The global steel industry is in essence back to where it was before the recent China-led boom and has to find a way to operate sustainably within this environment. The take-off of the Chinese economy, particularly fixed-asset investment, drove a massive increase in worldwide production in seven years and led to unprecedented levels of global capacity utilization. These conditions are unlikely to be repeated.

Steelmakers are struggling again. The period of prosperity was ended by a combination of overinvestment, a slowdown in fixed asset investment, the global economic crisis, and changes in the raw-materials pricing schemes. Now they must cope with overcapacity and low margins, the same conditions that led to long-term value destruction from the late 1980s until the China boom.

The Boston Consulting Group believes that it is unlikely that anything like the China boom years will happen again soon, either in China or elsewhere—overcapacity appears to be here to stay. Nonetheless, we strongly believe that steel companies can still influence their profitability.

Steel still matters. It remains all but impossible to build or maintain functioning modern economies without its products, either for old-style infrastructure or high-tech innovations like the high-strength steel used in new lightweight auto bodies.

Yet the industry is struggling. Only a few companies are currently earning sufficient margins to ensure long-term sustainability. The average EBITDA margin for European companies fell by close to two-thirds in five years, from 14 percent in 2008 to 5 percent in 2013.

The industry faces a number of constraints. It is globally still very fragmented, and steel companies continue to be sandwiched between consolidated raw-materials suppliers and end-product manufacturers. Furthermore, a high proportion of steel goods are commodity products, and the industry suffers from a flat cost curve. A long history of investment in practically nondifferentiated assets and operational-efficiency improvements is forcing most steel companies to operate within a relatively small cost band.

Overcapacity is at its highest for a decade, bringing with it profitability issues, lack of investment, and lack of innovation. Levels of overcapacity vary across regions, and there is no agreement on its precise extent. Estimates of European overcapacity range from 30 to 80 million tons (Mt). Most companies would benefit from a reduction in overcapacity. They may wish to close down capacity so that they can balance supply and demand and increase profits, but they are reluctant to take on the costs involved and see other companies benefit.

Awareness of steel’s vital importance means that governments and other regulators will try to help the industry. Past government interventions have had—as our analyses of Europe in the 1970s and 1980s and the U.S. in the 1980s will show—only limited success. In our opinion, government interventions help the industry only when they either lower exit barriers or ensure fair competition. Often, they have done just the opposite.

Nobody doubts that operational excellence remains indispensable, particularly given the industry’s flat cost curve. But continuous operational improvement serves only to keep companies competitive. It cannot create sustainable competitive advantage and significantly affect overcapacity. Thus, the steel industry needs to find new ways to get back on track, improve profitability, and create value.

This report offers steel companies innovative insights as well as nonstandard approaches and measures to deal with this difficult environment. We believe that companies that apply these measures can create and capture more value than other industry players.

How Much Overcapacity Is There?

