidly changing. Drawing on our experience with thousands of AI programs, we are sharing a series of playbooks designed to help senior executives navigate their AI transformation journeys and turn AI’s potential into real profit.

Meet Our Risk Management and Compliance Leaders

Our risk and compliance consulting experts couple deep technical expertise with strategic orientation, working shoulder-to-shoulder with clients through their toughest crises and compliance risk management challenges. We stay a step ahead, ensuring our clients are prepared for tomorrow.

Explore Our Insights on Risk and Compliance

Article

March 18, 2025

By standardizing and simplifying workflows, integrating advanced technologies, and adopting production steering, banks can boost efficiency, cost savings, and service quality.

Article

February 13, 2025

With both capital costs and external risks on the rise, banks need to build a performance-oriented culture at every level.

Explore More

Capability

Compliance and Crisis Management

Capability