Telematics, the wireless technology that delivers safety services, route information, and entertainment to motor vehicles, presents auto insurers with a significant opportunity to create new value. By utilizing the technology’s ability to transmit precise data on vehicle location and driving behavior in nearly real time, insurers can de-average pricing models, capture a greater share of the low-risk-driver market, cut the costs of managing claims, and enhance the overall customer experience.

The telematics landscape is still evolving, of course. But different types of stakeholders—including automakers, telematics service providers, wireless network providers, and hardware companies—have been busy getting into position and forging future strategies. Insurers, for their part, are gradually becoming more active in developing telematics-based coverage. Nonetheless, customer penetration remains low.

A series of recent interviews conducted by The Boston Consulting Group revealed that the hesitancy of some insurers to increase their investment in telematics might be based on misconceptions about the technology’s potential for creating value. At the same time, many insurers are aware of the data advantage that telematics can bring and of its vast commercial potential. In our view, the moment is right for insurers to further explore the telematics opportunity.

Tapping into the Technology

Telematics uses the satellite-based Global Positioning System and other wireless technologies to track the movements of vehicles and monitor driving behavior. This capacity to measure exactly when, where, and how a car is driven—including the g-force impact of a collision—has the potential to revolutionize the motor insurance industry through usage-based pricing. Instead of such traditional elements as age, address, and past driving record determining the premium, a driver’s current behavior behind the wheel becomes the significant factor. The value proposition for customers is basic: the safer your driving—as established by, for example, driving frequency, speed, rate of acceleration, route familiarity, and road conditions—the lower your bill.

Although more than 70 insurers worldwide currently offer telematics-based products, penetration is no greater than 1 percent in most markets—roughly 3 million policies globally. Italy is the most advanced market, with 19 of its top 20 insurers participating and a penetration rate of 3.5 percent. Italian insurers expect penetration to rise to 10 to 13 percent within the next few years.

Other major markets such as the U.S. (where 10 of the top 25 insurers participate) and the U.K. (8 of the top 10) are also in the game. According to our interviews, U.K. insurers expect telematics penetration to rise from less than 1 percent of policies now, to 7 to 10 percent within three years—and to around 15 percent within five years. In Japan, many automakers are installing telematics equipment into new vehicles, and interest among Japanese insurers is rising.

Growth in telematics-based insurance solutions will be driven by the various stakeholders’ openness to change and will differ by market. Competitive dynamics will obviously play a role, as more insurers vie for advantage in this growth area of their industry. The rate of customer uptake will also be critical, particularly in high-premium segments such as young drivers.

Moreover, some potentially game-changing forces may provide momentum. For example, new regulatory measures such as eCall—a pan-European initiative scheduled for 2015 that will enable faster location and rescue of car accident victims through the use of telematics—could boost consumer adoption. So could the fact that more automakers in many markets are thinking of installing telematics systems as standard equipment. Furthermore, the EU Gender Equality Directive, as well as the possibility of new legislation concerning age discrimination, may limit insurers’ ability to use traditional gender- and age-based pricing methods. Should such constraints arise, data gathered by telematics devices will be that much more useful.

Yet given the potential benefits, why has telematics penetration remained so low? According to our interviews with insurers, automakers, and other stakeholders, wider adoption may be hindered by some common misconceptions.

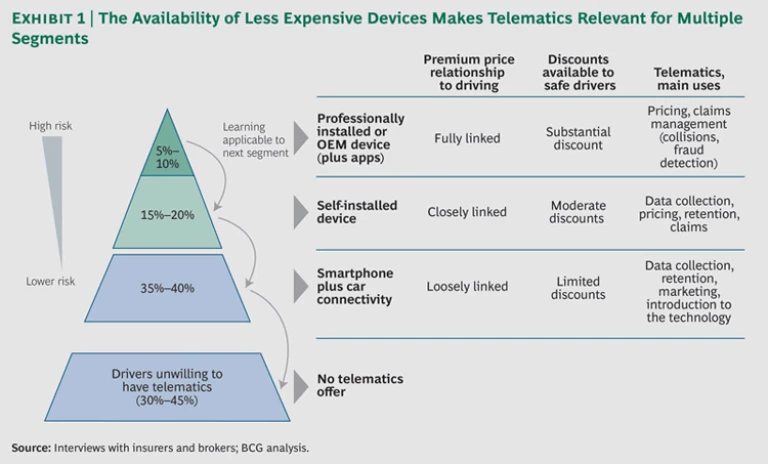

For example, some insurers think that telematics might be too expensive, requiring the professional installation of costly, state-of-the-art black boxes in vehicles. In fact, as lower-cost hardware and software—such as self-installed boxes and smartphone apps—gain more acceptance, these approaches will likely reap significant telematics benefits at a reduced cost. This in turn will make the economics of telematics relevant not just for high-risk segments such as young drivers but for medium- and low-risk segments as well. (See Exhibit 1.)

