That traditional media companies have struggled to migrate to a digital world is not news. The transition has taken longer than originally anticipated, and shareholders have lost faith in the sector, driving the share price of music labels, newspapers, and magazine companies to historic lows.

It may be news, however, that the cash flow for most of these media properties is far stronger than their valuations suggest. The market is treating many traditional media companies as if they will be out of business soon. But even in the worst-case scenarios, that just is not so. Most traditional media companies have far more endurance than investors believe.

If media companies make the right changes in their financial policies—particularly to their debt levels and ratios, dividends, and buybacks—and create a clear and compelling case for their long-term health, they can both lift their stock prices and attract more patient investors. The way to accomplish these goals is through a comprehensive approach to total shareholder return.

Pursuing Shareholder Return

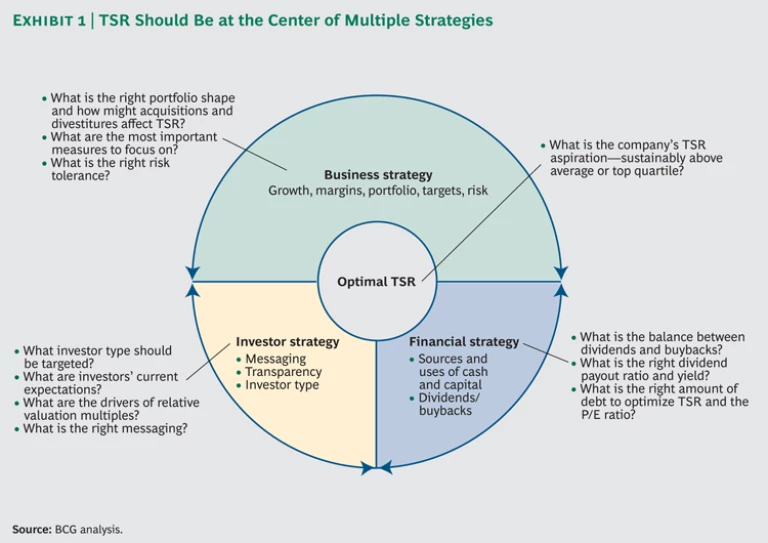

Rather than falling victim to self-fulfilling prophecies, media companies need to start using the full set of levers available to them for improving TSR. (See Exhibit 1.)

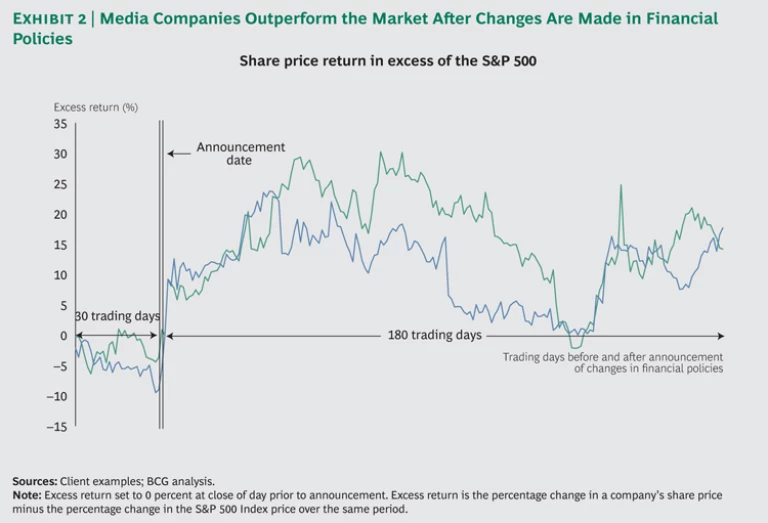

Two recent media clients substantially increased TSR by raising their dividends. Their actions created a minimum shareholder return of 5 to 6 percent annually—even without earnings growth—and provided an immediate boost to their stock prices. (See Exhibit 2.) With just a modest year-over-year improvement in earnings, both companies ought to generate sustainable shareholder returns of at least 6 to 8 percent, which is well within investors’ expectations. (See “Back to the Future: Investors Refocus on Yield,” BCG 2012 Investor Survey, April 2012.)

Yet media companies need to understand that they should not focus solely either on transforming their business or on satisfying shareholders. They must do both, working on all three sections of the wheel depicted in Exhibit 1. To date, many executives have understandably been training their attention almost entirely on operations and strategy and have lost sight of how they can generate returns for their shareholders in the near term—not in the distant future. Counterintuitive or even courageous as it may seem, many media companies can significantly increase their total cash payouts or reduce debt, or both, without jeopardizing future investments in the business. Among S&P 500 and S&P Midcap 400 stocks, those that have annual EBITDA growth of up to 5 percent over the past five years and dividends yields exceeding 3.5 percent have an average price-to-earnings multiple greater than 15. Most traditional media companies have not seen such a high multiple in years, but it is within reach.

Reshaping the Message to Investors

Media companies traditionally have attracted investors who understand the business. In the U.S., Mario Gabelli and Warren Buffett long ago recognized the franchise value and predictable growth and margins of these companies.

Today, however, the sector is largely attracting “deep value” investors, many of whom have no inherent interest in media companies beyond their worth as undervalued assets. We recently interviewed the investors of two traditional media clients. Most of the investors had only one media stock in their portfolios. They said they were buying “cheap” cash flow, and many would sell as soon as the market recognized the arbitrage opportunity. Few were committed to the companies’ futures or the future of the industry—a significant change from the historic profile of media investors.

Most media companies are allowing themselves to be defined by these deep-value investors. But by adopting a comprehensive TSR approach, they can start to frame their own stories and attract long-term investors who both understand the fundamentals of the industry and are willing to earn steady returns while media companies reconfigure their businesses for the digital era.

The Future Is Now

Media companies have the capacity to return cash to shareholders because they have managed their existing businesses well during tough times. And for now, they can continue down that path. But in the next three to five years, they will eventually run out of room to maneuver.

As part of their overall value-creation strategies, media companies need to start to pivot their businesses toward market opportunities. Many of these companies have valuable brands and hidden assets that have not been fully exploited. Within the context of a revised approach to investors based on their secure cash flow, companies can start actively managing their current assets and selectively seeking digital assets to round out their portfolio.

While these strategic and operating moves many not pay large dividends in the near term, they will set the foundation for future growth. In the meantime, traditional media companies have an excellent, integrated value-creation story to tell investors. They just need to execute it.