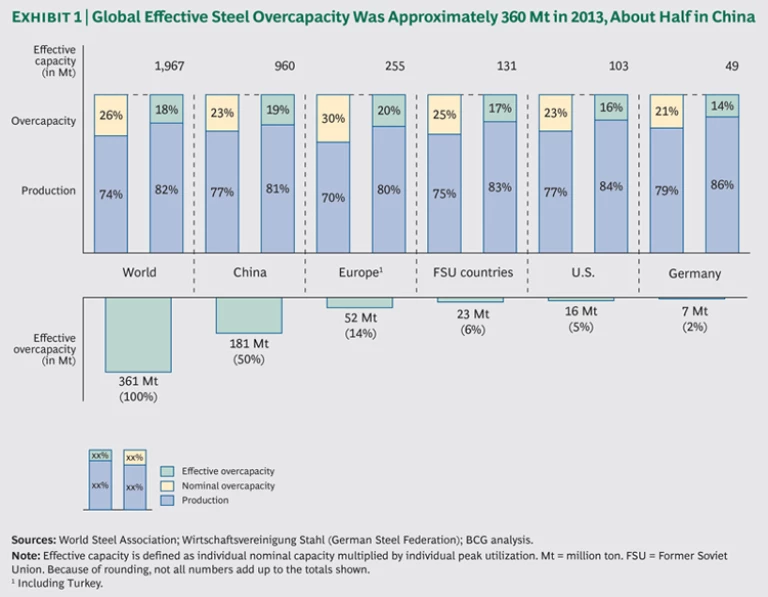

In order to discuss overcapacity, we first have to establish its extent. On the basis of our own computations, detailed in “Defining Capacity,” we argue that global effective overcapacity—that is, capacity proven available for production—was approximately 360 Mt in 2013. (See Exhibit 1.) This is a substantial amount, roughly equivalent to half of China’s current production or twice the European output. Yet it is less than some other published estimates, which range up to 500 Mt. We believe that estimates of 500 Mt overcapacity do not reflect reality because they are probably based on nameplate capacity numbers.

DEFINING CAPACITY

Estimates of industry overcapacity can vary widely because experts and analysts define the baseline in different ways. The crudest and simplest baseline is nameplate or nominal capacity. Most analysts, though, refer to “effective capacity” as a meaningful baseline for realistic overcapacity estimates. They take nominal capacity and deduct a standardized percentage to account for maintenance and other production downtimes.

BCG takes a more empirical view: we define effective capacity on the basis of proven, historically achieved peak-utilization levels during the last ten years, which include the China boom, assuming that capacity that was technically available and economically viable would clearly have been utilized during those peak years.

This enables the inclusion of another hard-to-measure factor that affects overall capacity and may even lead to operational capacity exceeding nameplate capacity: the “capacity creep” accumulated up to the last decade. Creep occurs in two ways: through short-term one-off measures such as putting hot briquetted iron into a blast furnace or through continuous improvement efforts that lead to small annual capacity increases.

We compute effective utilization as follows:

- We calculate peak regional utilization on an annual basis, representing maximum possible utilization as a percentage of nominal capacity during the 2000 through 2011 period.

- We then measure annual production against this maximum possible production.

An effective global overcapacity of about 360 Mt equates to 82 percent effective utilization, with considerable regional fluctuations. Chinese effective utilization rates, which had reached 100 percent at the beginning of the century, fell to about 81 percent by 2013. This equates to structural effective overcapacity of 181 Mt, or about half of the global total.

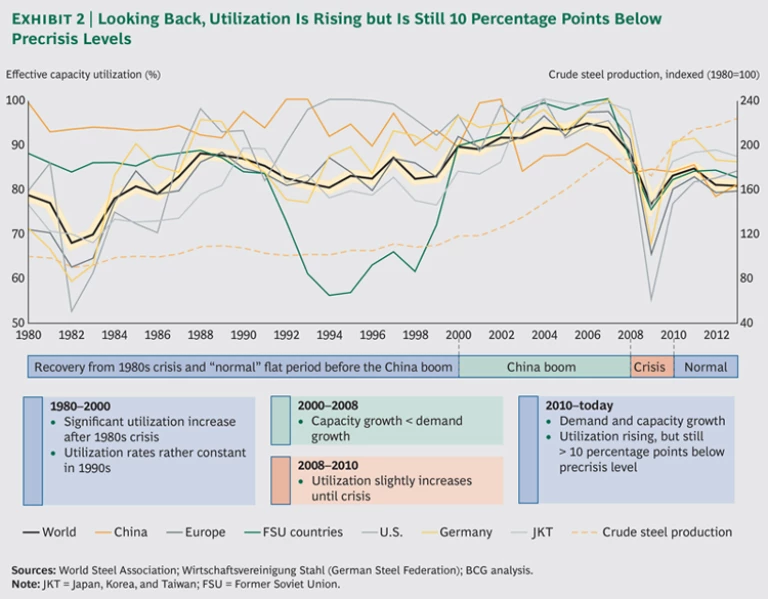

Utilization levels were flat during the late 1980s and 1990s. They rose during the China boom but fell back dramatically in 2008 and 2009. Production fell by slightly less than 8 percent at the same time that some 100 Mt of new capacity was introduced, most of it in China. This led to an 11.3 percentage point fall in utilization. (See Exhibit 2.) There has been some recovery, but utilization has not reached precrisis levels in any region as new capacity continued to come online. Furthermore, it is unlikely that precrisis utilization will be reached in the next few years. Steel companies have to accept that the exceptional circumstances of the China boom will not return in the foreseeable future.