The key to winning will be smart customer segmentation. Insurers need to find the right telematics product, value proposition, and hardware device for each segment. Such alignment will widen the appeal of telematics for market groups such as women, young families, and early adopters of technology who are not necessarily in traditionally high-premium segments.

We also observed from our interviews that some insurers think that a small product portfolio is sufficient to make them viable telematics players—hence their relatively low levels of investment. In truth, there is not much, in terms of learning and economics, that insurers can do with a negligible telematics offering. A certain degree of scale is needed to gain real competitive advantage and generate profits.

Of course, in order for insurers to maximize the benefits of telematics, they need to understand more than just the common misconceptions. They must also know how to generate real value from the technology.

Generating Real Value Using Telematics

In our experience, telematics-based solutions can lift the combined ratio 15 to 20 percentage points over the traditional auto-insurance book. These benefits stem from numerous sources, including enhanced ability both to gather detailed information on driving behavior and to select lower-risk clients. More broadly, long-term advantages come from the ways in which telematics changes key elements of the insurance value chain. Consider the following elements of insurers’ operations.

Pricing. Telematics allows insurers to select individuals from broad actuarial groups. Such granular segmentation can lead to a climate in which the insurers with the most innovative pricing models are certain to attract the lowest-risk customers, leaving higher-risk customers with other providers. The flow of accurately priced customers to the telematics product can cause the risk profile of drivers served by traditional insurance to deteriorate, pressuring nontelematics insurers to raise premiums. Insurers that offer telematics coverage can thus benefit from an influx of consumers seeking lower premiums, from reduced exposure to risk, and from retention of low-risk policyholders.

Indeed, since a driver’s current behavior behind the wheel—as opposed to age, address, past driving record, and other traditional factors—is a significant element in determining the premium, a safe driver has an incentive to join a telematics program. And since telematics provides a set of personalized driving data that is neither attainable through standard underwriting nor currently transferable to other insurers, drivers have good reason to stay with their insurer.

Although insurers are just beginning to use data gleaned by telematics devices, the data have the potential to provide significant competitive advantage. A key challenge for insurers will be building the internal skills, capabilities, and infrastructure to take full advantage of the data that telematics can furnish.

Claims Management. With instant notification of accidents, more accurate assessments of who is at fault, detection and deterrence of fraud, and the ability to sort out claims more quickly (ahead of other interested parties such as automakers and attorneys), telematics can revolutionize claims management processes and efficiency—and lower insurers’ costs at the same time.

The ability to capture such benefits will not come overnight: insurers must learn how to fully exploit the technology. In the long term, however, the results will be well worth the effort. Our analysis suggests that telematics can have as significant an effect on claims management as on pricing, although relatively few insurers have yet acted on either opportunity.

Loss Prevention. Leading insurers recognize the need to manage losses across the entire life of the policy. Telematics can help them bridge underwriting and claims points in several ways. For example, installation of the telematics box provides an opportunity for collecting additional information—such as the general condition of the client’s vehicle. Such data can enable insurers to alert drivers ahead of time of potential malfunctions that could be dangerous. For instance, recently developed technology allows insurers to inform drivers if the tires on their vehicles are not adequately inflated. Moreover, insurers can frequently provide driving feedback to policyholders through a Web portal or smartphone app, thereby encouraging better driving behaviors and developing patterns of meaningful interaction with the customer. Such regular contact can also boost customer loyalty and retention.

Commercial Strategy. If insurers can devise the right service offering at the right time for the right segment, telematics provides a golden opportunity for them to clearly differentiate their value propositions. This, in turn, can have a positive influence on customers’ perception of policy value. Indeed, leading players are trying to make motor insurance more service based, as opposed to primarily product and risk based. Telematics, with the range of services that can be provided in the event of an accident, lends itself naturally to this strategic shift.

Although some insurers still see telematics-based solutions as applicable primarily to young drivers, the use of self-installed devices, smartphone apps, and other innovative approaches can indeed change the playing field. Insurers may want the most sophisticated, fraud-proof, professionally installed devices for young drivers (in order to ensure data accuracy), but lower-cost devices should be sufficiently robust to provide insurers with highly useful data on medium- and low-risk customers. Proper segmentation, as well as a true understanding of the risk profile and potential value of each customer, will help insurers avoid cannibalizing their other existing businesses.

