This article is the result of a collaboration between BCG and Climeworks, a company from which BCG has purchased offsets.

The science is clear: getting the world to net zero requires both drastic reductions in CO2 emissions and the implementation of various carbon dioxide removal (CDR) methods for actively withdrawing residual and historical CO2 emissions from the atmosphere. According to the Intergovernmental Panel on Climate Change (IPCC), the world must remove 6 to 10 gigatons of CO2 per year by 2050—and beyond.

Similar measures are necessary to achieve corporate net zero targets. An increasing number of organizations are taking a science-based approach to the climate pledges they make. Most of them are already working on roadmaps for drastically reducing emissions—the first and most essential lever for fighting climate change. But to achieve net zero, even those that can reduce their CO2 footprint by 90% will still face hard-to-abate emissions that can be counterbalanced only through high-quality CDR offsets.

CDR covers a range of methods, including reforestation, bioenergy with carbon capture and storage (BECCS), and direct air capture and storage (DACS). Funding for the development and scaling of novel CDR methods can come from the purchase of carbon offsets by companies that need to lower their carbon footprint, and from more direct investment in the technology.

One of the most promising methods of CDR today is DACS, owing largely to the reliability of the offsets purchased to fund it. Development of DACS technology is still in its early stages, however, and implementing and scaling it will take time and money. According to our analysis, in order for the technology to gain widespread and timely adoption, the cost of DACS must fall from $800 or more per ton of CO2 today to $200 or below per ton by 2050, and preferably earlier.

Reaching this goal is everyone’s responsibility, including governments, NGOs, and companies in every industry that stand to benefit. By purchasing high-quality engineered CDR offsets, companies can start now to help achieve global net zero commitments while maximizing their chances to deliver on their own corporate net zero targets.

How does DACS fit into an overall CDR portfolio for companies looking to offset their long tail of greenhouse gas (GHG) emissions, and how can companies get involved in making it a reality?

Why Companies Need Carbon Removal

Thousands of companies across every industry have announced some sort of decarbonization plan, and have set goals for reaching net zero, sooner or later. For example, more than 6,000 companies are working with the Science Based Targets initiative (SBTi) to set emissions targets in line with climate science. The range of options for lowering emissions is wide. Options for reducing energy-related emissions include improving energy efficiency, switching to low-carbon fuels and renewable energy, and (when they become available) adopting new technologies that have yet to be brought to market or scaled up, such as carbon capture, utilization and storage, and even potentially fusion energy.

All of these options can have a significant impact on companies’ direct Scope 1 and energy-related Scope 2 emissions, as well as on indirect Scope 3 emissions across their value chains for which they are responsible. But will it be enough? And can it be done at a realistic cost?

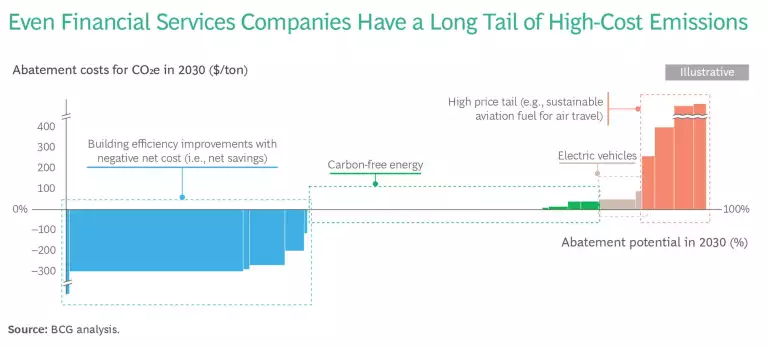

Consider the abatement challenge that a typical (hypothetical) financial services company faces. As the simplified abatement cost curve for Scope 1 and Scope 2 emissions in the exhibit illustrates, the company can achieve significant carbon and cost savings through building efficiency levers such as retrofitting heating, ventilation, and air conditioning systems and installing higher-energy efficient appliances (shown in blue). Reducing emissions by switching to carbon-free energy sources (shown in green) is roughly cost neutral, and reducing them by switching to electric vehicles has a small associated cost (shown in yellow). Pulling these three levers would enable the company to reduce about 90% of its emissions at a reasonable cost. But the remaining 10% of the company’s emissions (shown in red in the exhibit) are either impossible to abate or too expensive to abate without a significant negative financial impact on the business.

This is where permanent CDR comes in. Companies that base their net zero goals on Oxford principles, SBTi, and other scientific guidance should take the most cost-effective steps first because they must meet drastic emissions reduction targets. Then they can address the residual emissions with CDR offsets. The financial services company introduced above could use CDR to offset emissions resulting from business-critical air travel or refrigerants with high global-warming potential (the red bars in the exhibit). Companies in higher-emitting industries—such as agriculture—may need to turn to CDR to offset unavoidable Scope 1 or Scope 3 emissions as well. CDR also gives companies the opportunity to address historical emissions that continue to linger in the atmosphere.