Overcapacity is not unusual in capital-intensive industries. But steel’s technical and regulatory environment hampers short-term capacity adjustments (such as idling of blast furnaces) and increases long-term barriers to exit (such as legacy costs and environmental amelioration).

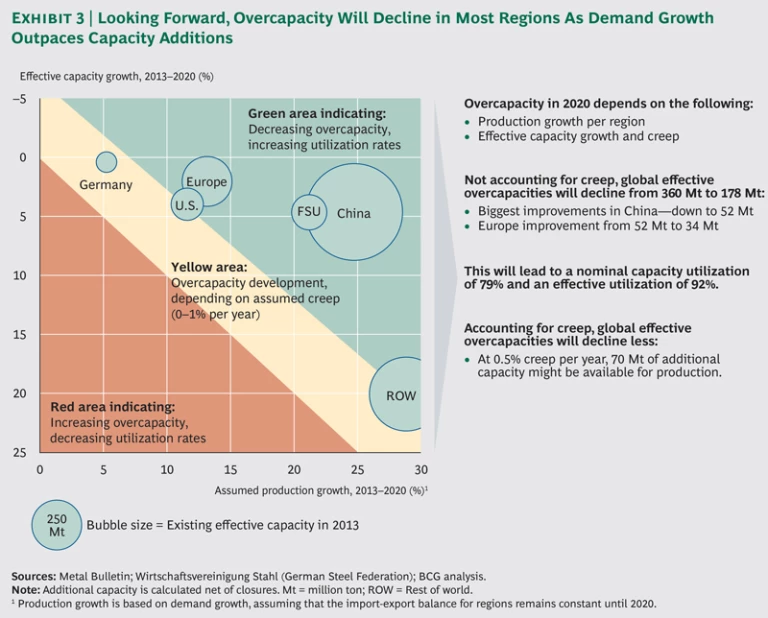

Although some overcapacity will be eliminated by growth in demand, the problem will remain. (See Exhibit 3.) On the basis of BCG’s long-term steel-demand model, we predict global overcapacity of 178 Mt in 2020—which is half of today’s levels but still approximately double the 90 Mt that was seen in 2007. In 2020, worldwide effective capacity utilization will be 92 percent, a nominal level of approximately 79 percent.

Overcapacity will ease most in China, where we predict a fall to about 50 Mt. This could, though, be complicated by a number of factors: if production grows more slowly than estimated or producers lack the concerted discipline to limit capacity growth (or both), Chinese overcapacities will be reduced by a lesser extent. A higher creep than 1 percent per year would be further detrimental. Obsolete capacity that does not show up in official calculations but could still produce steel could have an impact as well. If this extra capacity comes online again, net effective capacity growth is likely to be higher than the levels predicted in Exhibit 3, creating more overcapacity and depressing effective utilization rates.

Capacity creep could also change our projections. Creep of 0.5 percent per year on worldwide installed effective capacity would create 70 Mt of additional available production capacity by 2020.

So, overcapacity is here for years to come, with no collective solution in sight.

