In the wake of Russia’s invasion of Ukraine, our global food systems are struggling to feed those most at risk.

Russia’s invasion of Ukraine has led to a major humanitarian crisis, not just in Ukraine but also around the world. Given the region’s importance as a breadbasket to the world, the impact on key food commodities such as wheat and sunflower oil has been immediate, resulting in massive shortages and price shocks. What’s worse, Russia is a key producer of fertilizers and of the energy needed to distribute available food and to grow more.

According to the World Bank, global food prices are on track to rise 23% this year, after having risen 31% in 2021, and the cost of the inputs and fuel required to produce and move the food that the world will need tomorrow is also rising. The result: immediate distress and the likelihood of reduced farm yields for as long as the next four years.

We live in a world where more than 40% of caloric intake comes from just three crops—wheat, corn, and rice. Production of these grains is concentrated in just a few regions, and a scant few players dominate each step of the value chain. Because of this high level of concentration, disruptions in the supply chain in any critical region can have devastating ripple effects across the rest of the world. Many countries that are most exposed also suffer from high debt loads and uncertain weather conditions attributable to climate change.

An estimated 1.7 billion people—most of them in developing economies—could suffer greatly, due to severely heightened levels of food insecurity, energy prices, and debt burdens, according to the UN Task Team for the Global Crisis Response Group. And the effects will be felt disproportionately. Most residents of countries where food makes up less than 10% of consumer spending (such as the US, Australia, and the UK) will be modestly impacted by rising food prices. But the effects will be far more severe in the many countries around the world where food comprises over 40% of consumer spending (including Pakistan, Guatemala, Kenya, and Nigeria, to name a few) and for the most vulnerable populations in every country.

Critically, the looming global food crisis isn’t about the world’s capacity to produce enough food. Rather, it is about the inability of our food systems to store and distribute enough food—and the inputs that are needed to produce it securely and equitably—in the face of the disruption caused by the war in Ukraine. Global trade is and will remain an integral part of modern food systems. But many problems that have arisen are symptoms of larger, systemic issues in our long, highly intermediated, complex, and fragile global supply chains.

In this article, the first in a series exploring the impact of the Ukraine war on global food systems, we explore the nature and effects of the current crisis and examine how our food systems can be shaped to react quickly when humanitarian needs are most pressing. Critical to the solution is the ability to give people everywhere the means to take matters into their own hands, minimizing the impact of the crisis by ensuring that they have the inputs and tools they need to grow and access sustainable, affordable, and nutritious food, now and in the longer term. In an upcoming article, we will explore a series of key scenarios for the future of the world’s food systems and look at ways to strengthen the resilience of the global food chain through the lens of those scenarios.

Insecurity on the Rise

The war in Ukraine began less than three months ago, but its negative effects on global food systems—coming on top of higher food and fertilizer prices brought on by the COVID-19 pandemic—have been swift. Although the immediate causes of each crisis differ, this is the third major food crisis we’ve faced in the past couple of decades, including the rapid escalation of food prices in 2007–2008 and again in 2010–2011. (See “Not Learning from the Past.”) Several factors underlie all three crises, including chronic underinvestment in local food systems by both governments and the private sector, and a lack of the diversity, resilience, and flexibility needed to respond rapidly to sudden shocks related to weather, market disruption, or geopolitical conflict. However, the current crisis could be far more catastrophic than those that have preceded it.

Not Learning from the Past

The 2008 food price crisis was the culmination of several forces—some of them long-standing trends in global agriculture, and others the result of shorter-term market distortions. Taken together, they illustrate the interconnected nature of the global food system.

First, due in large part to a lack of investment by governments and the private sector, as well as to adverse weather conditions in key growing regions, the system had experienced a long-term slowdown in the growth of agricultural production. Grain stocks declined in the face of rising holding costs and the perception that there was less need to maintain stocks in an economic climate of liberalized global trade. By the end of 2008, world food stocks had dwindled to their lowest levels since 1982. Meanwhile, energy prices were soaring, further increasing food production costs.

More immediate trends included increased speculation in commodity futures, which exacerbated the volatility of commodity prices, and increased production of biofuels, partly in response to high oil prices.

