Global insurance companies face tough competition, weak markets, sluggish growth, and low returns. Yet most insurers are not fully tapping a golden opportunity to build a larger and more lucrative business. It involves customers that many carriers already serve but rarely interact with and revenues obscured by the cash from larger lines of business.

In a detailed global study, The Boston Consulting Group identified the untapped opportunity that lies in serving the growing commercial-insurance needs of small and medium-size enterprises (SMEs). BCG’s research included an extensive survey of 2,500 small businesses in six of the largest developed SME insurance markets—the U.S., the UK, Italy, France, Germany, and Japan—and focus group interviews that explored the insurance decision-making processes of small business owners. The results are a detailed and surprisingly different understanding of small-business insurance needs, preferences, and behaviors, as well as strategies that can enhance insurers’ profits.

SMEs are a growing force in the global economy, yet they remain an afterthought to many large insurers, which generally perceive SMEs as a scattered market of small customers, best handled at arm’s length through intermediary agents and brokers. In most markets, SMEs account for almost a third of the value of all commercial-insurance premiums—in a global market whose estimated value is nearly $1 trillion in annual premiums, including captives and reinsurance.

SMEs, for their part, have shown little interest in dealing directly with commercial carriers. They have preferred having broker and agent intermediaries help them navigate the complex market and choose appropriate coverage from the multitude of commercial-insurance offerings. In addition to property and casualty coverage, offerings include auto, transportation, liability, workers’ compensation, and malpractice insurance.

BCG found, however, that SMEs are more open to direct interaction and outreach from insurers than many carriers have expected. So in addition to using the traditional agent channel, carriers have the opportunity to find other ways to interact with SME customers. Our research results and work with insurers have helped us identify four approaches that astute and proactive carriers can pursue—individually or in combination as a multichannel approach—to build a larger and more profitable SME commercial-insurance business:

- Design targeted outreach initiatives that don’t threaten existing intermediaries but build a true multichannel interaction model with SMEs.

- Improve the value proposition for brokers and agents.

- Develop a “hybrid direct” model that provides semicustomized offerings, advice, and information.

- Develop new data capabilities and targeted analytics to maximize customer value.

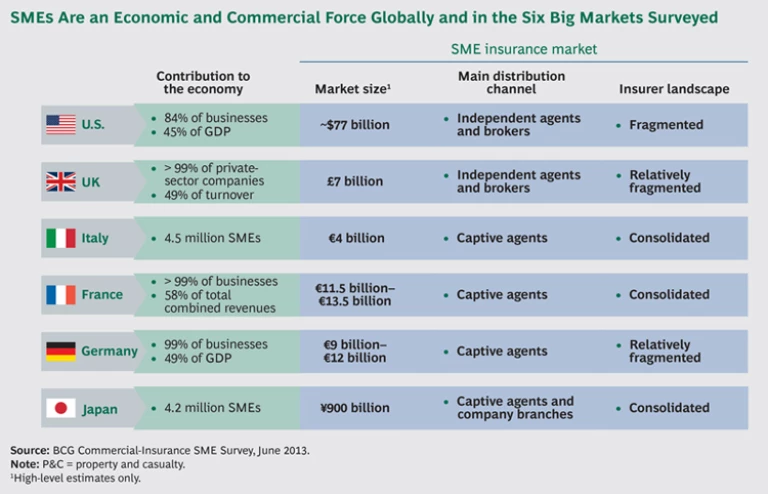

The Power of Small Companies in Six Big Markets

In addition to the survey of developed markets, our research was informed by in-depth SME interviews in the U.S. and input from carriers incorporated through an insurer advisory committee. The survey polled businesses with up to 250 employees, a widely used benchmark for defining SMEs. There is, however, no universally accepted SME definition, and criteria differ across markets, industries, and organizations. Country-reported SME data, for example, can reflect benchmarks that are based on company revenues, balance sheet totals, or employee head count.

By any definition, SMEs are a major economic force globally and in most developed markets. (See the exhibit below.) In the U.S., they account for 84 percent of limited-liability businesses and 45 percent of GDP. In the UK, France, and Germany, they make up some 99 percent of private-sector businesses.

That collective commercial heft is a critical opportunity for insurers competing in a global market that will likely remain challenging for the next decade. (See “ Improve P&C Profitability and Premium Growth ,” BCG article, January 2014.) Nonlife insurers are confronting sluggish growth in developed markets, price-sensitive customers, squeezed margins, and low return on equity. Capital surpluses have kept competition high, while a spate of recent catastrophic events has elevated loss ratios. Expanding business to rapidly developing economies (RDEs) has provided faster growth for some insurers—from a small revenue base and, in many cases, with high and costly barriers to entry.

On the basis of distribution, developed SME insurance markets fall into two distinct market archetypes:

- Independent-agent markets, notably the U.S. and the UK, where independent agents not directly owned by the insurer constitute the primary distribution channel

- Captive-agent markets, where the primary distribution channel comprises mostly captive agents or company branches, including Germany, France, Italy, and Japan

The archetypes, along with our research, provide insights and competitive guidance for SME insurers operating in the six markets surveyed and in developed markets worldwide. (For detailed data on each of the six major markets, see the Appendix .) The archetypes and their characteristics don’t necessarily apply to SME markets in emerging economies, which were not the subject of our research.