Telematics also influences the relationship between insurers and their sales channels, especially when agents are involved. There is a physical element of the product—the black box—to manage, and also, as premiums evolve from the flow of driving data, so do commissions. Agents in the Italian market, for example, initially resisted telematics because they feared potentially lower commissions. But the market has evolved. More agents now see telematics-based policies as clear and concrete value propositions that they can leverage to sell additional and profitable types of coverage. Moreover, they correctly perceive telematics as a way to protect their customer base from direct players. At one insurer we interviewed, more than 30 percent of customer acquisitions in the first half of 2013 were attributable to telematics-based policies.

Taking Action Now on Telematics

The evolution of telematics poses both opportunities and risks for insurers. In the short term, penetration is expected to grow steadily in most markets. But data asymmetry among players and the lack of well-defined data standards mean that early movers—using the superior data advantage that telematics provides—will be able to cherry-pick the best drivers currently being served by competitors, as well as retain desirable customers already on their books for longer periods of time. Winning insurers will seize this opportunity to make profitable gains in market share. The risk will fall mainly to those insurers that maintain the status quo and do not prepare for the anticipated growth in telematics.

In the medium term, as telematics becomes increasingly mainstream, regulators are likely to push for common data standards, as well as the easy transference of devices and data among insurers. In the long term, with so many forces exerting downward pressure on premiums, winning insurers will be those that have superior pricing, claims management, and loss prevention capabilities—all of which can clearly be enhanced by telematics, implying a strong need to get an early start in the game.

Moreover, interest by other stakeholders is poised to intensify. Automakers, for example, are increasingly moving into the insurance space—becoming more active in sales, distribution, and claims—much as they have become key players in financing new-vehicle sales over the past decade. For telcos, telematics represents a growth area for communication volume, making it a sizable strategic opportunity. Some telcos are already acting as telematics service providers to the insurance industry. And although the price element alone—lower premiums for safe and infrequent drivers—should provide ample motivation for consumers to explore a telematics-based product, insurers should also emphasize safety and security features as major benefits of the overall experience.

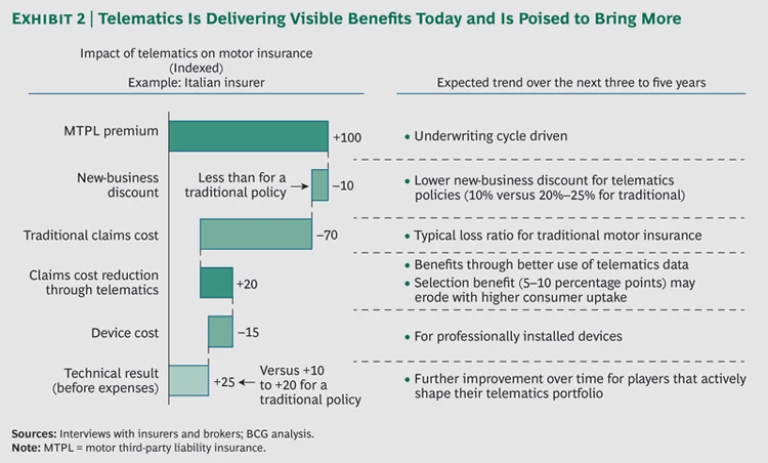

To be sure, the world is “going digital” in countless ways. Growth in telematics-based insurance will very likely be a part of this megatrend. With hundreds of millions of cars on the road worldwide, the implications are enormous. In the Italian market, for instance, telematics is already delivering visible benefits and is poised to bring more. (See Exhibit 2.)

In thinking about telematics, insurers in every market should consider the following truths:

- Installing telematics in motor vehicles is a pioneering step in the use of smart devices.

- Designing and using smart devices to monitor risks in real time will be critical for the insurance industry going forward.

- Big-data technology is a large part of this trend and will allow insurers to analyze large sets of data both to draw conclusions for risk selection and to customize coverage.

- Motor insurance is a first mover in telematics. But the same or similar technology could be applied to other types of insurance such as cargo, marine, household, and health.

Ultimately, insurers need to adapt their strategies and capabilities in order to be ready for growth in telematics. They should ask themselves how they might benefit from leveraging this innovative technology. Perhaps even more important, they should ask themselves another question: What are the consequences of being left out of the telematics game?