Food prices fell soon after the 2007–2008 crisis, only to rise again in 2010–2011. Over the next decade, those prices remained relatively high, as nations adopted various measures to protect their domestic markets—only to create a range of negative impacts on medium- to long-term food prices, along with additional trade restrictions.

While the immediate causes of the current crisis may differ, the ultimate conclusion remains the same: our global food systems are poorly designed to protect the most vulnerable from the impact on food prices of long- and short-term trends that are far beyond their control.

First, the supply of food available to a large portion of the world—predominately cereals and edible oils, which are staples worldwide—is falling. Together, Russia and Ukraine supply about 12% of the total food calories traded around the world, and both are critical exporters of key commodities such as wheat (28% of global trade) and sunflower oil (69%). The UN’s World Food Programme (WFP) buys from Ukraine half of the wheat that it distributes around the world. Even more alarmingly, as exports from these countries tumble, other leading food-exporting countries have announced export bans or licensing restrictions designed to protect their own food stockpiles. For example, Indonesia, which produces roughly 60% of global palm oil supplies, recently banned all exports of palm oil products. The impact on countries that rely on imported food has been severe.

As a result, prices are skyrocketing—not just for food, but for fertilizer and fuel as well. The FAO Food Price Index averaged 158.5 points in April 2022, 30% above its value in the corresponding month last year. Outstripping inflation in most countries, these increases significantly reduce household purchasing power, especially for the most vulnerable populations, which typically spend the highest share of their household income on food. Prices of staple commodities are increasing in countries around the world. Wheat prices have increased 18% in Kenya, for example, and the price of imported rice has risen a shocking 50% in Haiti. Even the US Consumer Price Index, often seen as a proxy for food price inflation, is going up, jumping 8.5% in March, the highest year-on-year increase since 1981.

Just as troubling is the increase in the cost of key agricultural inputs, notably fertilizer and fuel. For example, the price of Black Sea urea, a key fertilizer ingredient, exceeded $900 a ton in March 2022, up from $350 a ton in March 2021, due to a combination of sanctions and transport disruptions. Rising fertilizer prices mean that farmers in both net-importing and net-exporting countries must revise their plans—planting fewer crops, planting different crops that have lower fertilizer requirements (such as fewer nitrogen-hungry cereals), or skipping fertilizer altogether and hoping for the best—all of which can damage the global food supply chain. Because about half of the world’s people rely on food outputs that use fertilizer, a drop in fertilizer supply could severely affect exposed populations for up to four years if action is not taken immediately to boost supplies. And the ripple effects of disruptions to the fertilizer supply chain will reach consumers worldwide.

The war’s impact on the price of fuel has been equally dramatic. Aside from the added cost to farmers of the fuel they need to power their equipment, last-mile inland transportation can account for as much as 40% of food costs in many developing countries. So as fuel prices go up, the total cost of food increases, creating a vicious cycle.

Making matters worse, the current crisis coincides with high debt levels in many developing economies, due in part to public spending in response to the challenges presented by COVID-19. As a result, governments are struggling to support fast-rising food, fertilizer, and fuel costs—and in many cases are rolling back food subsidies or eliminating them altogether.

Adding to the pressure on global food systems is the current La Niña weather phenomenon, which, if it plays out as it did in 2012, will further depress the 2022 global harvest. Droughts in the Middle East are already pointing toward poor regional harvests, and the March heat wave in India has adversely affected India's wheat crop, reducing the country’s anticipated output to 6% below initial estimates. Hungary just experienced its fourth consecutive winter drought, and harvests in the south of Brazil are likely to be adversely affected by lack of precipitation.