The Leading Needs and Preferences of SMEs

BCG’s survey revealed four important SME needs and preferences that can contribute directly to building a larger commercial-insurance business.

SMEs want more interaction with insurers. While SMEs were mostly satisfied with their broker and agent relationships, they also wanted more direct interaction with carriers. That included greater insurer involvement in the purchase process and more information and education from insurers on coverage and insurance benchmarks related to their industries.

Closer and more interactive relations with SME customers can shave costs, broaden the client base, and create new opportunities for customer engagement. Many SMEs rely heavily on their brokers and agents, interacting exclusively with them throughout the policy life cycle. In the UK and the U.S., 35 percent and 14 percent of SMEs, respectively, reported that they did not know who their insurer was, or they listed their agent or broker as their carrier. SMEs in general expressed satisfaction with that relationship but indicated that they would like more proactive engagement from their carriers.

Price and consumerism often play limited roles when SMEs choose or switch insurers. SMEs apply little consumerism to their commercial-insurance purchase decisions. Rather than spend time “price shopping,” most said that they think about insurance only at renewal time or when filing a claim.

Price—while important—is not the deciding factor in many markets. Small business owners often start by looking for a lower-price option. Yet they freequently switch carriers to receive better coverage or meet a specific need rather than to get a lower price. Carriers that anticipate a full array of SME needs and are proactive—for example, contacting an SME with a relevant offer before renewal time—will gain the advantage, capturing market share with better retention and new business.

SMEs place greater trust and loyalty in incumbent insurers with captive agents. The inclination of SMEs to buy commercial insurance from their personal carrier is greater in markets—such as Italy and France and, to some extent, Germany and Japan—that have a strong presence of captive agents, the survey found.

That trust and loyalty gives carriers with strong captive-agent networks a substantial hidden advantage, particularly in cross-selling. They are better positioned to develop a more compelling offering than are carriers with a strong broker channel. In short, trust in the incumbent insurer is a significant advantage, the survey showed, and captive agents tend to win greater trust from SMEs.

SMEs in these developed markets are reluctant to depend on banks as intermediaries. Because they have depended on other intermediaries in the insurance-buying process, SMEs in developed markets, do not perceive banks as adequate advisors or intermediaries, nor do they believe that banks have sufficient expertise in insurance. That perception clearly reduces the ability of banks to intervene as fee-receiving intermediaries in those markets, which, in turn, increases the opportunity for insurers to interact directly with SMEs.

Also, in emerging markets, bancassurance can be a viable option, particularly where insurance products have not penetrated widely and there are few established intermediaries.

Four Approaches to Serving SMEs More Directly

Commercial insurers might well be tempted to “go direct” to the SME market, given the openness of SMEs in our survey to more outreach from carriers. In many markets, however, direct distribution is likely neither to offer insurers a fast track to growth nor to become a dominant model anytime soon. (See “Going Direct: A Path for the Future?”)

Going Direct: A Path for the Future?

Commercial insurers might well be tempted to “go direct” to the SME market. Eliminating the middleman, a direct-sales approach offers multiple benefits. It can shave commission costs by 10 to 15 percent while reducing process complexity, broadening the customer base, and creating fresh opportunities for client engagement. Direct distribution can also significantly improve customer response times, sometimes reducing a service process from a full week to a single day.

Going direct, however, isn’t likely to offer most insurers a fast track to growth in most markets. Direct-sales penetration to SMEs—while varying widely among the six developed markets we studied—was relatively low overall. Direct sales reached a maximum of just 18 percent of SMEs in the UK market and totaled just 4 percent in the U.S. (See the exhibit below.)

Prospects for going direct differ widely among markets—even among those that share the same market archetype. The U.S. and UK, for example, are both independent-agent markets.

A majority of SMEs in some markets—including the U.S. and France—said that they were unwilling to buy direct, in most cases because they need purchase advice. Most small-business owners consider commercial-insurance offerings extremely complex and difficult to understand. That finding alone shows how much work most carriers face before they can take advantage of the longer-term potential of going direct. They will need to simplify product offerings, become proficient at providing customized counsel, and improve brand awareness.

Going direct will require changing current direct-to-customer sales models. Although small commercial-auto policies, for instance, are similar to standard personal-auto policies and include many of the same prepackaged coverage options, SME customers face more complex requirements, and many require assistance in selecting appropriate coverage levels. For carriers, that will mean taking on dedicated advisors or finding new ways to deliver advice effectively and efficiently.

Furthermore, to avoid channel conflicts, many carriers will need to sell under brands different from their core brand in markets where they already have agent distribution.

Still, insurers such as Hiscox, Insurantz.com, and Premierline Direct in Europe, and Geico in the U.S. are testing the waters. We anticipate that others will follow and that the direct-commercial SME market could reach $25 billion by 2022.