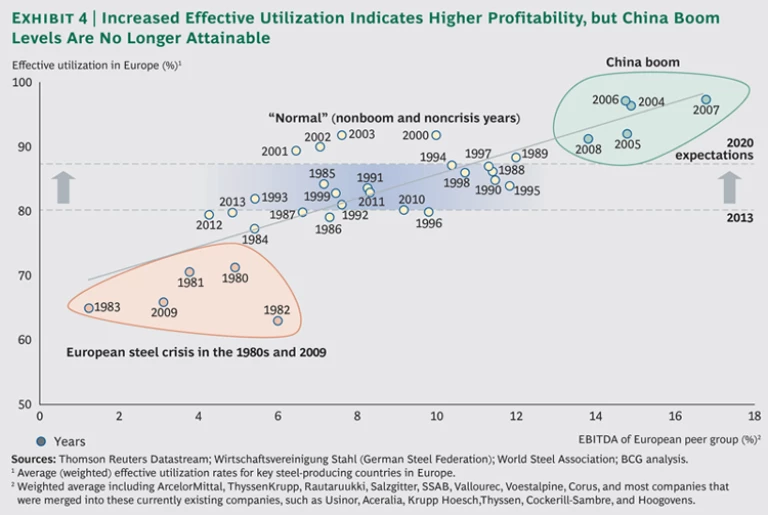

Our European peer-group study shows a clear inverse relation between overcapacity and profitability. (See Exhibit 4.) As of 2013, effective capacity utilization was close to the levels expected in “normal,” nonboom, noncrisis years, but European EBITDA is still at the low end. One could certainly blame this on the shift in the new materials pricing regime; however, we still believe there is room for improved profitability. This makes it imperative for the steel industry to help itself navigate through a difficult environment in a quest for better margins.

What Not to Do

There are still lessons to be learned from steel’s own history. In the 1970s and 1980s, governments devoted considerable spending and time to overcapacity crises in Europe and the U.S.

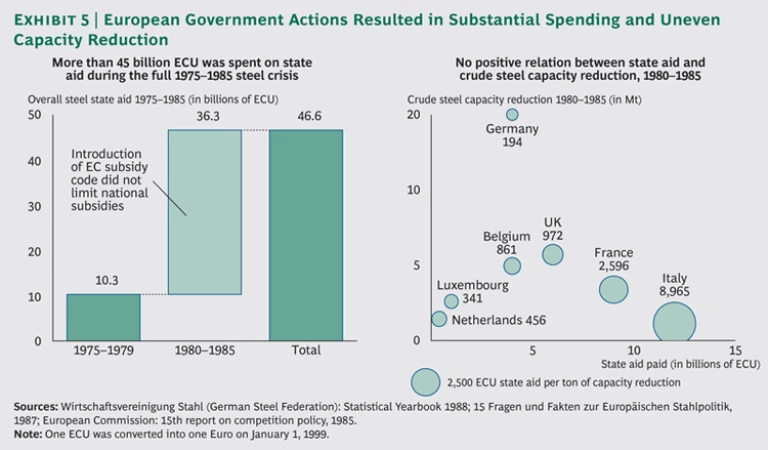

In Europe, applying active policy levers and paying various grants and subsidies—for example, operational, investment, closure, emergency, and R&D aid to the industry— cut crude steel capacity by 38 Mt from 1980 through 1985. (See Exhibit 5.) However, this capacity reduction came at a very high cost. More than 36 billion ECU was spent from 1980 through 1985, a cost of 940 ECU per ton of reduced capacity or 150,000 ECU for each full-time equivalent eliminated.

There was also a regional imbalance in subsidy payments and capacity reduction. Whereas some countries received relatively small subsidies and focused on industry restructuring, others received larger payments while spending it on measures that did not reduce capacity. Germany took out 19.8 Mt of crude steel capacity with only 3.8 billion ECU in subsidies, whereas Italy’s reduction of 1.3 Mt came at a cost of 12.0 billion ECU.

In the U.S., regulatory changes during the 1980s did long-term harm to the industry. A Department of Justice ban on mergers and acquisitions between viable companies left the supply landscape scattered, and trade barriers such as voluntary restraint agreements and trigger price mechanisms protected inefficient companies. They enabled struggling plants to continue, adding to overcapacity, as long as marginal revenues from extra production at least covered variable costs. Voluntary restraint agreements made steel more expensive. The U.S. International Trade Commission (USITC) has calculated that imported steel prices rose by 4.5 percent.

These increases fed into a loss of competitiveness by steel-consuming industries, whose exports fell by $1.7 billion from 1985 through 1988. At the same time, imports of steel-using products rose by $2.5 billion, a shift in trade patterns calculated by the USITC to have cost 15,000 jobs in steel-consuming industries. Other after-effects of voluntary restraint agreements included higher construction costs and increased prices in steel-intensive products such as cars and domestic appliances. The USITC calculates that consumers paid an extra $113,622 annually for every job saved in the steel industry in 1983.

