In today’s climate of volatility and global disruption, business leaders who prioritize procurement can achieve significant competitive advantage. Our procurement consulting experts help clients establish efficient operating models—powered by AI and analytics—to beat inflation, meet sustainability standards, strengthen supply chain resilience, and more.

With hundreds of procurement projects completed across industries and geographies over the past five years, BCG’s procurement consulting team—named a worldwide leader in operations improvement consulting services by IDC MarketScape—helps companies chart a course to buying differently and in a better way. They blend deep sector-specific knowledge with expertise in both traditional and new procurement best practices, as well as digital transformation.

BCG’s Approach to Sourcing and Procurement

Building relationships remains important to sourcing and procurement, but personal experience must be balanced with a rules-based process that uses digitization—such as AI-powered and analytical solutions—to speed up outcomes and reduce costs. Creating value requires enablers and a strong data foundation. To implement an effective digital procurement strategy and take full advantage of the opportunities that digital offers, BCG helps sourcing and procurement leaders define the core value that their function brings to the organization.

To identify the investments needed to create value, through increased savings, quality, speed, innovation, sustainability, and risk mitigation, we examine your organization’s strategic priorities and assess its digital maturity, including opportunities to unlock approaches that combine AI, technology, and human capabilities.

Using our extensive library of client use cases to speed our work—and tapping into the complementary capabilities of INVERTO, a BCG specialty business that focuses on procurement and supply chain management—we then select and run use cases that match your specific needs. The results help pinpoint technology interdependencies and anticipated pain points, which in turn helps shape your custom digital roadmap. To turn that roadmap into reality, we work with BCG X to develop and deploy user-centric digital solutions, address users’ needs, and help generate value.

Procurement has become a strategic lever for performance and business resilience as global volatility continues to expose structural vulnerabilities in supply chains. Heightened geopolitical risks, supply shocks, and regulatory shifts have made resilience a core competitive advantage, even if it leads to extra costs.

Our offering, enabled by AI-based tools such as Inflation Control Tower and Supplier Risk Monitor, helps provide transparency, predict and mitigate supply risks and prevent supply shortages, analyze inflation impact on product costs, and adjust end-product pricing.

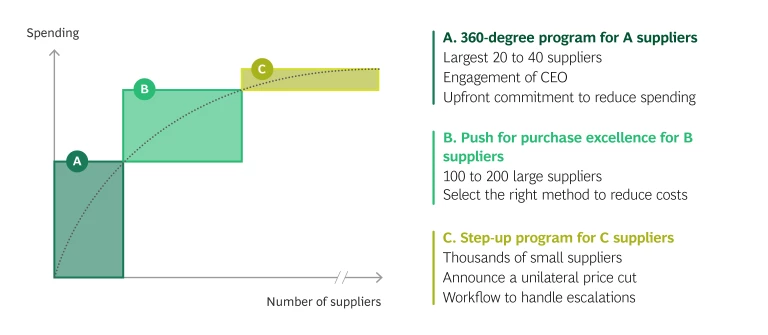

The New Pareto: Focusing on Suppliers Instead of Categories

To deliver value through savings, CPOs in all industries need to cut procurement expenditure substantially and quickly, but the conventional approach of focusing on reductions in category spending is too slow and often insufficient to generate competitive advantage. A more effective approach leverages both supplier relationships and technology and is tailored to each of the following major vendor segments:

A Suppliers. Our innovative 360° Program for A Suppliers engages the most senior levels, including the C-suite, to get the right decisions in place. The ambition is bold: to double the savings in a partnership mode.

B Suppliers. We push for procurement excellence, an approach that focuses on using the right commercial and technical levers, backed by the right preparation, to cut costs. BCG’s AI Negotiation Coach tool helps make this a reality, suggesting to the buyer the right go-to-market approach and analysis. Over time, the coach—an algorithm—learns from the outcomes and becomes increasingly strategic and effective.

C Suppliers. Our step-up-to-contribute program harnesses potential savings from the smaller vendors (which tend to fly under the radar) by increasing their visibility and making them contributing partners. Our AI Tail Cutter tool generates an appropriate savings target and steers the communication with an individualized approach.

Inverto, an international procurement and supply chain consulting company acquired by BCG in 2017, complements BCG's procurement approach with its strong focus on implementation to achieve fast and tangible impact, deep category knowledge from thousands of client projects, and numerous category benchmarks for maximum impact.

Savings. For a German bank looking to achieve near- and long-term savings in procurement spending, we used commercial and technical levers yielding an immediate 12% savings. By optimizing the target operating model, we developed 20 additional initiatives in governance, procurement mandate, savings tracking, and other areas.

Operating Model Redesign. For a large energy player, we conducted a full procurement optimization program that included the design of a new, center-led operating model. The work covered key processes and a capability-building program for teams, generating savings of 10% of addressable spending.

Sustainability. Our strategy for CO2 reduction at a European automotive OEM emphasized procurement practices, focusing on Scope 3 emissions under the Paris Agreement as the basis for new CO2 targets. We then outlined the required measures—including timing and cost—and laid out intermediate and long-term milestones.

Digital Transformation. We partnered with an international oil and gas company in Asia to create a roadmap for its digital procurement transformation. After completing our digital maturity review, we identified 11 use cases across strategic and operational procurement, prioritized efforts, and produced a detailed schedule for year-one digital implementations.

BMW Group is partnering with BCG to optimize efficiency and innovate workflows with GenAI leveraging Auto AI by BCG X. The solution was developed in collaboration with BCG X, AWS, and BCG Platinion. The streamlined approach to day-to-day operations is creating exciting new opportunities for growth.

To view this video content, you must consent to all cookies

Video

BMW Group's Transformation: Turning GenAI Concepts into Scalable Success

BMW has launched a major transformation initiative, leveraging GenAI to streamline procurement tasks, rethink processes, and improve supplier interactions. As an extension of our existing partnership around AI, BCG and BMW are now partnering with AWS, BCG X, and BCG Platinion to ensure a secure, scalable integration of GenAI.

How BCG streamlined the organization and strengthened the cost competitiveness of a top consumer durables manufacturer.

Change Management Is Inherent to Our Procurement Approach

Change management is critical to ensuring that procurement becomes a source of competitive advantage. It is integral to almost all of our procurement projects. To ensure that results are swift and sustainable, we work side by side with your teams so that they are clear on what procurement achieves in savings, sustainability, and competitive advantage. We are here to answer questions, integrate team-specific needs, and overcome pain points.

How BCG Works with Organizations to Reach Sustainability Milestones

Suppliers must comply with comprehensive environmental, social, and governance (ESG) legislation and directives. But meeting requirements isn’t enough. Leading companies across industries are already pushing beyond mere compliance, and are working to CO2-positive supply chains and socially responsible procurement. To deliver value through sustainable operations, our procurement consulting team supports companies in:

Translating company targets into supplier targets

Defining relevant measures

Building the abatement curve with a clear business case mindset

Setting up relevant measurement systems

Integrating sustainability into procurement’s target operating model and KPI set

Upskilling procurement teams and suppliers to accelerate Scope 3 decarbonization efforts through our Supply Chain Net Zero Academy

In today’s volatile environment, the benefits of a strategic approach to procurement are greater than ever.

To view this video content, you must consent to all cookies

Video

August 25, 2025

Elevating Procurement to the Leadership Table | BCG EDGE 2025

More than half of a company’s costs are external. Procurement has become essential to managing volatility and safeguarding margins in a shifting environment.

Procurement is poised to capitalize on AI, which can streamline manual work in key processes by up to 30% and reduce overall costs by roughly 15% to 45%.