Mining and Metals in a Sustainable World 2050 will be a dominant topic on both public and private agendas. The world must, in the face of continued increases in population and per-capita consumption, find a way to live within its environmental means and to protect finite resources.

Related article: Mining and Metals in a Sustainable World 2050

This imperative has profound implications for the mining and metal industry. Value chains will shift. For example, recycled scrap is increasingly replacing primary resources as a production material. Consequently, primary producers may face reduced demand. Companies along the mining and metal value chain will need to understand these changes so that they can prepare for and respond to them.

Steel provides an excellent proxy for understanding the implications of these changes for the mining and metal industry as a whole. It is a key commodity in value chains for multiple other commodities, including automotive and construction. It drives demand for commodity markets, in particular iron ore and coal. Recycling of steel is more advanced than that of many other metals; 85 percent of discarded steel is reused, although as yet only 39 percent of steel production input is recycled scrap.

The Outlook Scenarios

The Boston Consulting Group, working with the World Economic Forum and building on its own steel model, analyzed the changes confronting the industry, with an outlook through 2050. We compared two scenarios, “keeping a green line” and “true change.” The first scenario assumes that the current steel market will in many parts remain constant, and the second assumes a more sustainable world in which significantly more recycling occurs and use of resources is more circular.

Mining and metals will continue to play an important role in the world economy in both scenarios, but the projected outcomes differ, thus offering sharp insights into the possible future of steel (and, to some extent, other markets within the mining and metal sector).

Both scenarios rely on the same assumptions about the underlying steel demand. Among the most critical: steel intensity (that is, the amount of steel used per given output) will drop slowly in most developed regions, sales growth in China will continue to slow and will begin to approximate levels in Europe, and steady growth will characterize the new steel-consuming nations of India and Africa. The two scenarios share the same underlying steel-demand assumptions, with production overcapacity remaining prevalent for the next decade.

Keeping a Green Line. In this scenario, some of the main elements that drive steel production now will remain constant: the regional split between the two main types of steel-processing infrastructure (basic oxygen furnaces and electric arc furnaces), the share of scrap used for a given output of steel in the regional basic-oxygen-furnace route, and the current regional scrap-collection rates.

Even in this scenario, the use of scrap in the steel-making process will take on a more important role over time, with a corresponding decline in demand for primary resources (iron ore and metallurgical coal).

True Change. This scenario explores a worldwide switch from primary production to scrap recycling. It predicts waves of regulation in Europe, the U.S., and China to mandate increased recycling in the steel production process. In this scenario, steel producers would be forced to increase their use of scrap, rather than primary materials, as a source of steel.

Such changes would happen only if economically feasible—that is, if prices for secondary (recycled) material become more attractive relative to primary extracted material. Regulation will support the process and affect prices but will unlikely be so strong that it will threaten whole industries.

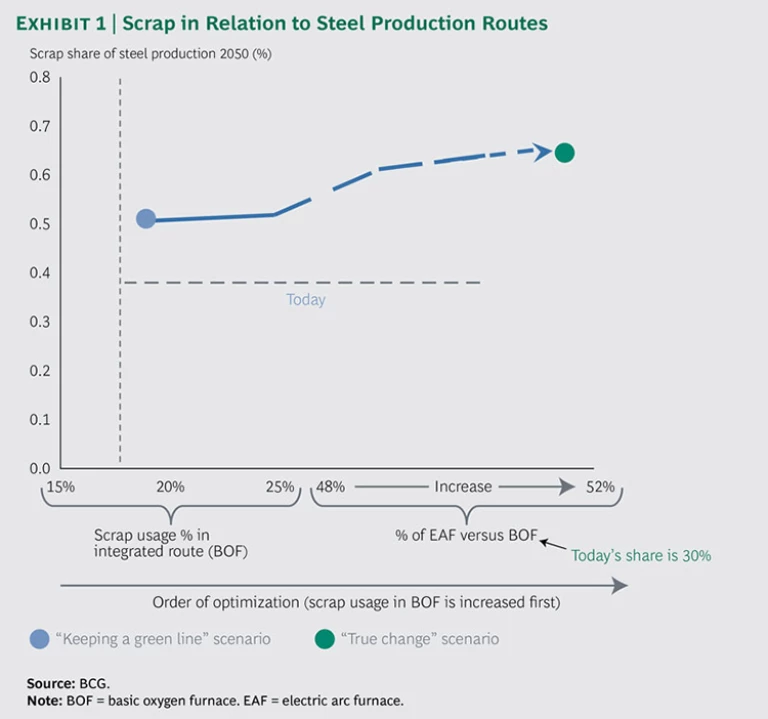

In the “true change” scenario, the use of scrap increases significantly in both main processing routes. Worldwide, the scenario envisions, both routes would use scrap to maximum capacity: 25 percent for the oxygen routes and almost 100 percent for the electric routes. The shift will also be driven by China’s increasing adoption of electric arc furnaces, whose share of production will rise from 10 percent in the next decades, assisted by fresh flows of scrap resulting from China’s late industrialization and an increase in collection rates to more than 90 percent. (See Exhibit 1.)