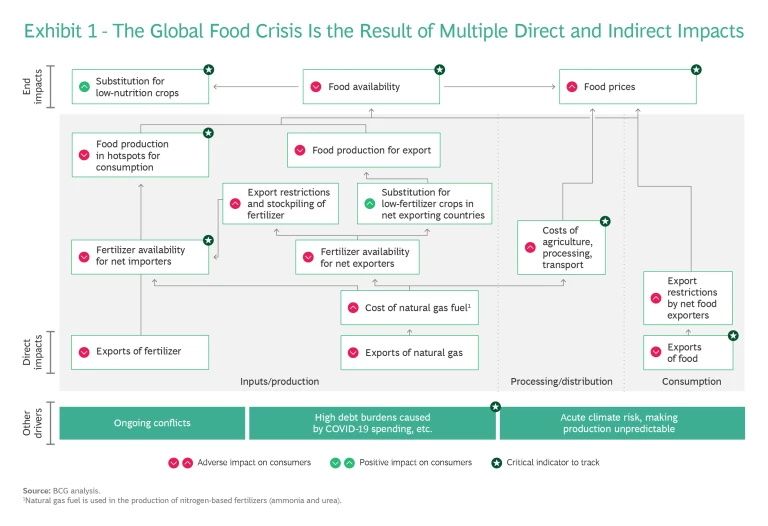

According to the UN, 193 million people in 53 countries already faced “acute food insecurity” in 2021. That number was 40 million higher than the previous record level in 2020. Now, Russia’s invasion of Ukraine has strained fragile global food systems to the breaking point. (See Exhibit 1.) The full effects, in both the short term and the medium term, have yet to be fully revealed.

Global Consequences

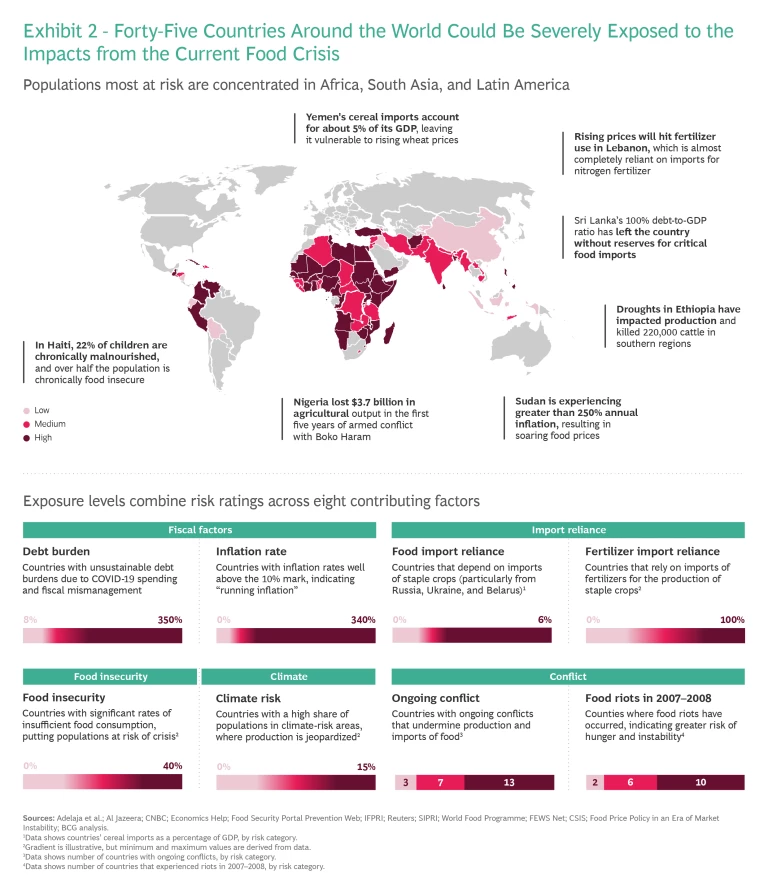

As the combined near-term impact of food and energy price continues to increase, food insecurity—exacerbated by countries’ mounting debt burden—will have devastating consequences for large portions of the global population. Our preliminary risk assessment highlights 45 hotspots around the world that are enduring some of the worst effects of the crisis. (See Exhibit 2.)

Classification as a high-risk country reflects exposure to a variety of potentially harmful factors. Virtually all countries in this classification face severe levels of extreme poverty, compounded by the ongoing economic and social challenges associated with the COVID-19 pandemic. Additional factors include heavy reliance on food imports, high import bills, high inflation, a high debt burden, climate risks, and civil unrest.

This perfect storm of factors means not only that this is a near-term crisis, but also that any reprieve over the next couple of years could be unlikely. The burden on smallholder subsistence farmers who produce food mostly for their own and their family’s consumption will be especially severe. Therefore, it is critical to give them the means to protect themselves from the effects of repeated food crises.