These examples show that intervention by governments and regulatory bodies has rarely achieved its intended effect. The European case (taking into account the limited number of countries included in this sample) may even suggest that the stronger and costlier the intervention, the less the impact on overcapacity. Where benefits have been achieved from tariffs, quotas, trade barriers, and subsidies, they have at best been short-term, regional, and costly.

We do not intend to say that intervention can never be justified. It does make sense to lower exit barriers and so contribute indirectly to capacity reductions. Here, the likeliest measures are postclosure environmental grants and payments, but these must be contingent on permanent capacity elimination. Intervention can also be used to ensure fair competition—for instance, through antidumping measures—when market forces are incapable of doing so.

Nor do we see mergers and acquisitions as directly effective measures against overcapacity. It is sometimes claimed that M&A can remove overcapacity by closing inefficient facilities. This, though, happens only when there are real synergies between both companies that make the new company significantly more efficient and profitable than its predecessors—and if governments allow the new company to deliver these synergies. M&As that merely create a larger low-profit business could have a limited impact on profitability and overcapacity.

Also, modern integrated steel companies offer only limited scope for scale-based cost differences. Many smaller and less efficient plants have already been replaced, especially in Western Europe and Japan, leaving steel less scope than other industries for further economies of scale. Operating costs in steel usually relate to an optimum single plant size, often defined by the volume of the hot-strip mill. So, M&A is unlikely to achieve significant operating-cost savings.

According to synergy-reviewing reports, European steel mergers such as those that formed ThyssenKrupp, ArcelorMittal, and Corus created synergies at low single-digit percentages of sales. This is still substantial but lower than the rates achieved by other industries and industrial-goods sectors.

If neither intervention by government and regulators nor M&A will work to eliminate overcapacity and increase profits, other measures capable of creating sustainable advantage are needed. So management should make the most efficient use of their time by focusing on measures that help to cope with existing overcapacity.

Creating Value in Times of Overcapacity

The measures that we recommend for creating value have potential not merely to steer a company through the pitfalls of overcapacity but to enable its transformation into an advanced player and ultimately into an industry leader. This is not a simple or rapid process. Many companies rate as advanced players in parts of their value chain, but none operates at an advanced level across all areas or can yet be called an industry leader. Some measures draw on ideas from other industries that have experienced comparable difficulties, and some are steel-specific approaches designed to turn around companies.

Lessons from Other Industries

While no two industries are alike, other industries do offer useful lessons for steel companies. Our research identified three approaches that helped other industries deal with overcapacity.

The first approach, focusing on active reduction of overcapacity, comes from the shipping industry. Shipping’s situation after a long period of tight capacity was similar to steel’s. Shipping companies cut fuel costs, and collective capacity, by slightly reducing the speed of fleets. So what can steel learn from this? Operating models that achieve maximum efficiency (relating to energy efficiency, quality of output, or operational stability) rather than maximum capacity utilization can have the desirable side effect of limiting collective capacity. The best utilization rate for achieving maximum efficiency can be significantly lower than the optimum output points often considered to be the only real “bliss point” for steel operations.

The second approach considers two measures in line with market rules that make better use of capacity. An automobile industry example shows the joint use of upstream capacities, and an airline industry example focuses on shared capacities to serve a global client network:

- The automotive companies Toyota and PSA Peugeot Citroën jointly built a new plant in the Czech Republic, sharing both the €650 million investment and their expertise: Toyota was responsible for production; PSA, for purchasing. The plant produced the Toyota Aygo, the Peugeot 107, and the Citroën C1—vehicles that are 90 percent identical in structure. Steel companies could similarly share investments or create joint ventures. Examples already exist—for joint upstream production in Germany and for rolling in the U.S.—but they have had little impact in a landscape of individual optimization. This approach also contrasts with the way in which many companies are currently trying to differentiate themselves, by building up their own (advanced) high-strength steel capacity. The danger is that everyone will do this, creating fresh overcapacity with low margins.

