With one tweet, the clock could start ticking on the end of the North American Free Trade Agreement as we know it. At any time, US President Donald Trump could announce that he is withdrawing his negotiators from ongoing NAFTA talks with Mexico and Canada and that he will take the US out of the trade deal. That tweet would be followed by an executive order beginning a six-month process of US withdrawal from the 23-year-old pact that governs more than $1 trillion in annual trade. And it would mark the end of business as usual for thousands of companies doing business in the US, Mexico, and Canada.

The three NAFTA partners are fast approaching a self-imposed deadline of March 2018 for renegotiating the pact, and very large differences on key points remain. President Trump has repeatedly threatened to pull out of NAFTA if US demands aren’t met. Such a move would likely be met with legal challenges, of course, as it is not clear that the US president has the authority to unilaterally withdraw from NAFTA without congressional approval. But it is also not clear that there would be a strong enough political coalition to save the treaty. So companies doing business in North America should prepare now for radical change.

Some business leaders still hope that the economic impact of NAFTA’s demise will be manageable. One prominent school of thought goes like this: since the US, Mexico, and Canada are members of the World Trade Organization, tariffs for most products will remain relatively low, even without NAFTA. While this may be true in the aggregate, however, average Mexican WTO tariff rates of 7.4% are about twice as high as those of the US. For some product categories, Mexican tariffs are well into the double digits. What’s more, and as we have argued previously, in sectors where US WTO tariffs are low and US trade deficits are high, the Trump Administration could well be expected to take further protectionist action in order to achieve its overarching goal of trade deficit reduction. (See “Three Things CEOs Should Do Now to Prepare for the New NAFTA,” BCG article, November 2017.) Furthermore, Mexico and Canada could retaliate against such US action by imposing restrictions on US products that currently enjoy favorable trade terms and high sales volumes into their markets, such as agricultural products, machinery, and chemicals.

Mexico and Canada could retaliate by imposing restrictions on US products that currently enjoy favorable trade terms and high sales volumes.

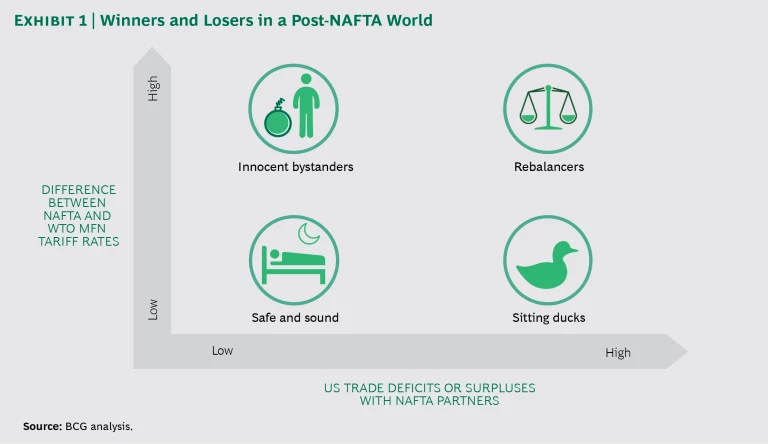

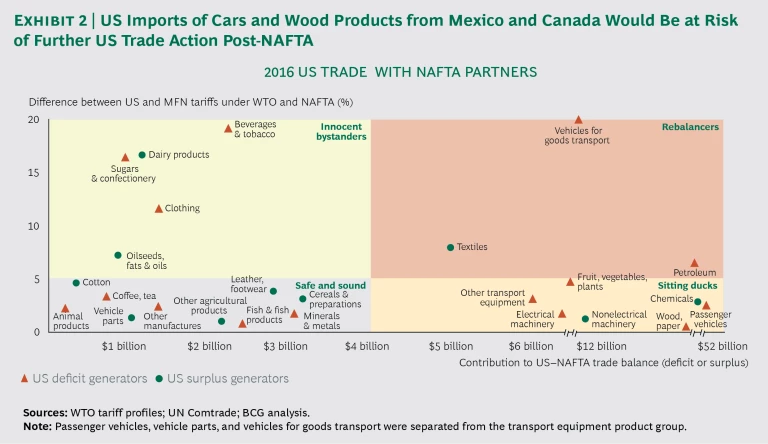

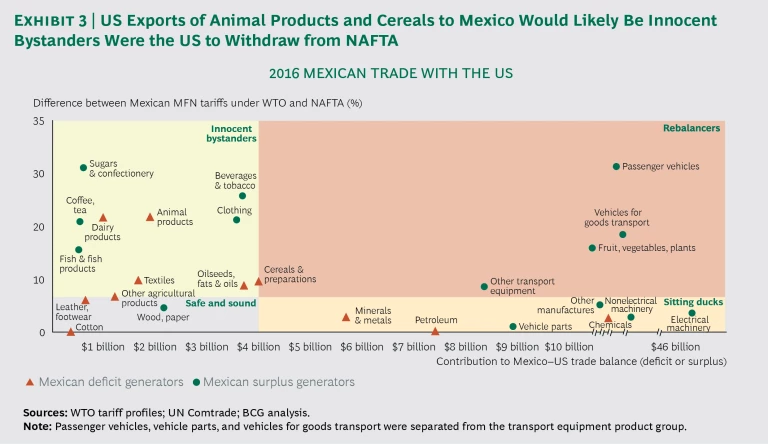

Which industries would be the winners and which the losers in a post-NAFTA world? To assess risk for specific industrial sectors, we looked at two dimensions: the degree to which an industry generates US trade deficits or surpluses, and the difference between NAFTA and WTO tariff rates for all three trade partners. It’s important to remember that each WTO member country has its own tariff schedule (so-called most-favored-nation, or MFN, rates) that applies to all other WTO members. These rates are often far from reciprocal: in the case of passenger vehicles, for example, the US MFN tariff rate is just 2.5%; but Canada’s rate is 5.8%, and Mexico’s is 31%.

