With subscribers’ thirst for data seemingly insatiable, these should be heady times for mobile network operators. Spurred by smartphones, 4G networks, and bandwidth-intensive applications like video, global mobile data traffic grew 81 percent in 2013, according to Cisco’s Visual Networking Index. And no slowdown is in sight: by 2018, traffic is expected to be nearly eleven times greater than in 2013. Yet many telcos are experiencing flat, and even declining, revenues.

To get an inkling of the source of the problem, one need only shop for a new mobile plan. In many cases, price is still centered around voice and messaging. But for telcos, these are declining assets, making up a diminishing share of network usage and contributing decreasing margins. Over-the-top (OTT) services offer free or inexpensive alternatives to traditional voice and messaging, and more and more consumers are using them. According to the market research firm Telegeography, Skype added 54 billion minutes of international voice traffic in 2013—50 percent more than the combined volume growth of every telco in the world.

Forward-thinking providers have gotten the message: pricing should be centered around data. This lets them monetize the extraordinary growth in that traffic and, crucially, make the economics of the business work. The growth in data requires huge investments in network capacity—investments that can pay off only when revenues are aligned with usage.

In The Boston Consulting Group’s work with telcos around the world, we are seeing the emergence of new practices that are the right ones for today’s data-driven mobile environment. Savvy telcos are dropping unlimited-data plans in favor of tiered “buckets.” They are also adopting multidevice and multiuser plans with shared data bundles. To better manage declines in voice and messaging—and monetize those businesses as well as possible—many are moving to flat-rate, all-you-can-use plans for these services.

Yet as sensible as these ideas are, telcos need to do more than embrace them. They need to offer the right mix of features at the right price points and design plans that are tailored to customer preferences and market conditions. That means tackling several challenges:

- Ensuring that the profitability of data increases in direct proportion to the high capital expenditure required by today’s mobile networks

- Ensuring that the business model is not at risk if voice and SMS business volumes continue to decline

- Ensuring that the large investments made in smartphone subsidies pay off

- Ensuring that plans are as attractive as possible to consumers

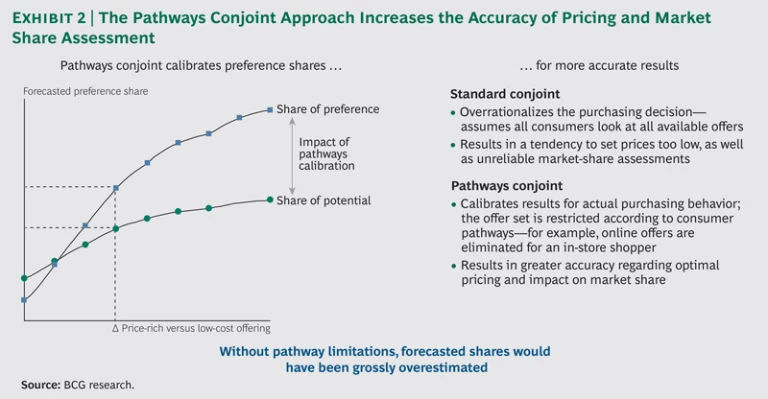

Traditionally, many telcos have turned to a technique known as conjoint analysis to fine-tune their pricing models. Adopted by a host of industries, it involves putting combinations of features and prices—that is, the offer attributes—before consumers to determine how preferences and price sensitivities influence purchasing decisions. Although conjoint analysis can indeed be helpful, we have found that it rarely establishes optimal pricing. It turns out that when making actual purchasing decisions, consumers tend to focus on specific attributes important to them. So instead of considering all offers, they consider only a subset, such as those made in-store or from a particular vendor. As a result, they demonstrate less price sensitivity than conjoint surveys would indicate—and prices set through conjoint analysis are generally set too low.

Providers need a more accurate method for pricing plans. To that end, BCG has developed a new methodology, one that doesn’t replace conjoint analysis but rather calibrates the results to reflect actual purchasing behavior. It does this by identifying and factoring in the different “pathways” consumers take when they consider “real” offers. By understanding these pathways, providers home in not only on the most favorable price levels but also on the features and services that customers, in fact, want most.

BCG estimates that this new approach—called “pathways conjoint”—can boost margins for the same target of gross adds by up to 10 percent over traditional conjoint-based pricing. This is growth that would otherwise be left on the table. And it can be obtained far more easily and quickly than providers might expect.

Building a Better Plan

Before telcos can employ pathways conjoint, they need, as always, to develop the general contours of their mobile plans—parameters that BCG’s approach will then help them refine. Although there is no perfect template for creating a modern, data-centered mobile plan, BCG has identified an essential group of practices that provide a solid starting point.

Implement more data “tiers,” at a stable price per megabyte. Mobile operators have largely moved from unlimited data plans to tiered data buckets—a sound policy that allows them to provide similar value to customers at less risk to themselves. But often pricing hasn’t been linear: larger buckets tend to cost far less per megabyte than smaller buckets. That gives users an incentive to buy more than they need—a nice model for the moment, but one that could prove unprofitable as usage goes up.

A better approach is to increase the number of data buckets offered and price them in a more linear fashion. This will steer customers to the tier that most accurately reflects their current usage, while enabling their evolving needs to be monetized. The key is to provide an easy upgrade path to the next bucket, which can be accomplished by eliminating steep overage penalties and instead simply up-selling to the next tier. For operators that already have a high share of subscribers to large or unlimited-data packages, creating a meaningful up-sell path will require a slightly different approach, such as offering new buckets that limit data volume but offer higher speeds.