Rapid Response

Currently, food systems are not structured to respond adequately during times of crisis—and so far, we seem to have learned little from the crises of the past. Relieving the current crisis requires, most importantly, a coordinated and immediate emergency humanitarian response by all stakeholders—governments, development institutions and banks, NGOS, and private companies—to meet people’s most pressing needs by providing humanitarian aid, including food, financial support, seeds, inputs, tools, and technical assistance to support in-country sustainable intensification and other crop substitution actions. In addition, multilateral institutions and bilateral creditors should pursue debt relief and restructuring to give affected countries much-needed financial liquidity so that their governments can provide emergency safety net funding and support livelihood activities.

At the same time, stakeholders must also consider the possibility that the war in Ukraine, and thus the global food crisis, will not end any time soon. With this possibility in mind, they must develop solutions that address both globally traded commodities and in-country production to prevent the prolongation or worsening of the global food crisis. Any solution must include preemptive actions designed to give the most vulnerable people the means to ensure their own food security in the medium term. Exhibit 3 lays out the key recommendations for all stakeholders.

Multisectoral Partnerships

Multisectoral coordination and, where possible, new partnerships are critical for sharing the data that stakeholders need to better understand the global stocks and trade flows of critical grains and oil crops, to identify populations that are most exposed to the crisis, and to explore the best immediate solutions (such as whether and where to provide food assistance or cash assistance). By working together, stakeholders can also promote innovation at all points along the agricultural supply chain.

To improve market transparency and prevent speculation in agricultural commodities, countries—especially net exporters—should work together in good faith to share data on inputs, production, national stockpiles, and strategic grain reserves, and detail the circumstances under which food can be released from them. Determining ways to include data on private grain stocks is critical to ensuring full transparency. These measures will not only address the current crisis but also provide early signals to help stakeholders understand weak points in globally interconnected food systems and adopt measures to prevent future crises.

Governments of Donor Countries and Net Exporters

The first order of business for donor countries is to fully support and fund the WFP and other humanitarian NGOs that provide food assistance in Ukraine and in other regions that have been immediately affected by the war. Governments, especially net exporters of grain such as the US, Canada, Australia, and India must quickly develop a coordinated strategy to release grain stocks and pre-position key food commodities where the need is greatest. They should also consider increasing the production of key commodities to make up for potential supply gaps stemming from the crisis.

Donor countries should also consider investing in expanding the WFP’s real-time monitoring of structural indicators related to food, such as the prevalence of insufficient food consumption, beyond the current remit of approximately 30 countries.

Financial assistance will also be necessary to restore or replace essential agriculture and food distribution infrastructure damaged in the war and to ensure that Ukraine’s private sector has the means to import the inputs it will need to plant next year’s crops. Over the longer term, maintaining official levels of development assistance will help build food system resilience beyond the immediate impacts of the war.

Donor countries should also direct emergency humanitarian assistance to smallholder farmers outside Ukraine—particularly in sub-Saharan Africa, South Asia, Central America, and small island states —to supply them with the seeds, fertilizer, and other inputs they need to minimize disruptions to the current planting season, along with the tools and digital services they will need to boost sustainable production in the future. Such support could include, for instance, the introduction of food and fertilizer import facilities for the most exposed countries.

Governments of Countries Most at Risk

The first order of business for governments in this group is to secure food for their most vulnerable citizens, working closely with WFP and NGOs. Next, they should focus on exploring the range of actions available for encouraging smallholder farmers to boost production of a diverse set of grains (both staples and alternative, nutritious crops) and oil seeds. This effort should include increasing support for seeds, retargeting subsidies to focus on poor smallholder farmers, improving access to credit (especially for women smallholders) through the G20’s Global Agriculture and Food Security Program and similar programs, and instituting minimum price supports for key crops. At the same time, although subsidies and minimum price supports can be instrumental in making sufficient nutrition available, countries that deploy these measures should have a clear plan for phasing them out over time to avoid significant and sustained market distortions.

Governments should also work to strengthen visibility into their country’s agricultural system and supply chain, and they should invest in collecting the data and digital tools needed to drive better decision making. Another important step is to participate in and strengthen available regional trade agreements, especially those in highly exposed geographies. Full ratification of the Africa Continental Free Trade Agreement, for example, would encompass a market of 1.2 billion people and a combined GDP of $2.5 trillion, creating the world’s largest trading bloc, which could unlock tremendous agribusiness gains

The Private Sector

To the extent possible, companies in the private sector must continue to support Ukraine’s farmers and its private sector by providing key inputs for planting, growing, and harvesting the upcoming year’s crop. In addition, further deployment of innovative technologies, business models, and data-sharing mechanisms will permit more efficient and effective food production in Ukraine and elsewhere. This will likely require collaboration across industries and with governments to share production, stockpiling, supply chain, and other relevant data through clearinghouses to ensure the availability of key inputs where needed.