Dividing Winners from Losers

We segmented industry sectors into four categories, which we designated as follows: safe and sound, innocent bystanders, rebalancers, and sitting ducks. (See Exhibit 1.)

Safe and Sound. Sectors that face little direct downside risk from a simple US withdrawal from NAFTA are those that do not generate large US trade deficits and in which there is little or no difference between NAFTA and WTO tariff rates. Safe-and-sound sectors could therefore be considered winners in a post-NAFTA world. For inbound trade to the US, coffee, tea, and cotton fall into this category. (See Exhibit 2.) Also in the safe-and-sound category are sectors in which trade is already thin because of foreign-ownership requirements or other protectionist measures permitted under the WTO. The Canadian dairy and poultry industries are good examples, as they enjoy high tariffs under Canada’s WTO arrangements.

Innocent Bystanders. Some sectors that enjoy relatively balanced trade—but that happen to have large differences between NAFTA and WTO tariff levels—could suffer greatly in a post-NAFTA scenario. These sectors, which include confections, beverages, and tobacco, are not part of the NAFTA “problem” from the Trump Administration’s perspective. US agricultural exports currently enjoy tariff-free access to the Mexican market. Animal products such as pork, cereals such as corn, and dairy products are particularly at risk of becoming innocent bystanders because a US withdrawal from NAFTA would subject them to Mexican MFN tariff rates without Mexico’s having to take any specific action. (See Exhibit 3.) It should be noted that in our analysis, Mexican trade with Canada would not be significantly affected. That is because tariff levels would likely change only for US goods; Canada and Mexico are widely expected to continue to honor their NAFTA commitments to each other even if the US withdraws.

Rebalancers. This category comprises sectors that generate either large surpluses or deficits for the US and that also have higher tariff rates under WTO rules than under NAFTA. These differences in tariffs would be significant enough to prompt manufacturers to shift production from one NAFTA country to another—and thereby make an impact on bilateral trade deficits. Light trucks such as pickups are a good example. Under NAFTA, Mexican-built light trucks are imported duty-free into the US. Under WTO rules, US tariffs on these vehicles would shoot up to 25%. So in a post-NAFTA world, automakers would be likely to relocate assembly of light trucks to the US for sale inside the US. One point that stands out in this analysis, however, is just how very few product categories, other than textiles and vehicles used for transporting goods, fall into this segment. This strengthens the point that in order to make a significant difference in the US-NAFTA trade balance, the Trump Administration would have to impose additional restrictions on imports of other types of products.

Sitting Ducks. These sectors are likely to get hit very hard by added protectionism. They contribute greatly to US trade deficits or surpluses, but a withdrawal from NAFTA would not be enough to make an impact, because US tariffs under WTO rules would remain very low. The deficit generators, such as passenger vehicles and fruits and vegetables, would be prime targets for further trade action by the US, as shown in Exhibit 2. The US MFN tariff on Mexican car imports is only 2.5%, for example, so the Trump Administration would have to hike trade barriers even further to force carmakers to shift production to the US. For trade into Mexico, chemicals and petroleum are among the sectors that can be regarded as sitting ducks. Sectors that generate significant trade surpluses for the US, meanwhile, would be natural targets for retaliation by Mexico and Canada if the US withdraws from NAFTA and imposes trade restrictions.

What Companies Must Do to Assess and Mitigate Risk

While it is important to identify which sectors are at risk, it is more critical for every company to understand how shifting trade rules will specifically affect its business. There are hundreds of tariff classifications and rates. The average tariffs we have used for analyzing overall industry sectors often mask higher and lower tariffs at a more granular, product-category level. In addition, each firm must assess its value chain. If an organization purchases its inputs and produces and sells in only one NAFTA country, it will face no direct risk from cancellation of NAFTA. But once the value chain includes activities in more than one North American country, there is risk.

Once a company's value chain includes activities in more than one North American country, there is risk.

Companies must do their homework. They must understand their specific risk profile and which steps they need to take to mitigate that risk. We suggest that sitting ducks, in particular, assess not only the risks posed by WTO tariff levels, but also the whole suite of policies that can lead to “managed trade” in specific sectors, such as quotas, seasonal restrictions, technical barriers to trade, and so-called voluntary export restraints.

Our previous article outlined three steps business leaders should take immediately: they should begin to assess the risk to their global value chains, work to influence policy, and develop a playbook for action based on several potential outcomes. Companies must also take into account the fact that the risk to the world trading system goes far beyond NAFTA; it also includes Brexit and increasing trade tensions between the US and China. (See “Adapting to a New Trade Order,” BCG article, July 2017.)

Any US move to cancel NAFTA will lead to major upheaval in industries that have built their business models around the free flow of business inputs and outputs among the three countries. It is vital that companies understand how this change will affect their competitive position and make the preparations necessary to move boldly regardless of the outcome. Indeed, companies at risk of being adversely affected should also mobilize now to try to stop the collapse of NAFTA from happening in the first place.

Acknowledgments

This article would not have been possible without the contributions of BCG colleagues Niki Lang, Raj Varadarajan, Michelle Andersen, Merih Ocbazghi, Marcela Macías, and Prateek Jain.