- Airlines have introduced “code sharing,” in which two or more airlines share one plane to increase utilization and extend the network size. This concept could transfer to steel. A company based in one region could sell products under license for another player from a different region. This could increase the sales reach of the supplying company and widen the product portfolio of the selling company, without new capacity additions. Elements of this approach have already been used by European and Japanese companies. They agreed on a cross-licensing contract that enables each to sell the other’s products in its own home market.

The last approach offers a model for the high-priority commercial side of the business. The European label-stock industry (a segment of the paper industry) had significant overcapacity after a phase of heavy investments. One company fundamentally changed its commercial strategy to maintain market share by focusing strictly on target niches and avoiding commoditized markets, taking overcapacity out of selected market segments. This highly effective approach, which increased sales margins by more than 25 percent and EBITDA by 50 percent, could be applicable to some extent in the steel industry.

Steel-Specific Approaches

As well as these lessons from other industries, steel also needs to consider approaches specific to itself. Steel already has a broad and familiar repertoire of classic measures for operational excellence and continuous improvement. These include lean production approaches such as maintenance optimization to increase “up time,” improvements in energy efficiency, cost-cutting in direct functions, delayering in support functions, digitizing support functions, applying proper customer segmentation, and offering basic value-added services. Classic efficiency measures have an important part to play. They need, though, to be reinforced by more complex methods for optimizing full sections of the value chain, such as comprehensive optimization of customer value creation.

Any company wishing to attain advanced-player status also needs to adopt advanced versions of existing concepts that are capable of generating competitive advantage and designed to achieve total margin optimization. These aims are attained by making resources and input factors flexible and increasing the value of products or product portfolios.

Yet companies are still hampered by the industry’s flat cost curve, which reflects moderate differentiation and low long-term average profitability. This intense competition means that companies must improve continuously or find themselves at the wrong end of the cost curve.

In this environment, competitive advantage is hard to find. Many aimed, and still aim, to be the “Toyota” of the steel industry, creating significant advantages over competitors. But this is not easy. Toyota was years ahead of its industry in introducing lean production and operational excellence, which created a real competitive advantage.

Nor is lean production a one-off measure that can be implemented within two to three years. It takes a real change in corporate culture. Steel companies are starting from much the same level. Being faster can create an advantage, but to create a true competitive advantage steel players need to drive it as Toyota did. The cost-cutting and other improvements prevalent in the industry are musts for all companies, rather than a means to create higher margins or market share and decrease overcapacity and so can take companies no further than being industry followers.

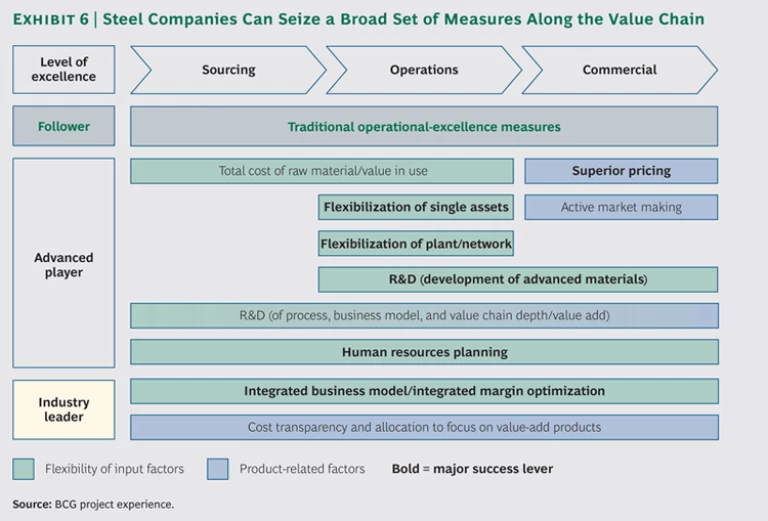

Given the limited potential of these classical measures, steel companies have to go further to create sustainable advantage over the competition. Most of the methods for achieving this are hybrids, combining the two goals of gaining flexibility in the use of input factors and increasing the value of products. There are many levers a company can use to become an advanced player in at least parts of the value chain. (See Exhibit 6.)