One need only look at how COVID-19-related disruptions pushed agricultural market actors in many parts of the world to accelerate the adoption of digital tools, leading to far greater transparency into agricultural data information and enabling better aggregation of smallholder farms' products. In addition to supporting Ukrainian farmers, the private sector should consider investing in new financial vehicles to support small and medium-size enterprises—including farmers—in countries where ensuring sustainable production at scale will require innovation and financial resources.

Private sector companies should also support the production and scaling of innovative and nutritious grains through the development and formulation of whole grains and blends (using crops such as millet, sorghum, and amaranth). Promoting research and development, pricing, sourcing, and logistics for these nutritious grains can promote wider availability of more nutrient-dense food at more attractive prices.

Finally, companies should balance the immediate food needs stemming from the crisis and the potential for long-term growth in emerging markets against their interest in near-term profits. By exploring the full spectrum of ways to achieve food access and ability to pay, companies can preserve fair pricing for those most in need.

Multilaterals and Development Institutions

The World Trade Organization should consider exempting the WFP and similar organizations from country-imposed restrictions that limit exports of food and inputs, and it should take further measures to streamline food purchasing for other emergency food assistance programs.

Multilaterals and development institutions can also collectively help strengthen systems such as the G20’s Agricultural Market Information System (AMIS) in its efforts to provide greater market transparency and to identify ways to include private commodity stockpiles in market databases. In addition, they should consider convening experts on transportation and supply chain management issues to explore creative ways to use land transport to move grains from the prior Ukrainian harvest to market.

These institutions should also investigate the use of cash transfer programming—such as food vouchers, agro-vouchers, essential household item vouchers, cash, and value vouchers—to help exposed populations afford to buy food as costs rise. Where cost effective, these programs can provide countries with greater operational flexibility and create multiplier effects.

Finally, restructuring debt or creating debt swaps to bolster smallholder resilience and strengthen social safety nets can help reduce economic shocks and increase stability in many heavily indebted countries. Multilaterals should also revisit the G20 common debt-serving framework and advocate for innovative financial mechanisms that could help increase economic capacity in highly exposed countries.

NGOs and the Social Sector

NGOs, like all stakeholders, must continue to provide immediate humanitarian relief to Ukraine’s population and to its farmers. These organizations should advocate for countries to increase food aid and ease export restrictions on food and fertilizer, and for government negotiators to strengthen regional trade agreements to reduce restrictions on trade in food.

NGOs should also work with both net-exporting and net-importing countries to develop a coordinated approach to increasing access to fertilizer and other agricultural inputs and to improving the sustainable efficiency of fertilizer use. Greater in-country support and technical assistance are also necessary to promote the sustainable intensification of key crops. Examples include supporting the 1.5 million Sri Lankan farmers who relied on chemical fertilizers before the government imposed an import ban on chemical fertilizers, with the goal of helping them make better use of available fertilizers and thus prevent potential decreases of 30% to 50% in the yield of key crops such as rice, as well as the resulting price hikes.

Like multinationals and development organizations, NGOs should explore cash transfer programming. Direct transfers can improve people’s overall economic security by increasing their food security and reducing their asset depletion, both of which will be critical in the near term for supporting highly exposed segments of the world’s population across various hotspots.

The Way Forward

First things first. The global community must immediately address the humanitarian needs of those affected by the current food crisis—in Ukraine most of all, but in the rest of the world as well.

The current crisis also demands that we try, once more, to rethink and repair our food systems, making them more equitable, more resilient, and more responsive in times of great need. Avoiding more such crises in the future will require diversifying food production across diets, supply chains, and markets and addressing issues of indebtedness, economic inequities, and market distortions that have contributed to the current crisis.

We owe it to the millions in need, now and in the future.

The authors would like to acknowledge the contribution of Emily Fletcher, David Lee, Nicole Barman, and Jaidev Phadke to this article.