Carbon dioxide removal (CDR) technologies are essential to delivering the “net” in net zero. These technologies will provide a balance to anthropogenic emissions that are hard to reduce as well as reverse the buildup of historic emissions that are already present in the atmosphere.

One of these CDR technologies, direct air capture (DAC), has significant advantages over other CDR approaches. DAC can provide the highest-quality CO2 removals in terms of scalability, permanence, and verifiability. For example, DAC is more than 100 times as land efficient as reforestation, making it a more scalable solution. It can sequester emissions for many centuries, making it the most permanent of all removal options. And tracking how much CO2 has been removed is straightforward, making it more verifiable than ocean alkalinization. As a result, even though it is still nascent, DAC could play a critical role in delivering on net zero.

Even though it is still nascent, DAC could play a critical role in delivering on net zero.

In spite of this, DAC is in danger of failing to fulfill its potential because of its current high cost and comparatively low support from governments and other players with moving down the cost curve. We estimate that in order for the technology to be widely adopted, the cost of DAC (the end-to-end cost of CO2 removal including final storage) will need to fall from $600 to $1,000 per ton of CO2 today to below $200 per ton and ideally closer to $100 per ton by 2050, and preferably earlier. This cost is in line with other waste products; solid waste disposal costs in high-income countries, by comparison, range from around $170 to $205 per ton of solid waste.

This reduction in cost would dramatically accelerate demand, encouraging private developers to build more capacity and making the technology affordable for the world. (See “Can the World Afford DAC?”) However, to unlock the insights and technologies that will drive costs down, far greater capacity than is currently planned will be needed in the short term, underpinned by expectations that there will be a market for the carbon credits generated.

Can the World Afford DAC?

This is comparable to current estimates of the global spend and cost of wastewater purification each year: a combined 0.5% to 1% of current global GDP. Therefore, from a global perspective, DAC removals are a costly but by no means unaffordable solution.

BCG has modeled the greenhouse gas abatement cost curves for many industries and companies. While reducing the first 60% to 80% of emissions is very affordable for most organizations (assuming sufficient access to renewables and other existing technologies), reducing the last 20% to 40% is very expensive—often well above $150 per ton. Tackling these final emissions will require removing many obstacles, from permitting to just transitions for local communities to a host of “not in my backyard” issues. If we are serious about a net zero world, then large-scale DAC at $150 per ton or lower should be a major part of the equation.

Getting to $150 per ton for carbon removal with DAC technology would establish a clear cap on the marginal cost for tackling emissions. It would also encourage additional, non-DAC actions to remove emissions, most of which can be carried out below that price point, though not necessarily at sufficient global volumes.

Solving this challenge will require a paradigm shift. We believe that reducing DAC costs to $150 per ton of CO2 or below is achievable, but getting there is going to be a stretch. Reaching this target depends on early and dramatic progress in several areas and will require governments and other stakeholders (including carbon accounting and net zero target-setting organizations) to play their part.

DAC Costs Could Fall Dramatically

By 2050, up to 10 billion tons of CO2 will need to be removed from the atmosphere annually, according to the median estimates of several net zero scenarios considered by the Intergovernmental Panel on Climate Change. This could be done using a variety of CDR technologies, including DAC, bioenergy with carbon capture and storage (BECCS), and nature-based solutions. However, given the current emissions trajectory and the probability of exceeding the atmospheric concentrations of CO2 necessary to keep planetary warming to 1.5 degrees Celsius, we are likely to need sizeable amounts of CDR as early as 2030.

While DAC has a tremendous role to play in delivering on net zero, deployment has so far been limited. Multiple technologies are emerging, but all require a dramatic reduction in cost to reach the scale that is needed. (See “Three Potential Answers to the DAC Puzzle.”)