Any company that wishes to progress beyond the advanced-player level and become a market leader must accompany these measures with the introduction of an integrated business model and margin optimization. This means applying the flexibility creation measures across the entire value chain, with complete transparency on cost allocation and a clear focus on all measures targeted at increasing the value of the product.

Toward Industry Leadership

The principles of value chain flexibility, cost transparency, and value addition in products—the prerequisites for industry leadership—can be ingrained in the operations of a company through two sophisticated optimization concepts: price differentiation as a product-related measure and integrated margin optimization, which integrates business models and margins. Models of how companies adopting these concepts can operate are provided by two case studies illustrating BCG experience of their application.

Price Differentiation as a Product-Related Measure

The commercial side of business is extremely tough to change and improve, because overcapacity is the prime enemy of commercial optimization. Even so, it offers potential competitive advantages to forward-thinking companies. Systematic and strategic optimization of value creation and value capture is still in early stages in the steel industry, in spite of the vast amount of talent and resources that raw-material companies are investing in commercial excellence and value-creation-and-capture models such as value in use.

Steel companies also need a clear picture of where they operate. In practice, commercial excellence starts with a customer segmentation based on a product’s specific value contribution to the customer, including the value of both the material and the accompanying services. A deep understanding of steel’s value in use per customer and application is needed for a fair sharing of price, cost, and added value. Such a detailed understanding of the value that the same ton of steel can create in different customer industries, and for different clients and applications, enables targeted offerings (steel grade, material treatment, logistics, and services) that will be very differently priced.

Steel has unprecedented opportunities for using data to create such granular segmentation. New data-handling tools can move analysis from business warehouse level to a more granular and insightful enterprise-resource-planning level. This advance in segmentation will truly enhance commercial possibilities. BCG’s experience in the process industries shows that this approach results in a significant, sometimes counterintuitive reshaping of existing segments.

Big data–supported value-based pricing needs to be rigorously enforced through the sales organization. This should be reflected in improved management of the price waterfall that is anchored in day-to-day business to minimize price leakage. We recommend a high level of internal transparency on every element that builds up or reduces the realized price, such as bonuses and discounts. Application of such instruments should require approval at a high level to ensure that every reduction follows a clearly defined goal.

Integrated Margin Optimization

Companies need to change their current thinking and embrace recent changes in market practice if they are to develop into industry leaders, clearly differentiated from their competitors and with a competitive edge over them.

They need to respond to the combination of increasing price transparency, price volatility, and transactional liquidity that has forced companies into rethinking how they market their products and optimize their value chain. The best companies will see this shift in market behavior as an opportunity to differentiate themselves and to define a competitive advantage. Increasing transparency exposes previously invisible market inefficiencies, and the associated liquidity enables companies to act to offset those inefficiencies. This means identifying arbitrages across locations, qualities, and the value chain, such as transformation arbitrage between input and output.

Companies can create significant value, but only if they make a fundamental shift in their business. To introduce integrated margin optimization, they need to make two significant structural changes to their strategy:

- Change the value proposition: shifting the traditional mind-set of optimizing the company value chain toward optimizing the industry value chain

- Change organization design and associated governance: catering to the increased requirements of transparency along the full value chain, as well as the interactions and linkages between separate departments

Achieving these changes will end silo thinking, shifting from departmental P&L toward a P&L focus for the entire business.

Two new units are essential to changing steel companies. A centralized optimization department should enforce an integrated operating logic based on planning asset flexibility in close cooperation with all departments associated with the value chain. The unit’s initial task is to calculate the elements of an integrated P&L against market prices, enabling single departments to act in overall company interests. Its ability to react to the value chain should enable quicker responses to changing market conditions and prevent mispricing.

It should be joined by a risk management unit offering real-time analysis of the company’s risk position, for instance in relation to the net exposure of raw materials and sold products across the maturity of the contract, as well as providing transparency in financial exposure.

This level of integration will offer new opportunities across the whole value chain. It should eliminate silo-developed measures and go a step beyond existing concepts such as value in use by considering the entire value chain including sales, avoiding mistakes such as pricing steel of a certain quality without a full understanding of the company’s risk position.