Insurers should, however, consider four other approaches that proactively address SME needs and preferences. Each approach can help build a larger and more profitable business while taking advantage of competitive, economic, and regulatory conditions in specific markets. Most of these initiatives can be launched without incurring substantial costs or overhauling a carrier’s business model.

Design targeted outreach initiatives that don’t threaten existing intermediaries. Insurers can explore targeted outreach initiatives that add value and build business through proactive interaction and initiatives. But carriers should do so in a way that doesn’t threaten existing intermediaries that are crucial to their business.

Initially, an insurer can maximize its value to an SME by providing education on insurance best practices and benchmark information relevant to the SME’s industry. More ambitious initiatives might include “good behavior” programs and benefits similar to those offered in personal-insurance lines.

Strategically, insurers should develop operating models that are better targeted to serve explicit small-business needs. By tightly integrating the model with distribution channels, insurers can provide differentiated service, including more tailored and proactive communications, better integration with the agent or broker, and quicker servicing of policies.

Improve your value proposition to brokers and agents. Given their relations with and influence over small business owners in most markets, brokers and agents provide a crucial, prepaved path to building your business. That makes it important to give brokers and agents, in addition to the customers, a keen sense of your value.

One means of achieving this is to provide data and analytics on SME behavior that help intermediaries grow their book. Insurers can also provide modularized products designed to help intermediaries pitch to specific acquisition targets. Another way is to help intermediaries build multichannel servicing capabilities—for example, online pricing and self-service platforms for clients. These provide the added benefit of integrating insurers’ operating models more tightly with intermediaries.

Insurer relationships with brokers and agents tend to be highly concentrated—typically about 80 percent of premiums are driven by 20 percent of brokers and agents. For this reason, insurers should evaluate and segment their intermediaries according to business-building potential and target their strongest efforts on the highest-value intermediaries with a differentiated partnership model.

Develop a hybrid-direct model with semicustomized advice and information. Although going completely direct isn’t an immediately viable game changer for many carriers, most can take a portion of their SME business direct. A hybrid, or personalized, direct model—with semicustomized offerings, advice, and information—can produce some of the same client-centric benefits. This model has the potential to increase SME penetration and profit immediately. To succeed, the hybrid-direct program should aim to give SMEs the kind of personalized interaction they are accustomed to experiencing with an agent or broker.

A hybrid-direct offering coexists with an insurer’s agent and broker channels without undermining them—avoiding channel conflict, for example, by establishing a new brand not associated with the core business. The hybrid offering provides products and coverage in tandem with—but different from—the insurer’s traditional products distributed by agents. A hybrid-direct initiative might include services and products tiered by customer segment, with related pricing options.

The hybrid-direct approach provides personalized interaction and advice through a semicustomized service that is consistent with the carrier’s business model and resources. This might include assigning SMEs dedicated agents who work and communicate from a central location rather than interacting directly with clients in the field. An SME would know its dedicated agent by name and communicate directly by phone or e-mail, rarely, if ever, seeing him or her.

Develop data capabilities and targeted analytics to maximize customer value and improve underwriting. By combining in-house data with customer data from new sources—such as company databases and credit-scoring providers—insurers can create a multitude of business opportunities. Many of them derive from customer segmentation—using data and analytics to identify SMEs that share specific needs, preferences, or product attributes such as maturity dates—then developing targeted products and services customized to those segments.

Similar opportunities can be created by exploring customer lifetime value and tailoring products to maximize that value. This approach may be preferable to pricing discounts, which might not be financially viable, or active cross-selling, which the customer might resent. Another set of initiatives involves simplifying and shortening underwriting cycles by using information available from company databases and credit-scoring sources.

Developing advanced analytics on the basis of new or existing data allows carriers to optimize value propositions for specific demographic segments in, for example, the following ways:

- Helping target women and minorities who are now more commonly the founders and owners of small businesses, particularly in the U.S.

- Identifying potential new SME customers within the existing customer base of the carrier’s personal-insurance lines, then developing targeted marketing programs to reach them—a strategy that has been used very effectively by credit card companies

Carriers might also tap industry-specific data and knowledge to provide risk mitigation advice and tools as part of their service offering to SMEs, which have limited resources to create sophisticated tools of their own. One carrier, for example, provided fleet-monitoring programs to SME clients and, in three years, reduced its loss ratio by 10 percent while increasing customer retention by more than 15 percent.

In an era of tight margins and weak returns for commercial insurers, small businesses offer a substantial and rewarding growth market. But tapping that growth will require developing more direct and customer-centric approaches that serve SMEs both collectively and individually.

Success means understanding the collective needs and preferences of SMEs clearly. At the same time, it requires approaching individual clients more directly and offering services that satisfy individual needs in a more customized fashion—with less complexity. Carriers that succeed will be those capable of rethinking the market, the SME customer, and perhaps even their own business model.

For astute insurers that step up to the challenge, adopting one or more of the approaches discussed above can unlock the golden opportunity at their doorstep.