This article is an excerpt from 2016 ECS Value Creators Report: Building Endurance, the 2016 Value Creators Report.

Digital technology is revolutionizing the way engineering, construction, and services (ECS) companies operate, presenting tremendous opportunities for value creation. For example, BCG estimates that digital technology will eventually lead to annual cost savings of $700 billion to $1.2 trillion for the ECS industry. The biggest savings will probably be in institutional building, transportation, energy, and communications.

Recognizing the opportunity, leading ECS companies have increased their adoption of digital technologies. At the core of these technologies is building information modeling (BIM): a digital representation of a project’s physical, functional, and planning characteristics, applied to boost efficiency and effectiveness. (See The Transformative Power of Building Information Modeling, BCG Focus, March 2016.) Some countries, such as the UK, are mandating the use of BIM for government-funded projects, thereby speeding adoption of the technology.

Examples of applications for digital technology in ECS include:

- Real-time data sharing, integration, and coordination through the cloud

- Data-driven construction planning and lean execution

- New fabrication methods (such as 3D printing)

- Automated and autonomous construction

- Rigorous construction monitoring and surveillance

Companies are using such applications to boost productivity, manage complexity, reduce project delays and cost overruns, and enhance safety and quality. In addition to pursuing these objectives, ECS companies are expected to increase their technology spending in order to capture the benefits of cloud computing and big data and analytics. As a result, IT spending in the ECS industry is expected to grow from roughly $110 billion in 2015 (1.2% of revenues) to $500 billion in 2025 (3.3% of revenues). This represents a CAGR of 16%.

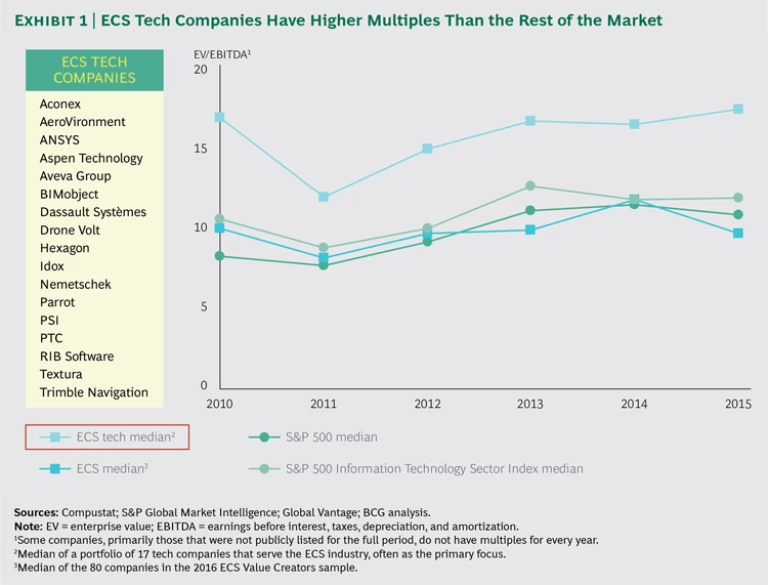

To support strategic decision making related to ECS technology investments, BCG has created the ECS Technology Index. This index, the first of its kind, is a portfolio of 17 publicly listed technology and IT companies that participate primarily or significantly in the ECS space. These ECS tech companies include providers of software, drones, robotics, cybersecurity services, and project management services. To continue to derive up-to-date insights from the index, we will refresh and expand it as ECS technologies evolve and new ones emerge.

Investors See a Bright Future for ECS Tech Companies

We compared the performance of the ECS Technology Index with that of our ECS Value Creators sample and of various US indexes. The ECS Technology Index trades at a higher multiple (a median of 16.7 times EBITDA in the past three years) than the ECS Value Creators (a median of 10.4 times EBITDA in the past three years). Moreover, ECS tech companies have a higher multiple than that of the balanced portfolio of the S&P 500 information technology index. (See the exhibit.) This pattern has been consistent since 2011, as the trading multiples of ECS tech companies have increased in line with improvements in the stock market’s performance. In another sign of the positive outlook for their performance, ECS tech companies delivered a weighted-average TSR of 12% from 2011 through 2015, compared with 2% for the ECS companies in our sample. In other words, the market sees a bright future for ECS tech companies.

ECS tech companies are growing rapidly as the industry’s adoption of technology accelerates. (See the sidebar.) Like traditional ECS companies, the tech-focused companies can capture the benefits of globalization by, for instance, participating in infrastructure projects around the world and exploiting scale. However, because their businesses entail selling software and devices, they are not burdened by the challenges that ECS incumbents must address, such as managing large projects, forging a large number of local connections to enter new markets, or coping with many competitors. But tech companies face the complexity of having to sell on a project-by-project basis with buy-in from multiple stakeholders. As the ECS industry adopts more-advanced versions of BIM, mobile applications, and digital collaboration tools, ECS tech companies can use their advantages to capture more of the value in the industry. Companies with a robust, high-performing technology division may wish to consider spinning it off to achieve the full valuation of their investment.

LEADING TECH COMPANIES DEMONSTRATE THE POTENTIAL

To better understand what generates high performance among the companies in our ECS tech sample, we categorized them on the basis of their degree of focus on the ECS industry. Two tech companies exemplify those with a medium to high degree of focus:

- Nemetschek Group, a German software company with 2015 revenue of more than $300 million, has a portfolio of 12 brands serving the architecture, engineering, and construction industries. The company covers the full design-build-manage process and has established itself as a leader in advanced approaches to BIM technology, including open BIM and 5D BIM, which facilitate collaboration among project participants. From 2010 through 2015, the company enjoyed strong growth in revenue (9% CAGR) and margins (1% CAGR, excluding revenue impact) while paying dividends (4% dividend yield). The market has rewarded Nemetschek with a five-year TSR of 40% and a three-year average valuation multiple of 18.1.

- Dassault Systèmes is a French software and services company with 2015 revenue of $3.1 billion. Initially known for its software for 3D computer- aided design and computer-aided manufacturing, the company now provides a technology platform that supports applications used for 3D modeling, simulation, business intelligence, and collaboration. Dassault has generated sustained revenue growth (8% CAGR from 2010 through 2015) by pursuing a broader product portfolio, geographic expansion, and acquisitions. The company’s strong growth has resulted in a robust five-year TSR of 17% and a three-year average valuation multiple of 20.0.

Is Proprietary Technology More Valuable In-House or Spun Off?

ECS companies need to consider the value of digital technologies from the perspective of both project delivery and corporate portfolio strategy. Portfolio strategy comes into play if an ECS company has developed proprietary technology that would be valuable to other companies. In such a case, the company needs to compare the potential for value creation of two scenarios:

- Keeping the technology in-house and capturing the competitive advantage in terms of higher prices or lower costs

- Spinning off the technology into a standalone company and capturing the shareholder value created by the higher valuation multiples that the market rewards to ECS tech companies and the additional revenues generated by commercializing the technology

To choose the right approach, ECS companies must weigh both sides. Spinning off the technology may give it the entrepreneurial freedom it needs in order to develop and allow the company to take advantage of ECS tech companies’ high multiples. Keeping the technology in-house may let it benefit from substantial internal synergies, and a company may be able to make a market for it and support it with resources that would not be available on the open market. The best approach will depend on the firm and the technology.