DACS as Part of a CDR Offsets Portfolio

If we are to reach our net zero goals and slow the process of global warming, we must put every possible method of CDR to the task, and offsets are the most effective way for companies to participate. The offsets themselves should balance three factors: permanence (the removed carbon is sequestered for tens, hundreds, or thousands of years); third-party verification (the removal is monitored, reported, and verified under an accepted standard); and additionality (the removal wouldn’t have happened without the purchase). Companies should also take into account the cost of the offsets and their underlying technologies’ impact on land use. Properly balanced, these factors will maximize the value of any CDR offset, and hence its long-term contribution to decarbonization.

In this regard, DACS stands out for several reasons. According to the IPCC, it has the potential to remove from 5 to 40 gigatons of CO2 per year, significantly more than such alternative CDR solutions as biochar (a carbon-intensive form of charcoal that can be combined with soil to sequester CO2) and BECCS (a process that captures the energy latent in biomass and stores the resulting CO2).

DACS also makes efficient use of land and does not compete with arable land, thus avoiding the main limitations of large-scale, nature-based CDR solutions such as reforestation. Moreover, DACS offsets are fully additional without risk of double-counting, which makes them attractive for rigorous net zero targets. In fact, Oxford net zero principles require carbon portfolios to gradually evolve toward 100% engineered removals such as DACS by 2050.

To balance the tradeoffs across permanence, verification, additionality, cost, and land use, companies typically use a portfolio of CDR approaches. DACS and other permanent CDR techniques are likely to become a larger share of portfolios over time. Today, because of its the high cost, it commands a relatively small share, but that share is projected to grow as costs decline.

Engaging with DACS

As with most other methods of permanent CDR, the primary hindrance to wider adoption that DACS faces is its current high cost. We previously reported that a cost of around $200 per ton of CO2—and possibly lower—is necessary and achievable. Reaching this point, however, will require massive investment in the technology, including far greater financial and policy commitments on the part of governments. Just as important is the role that companies must play as they look to offset their long tail of GHG emissions and deliver on their net zero goals. Today, companies have two primary ways to buy offsets and participate in the development of DACS and other permanent CDR methods: through direct removal offset purchases, and through indirect “buyers club” purchases.

Direct Removal Offset Purchases. Companies can benefit from purchasing DACS offsets or advance purchase agreements on voluntary offset markets now. The advantage for the purchasing company lies in locking in the DACS offsets for the volume purchased and having access to future supplies of DACS offsets. For companies working on DACS and other engineered CDR technologies, advance purchases can provide needed early-stage funding to further develop the technology and build current projects. Even if companies that are arranging to buy removal offsets sign up for purchases without putting any money down, these advance commitments can help de-risk future sales and lower developers’ cost of capital, thereby helping to unlock the project financing needed to build projects.

A number of companies are pursuing these high-quality DACS offsets, typically as part of a portfolio of CDR solutions. Because the industry is young, these arrangements typically to take the form of bespoke agreements. Many financial services and technology companies, in particular, have recently announced DACS purchases, usually covering tens or hundreds of kilotons of CO2 over several years.

Pioneering companies engaged in purchasing high-quality CDR tend to be from industries such as technology, financial services, and consulting that provide services and have limited Scope 1 and Scope 2 emissions. But every company with a science-based net zero ambition, regardless of industry, should start planning its CDR purchases to offset its projected residual CO2 emissions in addition to devising its carbon footprint reduction roadmap.

Indirect “Buyers Club” Purchases. For companies that are unwilling or unable to negotiate individual agreements with suppliers of removal offsets, buyers clubs can provide simplified access to high-quality, permanent CDR purchases, including DACS. The mechanisms can be similar to direct purchases, including advance purchases and advance commitments, but they offer a wide portfolio of CDR approaches to balance quality, scalability, and cost considerations. For example, Frontier provides centralized access to CDR suppliers; NextGen gives companies the opportunity to buy into its portfolio of removal credits; and members of the First Movers Coalition (FMC) commit to buying credits for CDR and other low-carbon technologies. (BCG is a founding buyer of credits from NextGen and a founding member of FMC.)

Why Companies Must Start Today

Companies in every industry would be well-advised to develop and implement their permanent CDR strategy now. Those that wait will face two challenges. First, as demand for permanent CDR increases over the next decade, companies may find themselves with little or no access to carbon removal offsets. Already, the supply of high-quality carbon removal offsets is scarce, and as more companies look to permanent CDR to reach their climate goals, demand will grow further. As a result, competition for the limited quantities of permanent CDR offsets available is likely to intensify in the late 2020s, resulting in higher prices. This scenario would leave companies that delay unable to meet their climate goals and unprepared for the likelihood of increasingly stringent climate regulations.

Second, if too few companies invest in permanent CDR, the costs will not come down even as supply ramps up to meet demand in the longer term. Deployment is needed today to reduce costs in the future. For most CDR technologies, projects take several years to plan and build, entailing long lead times. Widespread failure by companies to act in a timely fashion could significantly slow efforts to scale permanent CDR to the levels required by science to enable the world to get to net zero by mid-century.

Companies in every industry and every sector share a responsibility to help scale high-quality CDR in two critical ways: first, to deliver on their net zero pledges; and second, to collectively shape the CDR market to the levels required to limit global warming to 1.5°C or 2°C.

They have little time left to act. Accordingly, companies should start looking for opportunities to support the technology now, while also determining their strategies for managing their future CDR needs.