Three Potential Answers to the DAC Puzzle

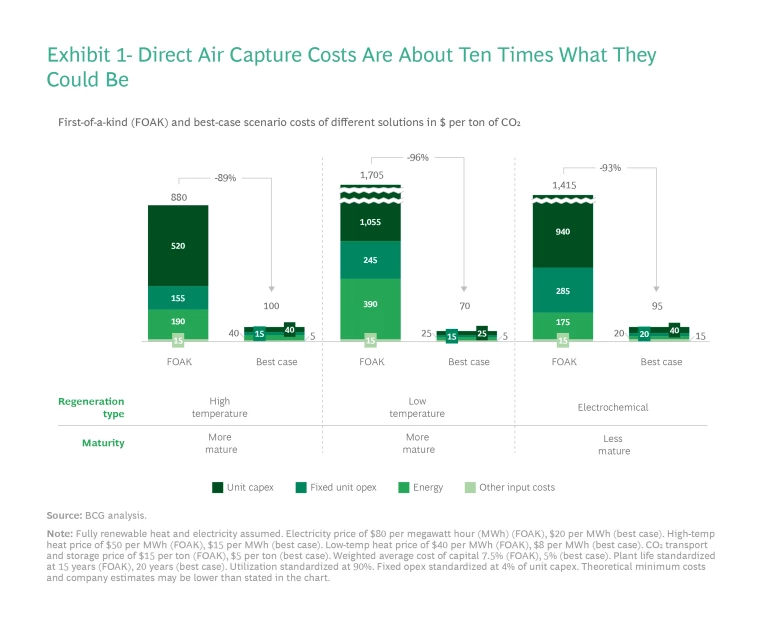

High-Temperature Heat Regeneration Solutions. Heat-based solutions are the most popular regeneration method. High-temperature solutions (at about 900 degrees Celsius) are among the most advanced and provide a viable near-term route to megaton-scale DAC technology. The heat source most widely used today is natural gas with the CO2 from its combustion captured. These solutions could face challenges as fossil fuels are phased out but in the meantime can be used to take advantage of existing abundant supply for a faster rollout. Alternative approaches that would employ electricity or hydrogen to generate the high temperatures required are also in the works.

Low-Temperature Heat Regeneration Solutions. These solutions require temperatures of around 80 to 100 degrees Celsius delivered in the form of steam. Today, this heat could originate from fossil fuels, but it would ultimately have to come from low-carbon sources, which could be a challenge. Still, generating heat for low-temperature solutions from renewables is far easier than generating heat for high-temperature solutions and could be synergistic with geothermal or nuclear plants. This approach is one of the most active areas in DAC technology development today, with multiple pilots and an operational commercial-scale plant already in place.

Electrochemical Regeneration Solutions. This group of solutions aims to solve the energy-sourcing challenges faced by high- and low-heat approaches by regenerating at ambient temperatures. It uses electricity as the only input. Electrochemical regeneration solutions are expected to require less energy and have an easier route to sourcing low-carbon energy. Because they don’t need heat, they can use power direct from renewable sources—as long as it is available 24-7. However, because electricity tends to be more expensive than heat, total energy costs could remain comparatively high.

The question is whether it is reasonable to project significant cost reductions—of 75% or more—to deliver a climate solution supported by market demand. We have examined this question deeply using BCG’s proprietary DAC cost model and our detailed analysis of seven DAC developers. We found that it is in fact possible for DAC costs to fall dramatically, even to a level below $150 per ton. (See Exhibit 1.) However, it will be a challenge, particularly given the timeframe involved. Solar installation costs have declined by more than 90% over the past 40 years. We need to deliver a similar reduction in DAC costs to achieve scale in the gigatons, but in just over half the time.

A massive step up in investments, government support, collaboration models, and broader industry engagement will be required.

Business As Usual Is Not an Option

While we believe affordable DAC is feasible, a business-as-usual approach will not get us there within the time that we have. We need to be realistic and understand the forces that are holding DAC back. Here are some of the main ones:

- The technology’s high costs mean that few customers (normally large companies) are willing to sign on to early-stage DAC projects at the scale required. At the same time, suppliers of key components aren’t investing sufficient resources in development.

- Policy support is still nascent despite recent incentives, such as the $180 tax credit for every ton of permanently stored CO2 announced in last year’s US Inflation Reduction Act.

- Companies are carrying out development within walled gardens to protect their intellectual property, rather than adopting the more collaborative approach that will be needed to drive greater learning and standardization and that will enable players to move at the rapid speed required.

- Net zero accounting standards limit companies’ ability to count CO2 removed using permanent CDR technologies such as DAC against their scope 3 targets, discouraging investment.

- Capital costs are high because investors and lenders are reluctant to put money into the technology without greater certainty around future demand.

Due to these negative forces, investment in DAC is a small percentage of the amount needed to drive the technology down the cost curve.

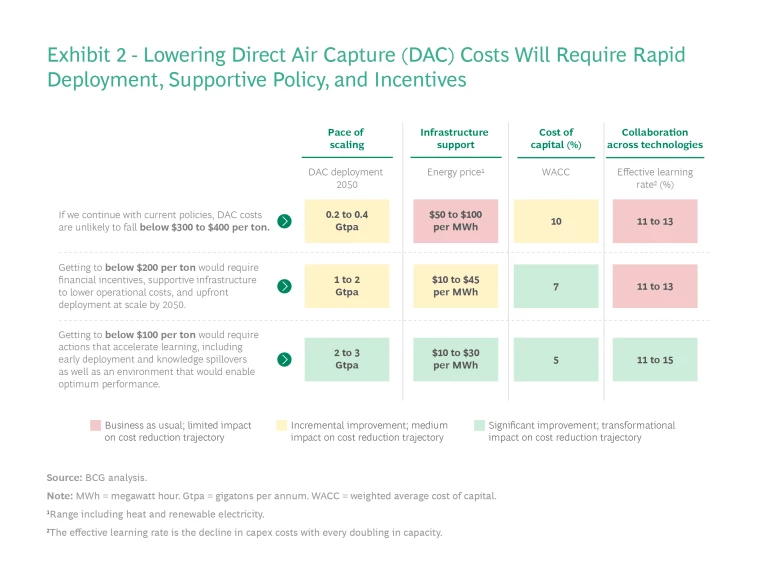

We estimate that DAC costs are unlikely to drop below $300 to $400 per ton if the status quo continues. According to our model, getting costs to $200 and below would need incentives such as far more favorable capital costs, supportive infrastructure to lower operational expenses, actions that accelerate learning, and upfront deployment at scale well before 2050. (See Exhibit 2.)