Embrace multidevice and multiuser plans with shared data. With the growth of smartphones and tablets, households and individuals possess more devices than ever. Telcos can take advantage of this trend by moving beyond traditional one-SIM-card contracts and letting multiple devices share one bundle of data. This will bring a number of important benefits. (See Exhibit 1.) For one thing, it will allow providers to price data higher than for a standard one-SIM-card plan, as customers can still realize savings over the multiple individual plans that they would otherwise need. Higher data prices, in turn, allow telcos to offer additional SIM cards at low cost—an incentive for customers to add more devices and more shared data as well.

Multidevice customers are more likely to stick around, too, as the economies of scale can make it simply too cumbersome for them to switch everything to a new provider. As early adopters like AT&T and Verizon have demonstrated, multi-SIM-card plans can result in higher average revenue per user (ARPU) and stabilized or reduced churn. (Both providers saw roughly a 1 percent rise in ARPU six months after introducing shared plans.) Operators in both the U.S. and Europe have also reported increased cross-selling of similar or related products after implementing such plans.

Take a fresh look at subsidies. Smartphone subsidies tend to be far more costly than those for more basic phones (in Europe, they typically run €100 to €200 more per handset). And they can be risky. Given the off-network uses of smartphones, telcos can end up footing the bill for an expensive gadget if they don’t carefully design their plans. Yet there is good reason to keep these subsidies. They make plans more attractive to customers who want the latest phones. The devices generate an outsized amount of usage—in 2013, smartphones accounted for 27 percent of global handsets but 95 percent of data traffic, according to the Visual Networking Index. And—no small point—telcos that have dropped subsidies have often seen their market share fall as well. Moreover, subsidies bring opportunities. With high demand for smartphones and an easy way to pay for them, handset financing could become a profitable separate business for a telco. Operators should keep their financing structures straightforward, though. Subscribers are more likely to embrace simple monthly payments than a complex leasing arrangement.

Set a fixed ARPU for voice and text. The impact of OTT players on traditional voice and text volumes isn’t likely to subside. Indeed, Juniper Research estimates that, by 2018, OTT services like WhatsApp are expected to control 75 percent of all mobile messaging traffic. In light of this trend, providers might consider offering flat-rate, unlimited-use voice and text for all but their low-end packages. By doing so, they can protect their business model from drop-offs in usage. Yet here, too, operators should proceed carefully. Some may find that there is still some value in voice allowances.

Ideal Pricing: A Unique Approach

Although the aforementioned practices can steer telcos in the right direction as they develop packages, data-centered plans also add complexity. In a voice-dominant world, network costs were traditionally treated as fixed. But in a data-dominant environment, they are closely tied to usage. (See “How Telecoms Can Manage the Mobile Data Explosion,” BCG article, May 2012.) More demand requires more capacity, which requires more investment—costs that must be factored into pricing. Meanwhile, the new ideas outlined here are just that: new. Most telcos don’t have a lot of experience zeroing in on the right levels and mixes of these plan attributes.

This is where pathways conjoint earns its keep. By helping telcos understand the actual pathways consumers take when they consider offers, it provides insights into the trade-offs subscribers are willing to make when purchasing a plan. In our case work, for example, we found that roughly a third of mobile subscribers in France, Germany, and the Netherlands follow a distinct “loyal customer” pathway when considering offers. These consumers focus on offers from their existing provider. Meanwhile, another 11 to 15 percent of subscribers focus on high-end handsets. In both pathways, cost is likely to be a secondary consideration—and consumers are more amenable to a higher price than a traditional conjoint survey would indicate.

BCG’s methodology is designed to deliver and apply such insights. The process consists of three main steps, which telcos can usually complete in just 9 to 12 weeks.

- Qualitative Assessment and Identifying Consumer Pathways. In one-on-one interviews, consumers are asked questions that allow operators to identify the features they are interested in (from shared data to high-end smartphones to network speed and quality) and the various pathways they take when making purchasing decisions (loyal customer, online shopper, and so on).

- Quantitative Assessment—Conjoint Survey and Calibration. Employing a large survey sample of about 2,000 consumers, traditional conjoint techniques are used to quantify the demand and price elasticity for proposed plan features. Mobile operators can then estimate a share of preference for different pricing models. This result is calibrated with the pathways uncovered earlier by restricting the consideration set to offers relevant to each pathway. Operators end up with a share of potential for each new pricing model—a far more accurate predictor of its effectiveness. (See Exhibit 2.)

- Business Modeling and Fine-Tuning on Price. Modeling techniques are used to assess the subscriber gross-add potential of the proposed pricing plans. But the plans aren’t tested in a vacuum: competitive responses are also simulated. Depending on how rival plans affect gross adds, final tweaks to pricing may be necessary.

Pathways conjoint has already been battle tested with some of the world’s leading mobile operators. For one client, a major European provider, we estimate that the methodology will add an additional 2 percent to its gross-adds share. Traditional conjoint techniques had overestimated price elasticity, but by identifying consumer pathways we were able to obtain a more accurate picture. Meanwhile, the qualitative assessment lets us zero in on the most promising value-added services, which included free access to the provider’s Wi-Fi hotspots, voice roaming minutes, and the ability to lock a lost device and delete its data.

Telcos will also find that pathways conjoint can be applied to other emerging pricing challenges, such as repricing current customers to support cross-selling and retention—and pricing fixed-mobile convergence offers, something that is high on carriers’ agendas.

For mobile operators, the focus has rightly been on innovation: finding profit in new technologies and compelling new services. But how they package these innovations will make all the difference. Consumers want features and pricing models designed for the new ways they buy and use devices. Providers, meanwhile, have to get pricing right if their big-bet investments in mobile data capacity are to pay off. Pathways conjoint provides insight that enables both customers and operators to get optimal results—and value.