Conclusions

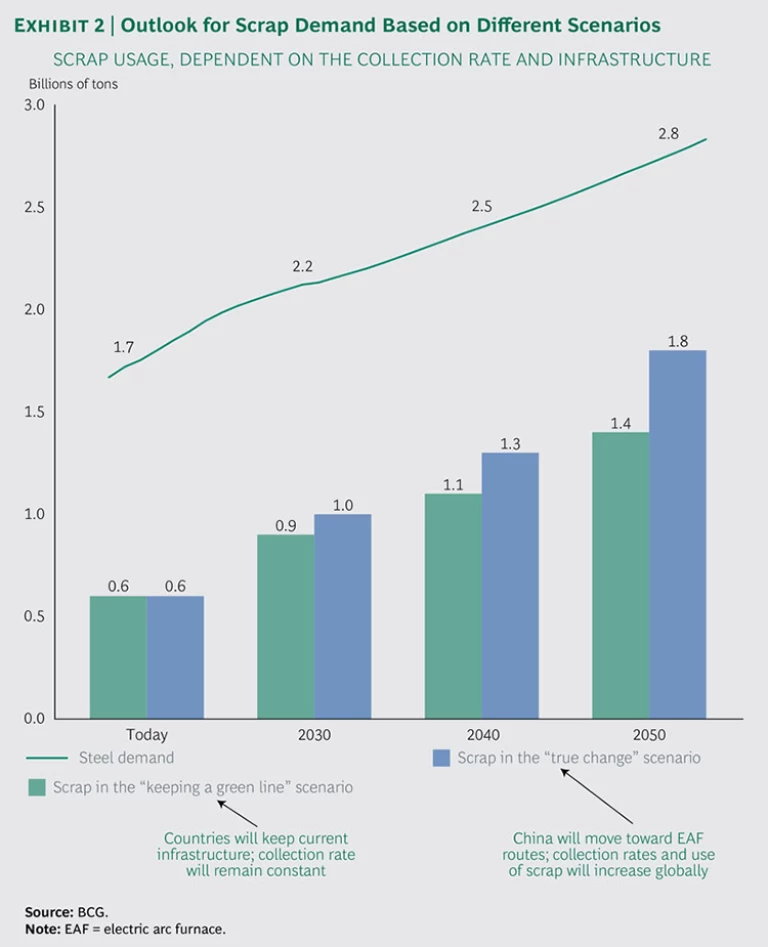

Demand for scrap steel will increase dramatically. Even in the more constant first scenario, approximately half of the projected 2.8 billion tons of total global steel production in 2050 will rely on recycled scrap. In the second scenario, of course, recycled scrap will be increasingly dominant, constituting close to 70 percent of the 2050 global total, and primary steel production will increase only marginally over today’s levels. (See Exhibit 2.)

The model also enabled projections of demand for other primary steel-making materials, such as iron ore and metallurgical coal.

In the first scenario, demand for these two commodities will continue to increase although growth will slow. In the second scenario, the focus on recycling and the consequent sharp increase in demand for scrap will reduce demand for iron ore and metallurgical coal beginning in 2020 and approximating today's levels by 2050.

The “true change” scenario is a bold forecast. It will not happen by itself. It would require concerted action by governments and the industry to incentivize the shift, make it financially feasible, and drive change. Other factors—such as global growth and material substitutions—will play a role in determining future recycling rates.

The stronger the move to recycling, the greater the implications for metal players. In particular, a significant switch such as that described in the ”true change” scenario could require metal providers to adapt their business models, possibly redefining themselves as material providers, integrating primary metal, recycled material, and substitute products.

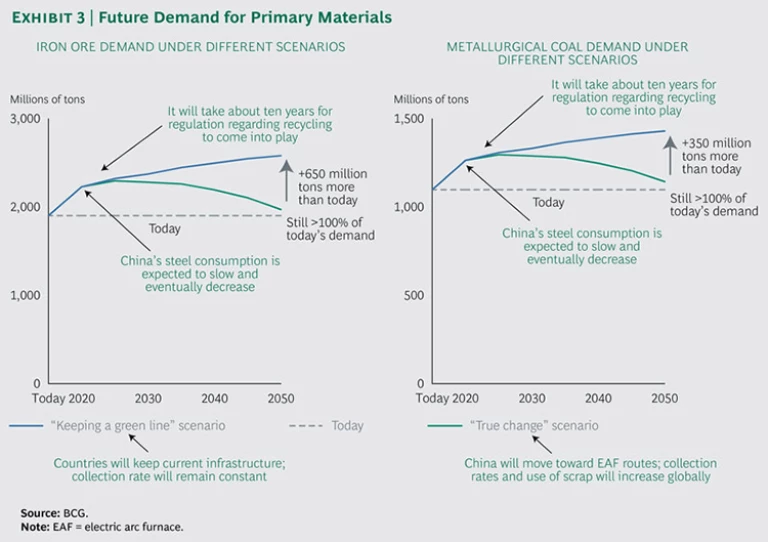

For mining players, the different scenarios mean different things. The “keeping a green line” scenario envisions limited changes. Demand for iron ore and metallurgical coal would grow by more than a third over today’s levels. In contrast, the “true change” scenario envisions that demand for these two commodities will remain at current levels. (See Exhibit 3.) The extraction of primary resources will retain a key role in both scenarios, but if the “true change” scenario comes to pass, companies on the right side of the cost curve (that is, those with high production costs) will experience considerable pressure.

Mining and metal companies need to monitor these developments, consistently assessing their position in a more sustainable world and reflecting upon different scenarios for the future.