For starters, current production volumes are far below the capacity needed to make the technology truly viable. DAC plants would also have to be far larger than they are now. On the plus side, all this construction activity would deliver significant economies of scale both within individual sites and across the industry as a whole.

Due to experience curve effects and shared learning, capex costs typically decline as more capacity is deployed. In the case of gas turbines, capex costs have fallen by 15% for every doubling in production capacity. We estimate that if DAC achieves similar improvements, about one gigaton of annual capacity—requiring additional capex and opex investment of about $200 billion—will be needed to move the technology sufficiently down the learning curve to make costs attractive. With lower learning rates, the investment bill will be much higher (two to three times greater with a learning rate of 13%, for example), underlining the requirement to maximize shared learning wherever possible.

A Call to Action

Turning DAC into a viable solution for tackling the climate crisis will require action in several areas. Four near-term levers can reduce costs so that the technology is attractive, but players will need to pull hard on each one.

Accelerate shared learning to move faster down the cost curve. As governments and corporate buyers provide greater support for DAC development, they could also impose tougher requirements. For starters, they could encourage players to share their learning across the supply chain in less competitive areas such as fans, balance of plant designs, and regeneration. Furthermore, we believe that as solutions mature, investors will need to select two or three potential winners. They should focus their support on those approaches in order to accelerate development as quickly as possible while still aiming to make a return on their investment.

When it comes to capital requirements, treat DAC like a public utility. Governments often use financial and commercial guarantees and other mechanisms to help municipal waste plants raise low-cost debt because these facilities provide an essential public service. Removing carbon from the air is analogous to cleaning up municipal solid waste, so governments could take a similar approach by aiming to reduce the weighted average cost of capital (WACC) for projects from more than 10% to 7% to 8% in the near term and 5% to 7% in the medium term as DAC solutions scale up. As with municipal waste, governments could introduce legislation that stipulates that companies must comply with certain removal obligations.

The most feasible pathway for giving DAC the status of a waste removal service would be to include it in compliance carbon markets and to expand their scope. Unfortunately, the only viable markets for doing this to date are the European Union‘s Emissions Trading System and a few others. A second but less satisfactory option would be to include it in industry-led initiatives, such as the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

Substantially increase investment by changing carbon accounting rules. Each year, NASA spends more than $20 billion on space research. We may not need that amount of pure R&D money to make DAC viable—although some solutions will require more funding than others to accelerate to the demonstration phase. However, we’ll need to invest much more heavily in facilities and plants than we are doing today.

One way to unlock sources of capital could be to change the rules on how permanent CO2 removals are accounted for. As we’ve mentioned, current carbon accounting rules limit companies’ ability to count removals towards their emissions targets. However, by revising their rules on permanent removals, at least for companies’ scope 3 emissions, carbon accounting organizations would encourage investment in these technologies. For example, investments to permanently remove a ton of CO2 from the atmosphere using permanent CDR technologies such as DAC could, with the appropriate guardrails, be considered equivalent to a company reducing its scope 3 emissions by a ton of CO2. This is an area of ongoing work.

Low-cost DAC is challenging, but no more so than any other revolutionary technology.

Focus on optimal locations. For DAC to succeed, it will be critical to find geographical locations that have substantial storage potential, are able to provide abundant, cheap renewable energy or have good but stranded renewable energy resources, and meet the specific climatic requirements of different solutions. For example, local temperature, humidity, and elevation can have different effects on the performance of individual DAC technologies. To provide a sense of scale, sequestering one gigaton of CO2 each year as a supercritical fluid—the form in which it would typically be stored—would require storage capacity equivalent to 1,600 Empire State Buildings. Fortunately, this amount of storage is available today. Government and regulatory agencies and private players can help rapidly establish a robust DAC infrastructure in advantaged locations through effective permitting rules, incentives, and multilateral offtake agreements. Many of these locations can provide new sources of low-carbon energy while also enabling a just transition.

Low-cost DAC is challenging, but no more so than any other revolutionary technology. No one can say definitively what the limits on DAC improvements will be. One thing is certain, however: the stakes are incredibly high. Getting to one gigaton of DAC capacity won’t be cheap. But given the depth of the climate crisis, we can’t afford not to scale this groundbreaking technology using all means available. We must grasp the challenge and go for it.

The authors wish to thank Nako Thompson for their contributions to this article.