Asked to calculate the effect of changing the operating mode of a blast furnace, the optimization unit would look beyond cost saving at individual process steps. It would also consider effects on the sourcing department such as the possible need to dispose of old raw materials and the impact on the commercial side of the business of filling production with low-quality products.

Case Study: A Flexible Model for Iron Making

An international steel company asked a BCG team how to cope with low plant utilization caused by structurally low and fluctuating demand, which led to low profitability.

We helped the client to significantly reduce the production costs per ton of steel and introduced a flexible production model. The key to reducing fixed costs was making blast furnace operations more flexible and reducing the number of furnaces on line. The new flexible operating model made it possible to adjust the iron-making capacity of each furnace. This was achieved by using hot briquetted iron (HBI) or pellets instead of ordinary burden or increasing the pulverized coal injection (PCI) and oxygen injection rates. The team then defined optimum operating points for the blast furnaces under different scenarios and assessed the financial impact for the client.

This enabled the client to adjust more quickly to fluctuating market conditions and to considerably reduce operating costs. Measures included “mothballing” blast furnaces and adjusting their operating rates to market demand. The operating rates of the coke ovens and the number of sinter plant strands were adjusted accordingly. This resulted in fixed cost savings of 10 to 15 percent. Raw-material savings of 2 to 3 percent were achieved through adjustments in the burden, a cheaper raw-material sourcing mix, and optimal use of low-cost coals. Similar results were achieved by applying this flexible model to rolling mill operations.

Case Study: Establishing the Optimal R&D Organization

R&D matters. Every survey of top executives confirms this. Some 25 percent see it as their company’s top priority, and a further 50 percent rate it among the top three priorities. Coming out of the crisis, companies are spending more on R&D. A BCG study in 2013 found that some 20 percent planned a significant increase compared with the previous year, and another 50 percent planned at least a slight increase.

Yet senior managers also see real difficulty in converting R&D spending into top- or bottom-line impact. The three obstacles most cited are long development lead times, selection of the right ideas, and lack of coordination. This reflects what we see at our clients. Companies with large, expanding R&D project portfolios often fail to measure payoff or operate a meaningful stage-gate process.

Innovation can help secure margins and differentiate your company, neither of which is easy in the low-margin, commodity-product-dominated steel industry. A well-structured R&D organization, with well-defined processes—especially clear budget allocation for the research and development sides—and governance structures, can be a key factor for differentiation and R&D budget efficiency. It needs to master the trade-off between basic research, funding ideas for longer-term success and developing new products or product generations for existing and new customers. Too often, we see an ineffective combination of ivory-tower research with pure, largely incremental, product development.

Successful innovation depends on funding ideas that will not necessarily generate EBIT impact in one year but will secure long-term innovation strength. Projects should be funded on the development side both for current profit pools (new generations of existing products or upgrades) and future profit pools (new products for existing or new clients). A “fast track” fund should be introduced to support small investments without going through the entire R&D project-application process.

BCG clients have been able to cut R&D budgets by 15 percent, without jeopardizing their R&D strength. Strong stage-gate processes have eliminated projects that were not beneficial but had continued to receive allocations. A competition for R&D funding has ensured that the best ideas were backed, and money was reserved for out-of-the-box ideas with no immediate impact but long-term potential. Most important of all has been cultural change: accepting that success in innovation comes only at the cost of some failures.

While this paper offers a fresh way of looking at current and future overcapacity, steel CEOs and leadership teams will find there are few easy answers to the problem. The coming years will be defined by the daunting task of value creation in a phase of overcapacity.

Steel companies will need to adapt as the business becomes more sophisticated and complex. This will demand more talent, greater technical competence, and more-sophisticated operating models. These requirements are likely to lead to a shakeout separating companies that do little from those that break out of the overcapacity dilemma through operational excellence, true commercial excellence, and the first steps toward integrated margin optimization. Those that do little will struggle, but there will be huge benefits for ambitious companies, which will prosper by being more progressive than their competitors.