Transforming from a telco to a techco required a deep commitment to inspiring engagement throughout the company. EVP and Chief Revenue Officer Ashley Haynes-Gaspar discusses partnering with BCG to navigate this change and the extraordinary results Lumen has already seen.

Although many business transformations deliver short-term impact, 75% fail to deliver long-term, fundamental change. Successful company transformations are marked by three critical outcomes:

- Sustainable value creation: Gains are sustained post-transformation, with a focus on continuous value delivery.

- Step changes in capabilities: The organization is fully equipped to deliver changes and drive continuous improvement.

- Sustained culture shift: The culture ensures that the organization is aligned and engaged in new ways of working.

These companies are three times more likely to outperform average short- and long-term total shareholder return for their sector. The 50 largest transformations that BCG worked on over a recent five-year period have delivered 15% higher TSR for those companies compared to relevant stock indices.

Our Business Transformation Services

We partner with our clients to accelerate performance and drive value creation, using a proven methodology tailored for business transformation.

A performance and value acceleration transformation yields more impactful results than a traditional approach.

BCG's special situations team delivers turnaround and restructuring consulting services to clients facing profitability and liquidity crises.

BCG’s cost advantage approach resets costs within a framework that is customized, precise, and thorough.

Tech-Led Business Transformation

We help clients leverage the right technology, digital, or AI solutions to enhance capabilities, boost efficiency, drive innovation, and improve CX.

Related Services

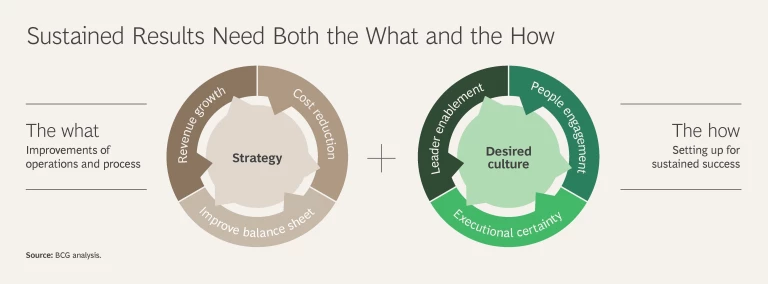

We partner with clients to deploy an industry-leading proprietary methodology that ensures a relentless focus on value. Our methodology is based on deep experience, which has shown that to create sustained results, programs must address the what and the how of strategic transformation.

The what focuses on making the right improvements in operations and processes, including:

- A holistic strategy to uplift end-to-end business performance, supported by a transformative approach covering the entire business.

- Revenue growth driven by actions such as pricing optimization and salesforce activation and effectiveness, all tied to metrics and KPIs.

- Cost reduction realized through cost excellence, organizational simplicity, capital efficiency, and other measures, also tied to metrics and KPIs.

- An improved balance sheet from optimizing working capital and liquidity management.

The how sets up a company for sustained success through:

- Executional certainty. All change efforts are coordinated through a transformation office and backed by financial tracking, a defined transformation structure, and rigorous processes and tools to embed and reinforce change.

- Leader enablement. Leaders agree on what needs to change. They’re motivated to deliver on objectives, accountable for results, and lead by surrounding themselves with teams of champions.

- People engagement. People feel seen and supported, and they understand what is happening and why. They are energized by the vision, motivated and enabled to contribute, and upskilled to support their growth.

- Desired culture. The culture is aligned to the transformation vision, and leaders role-model target behaviors. Teams exhibit these same behaviors, which are embedded throughout the organization’s structures, processes, and policies.

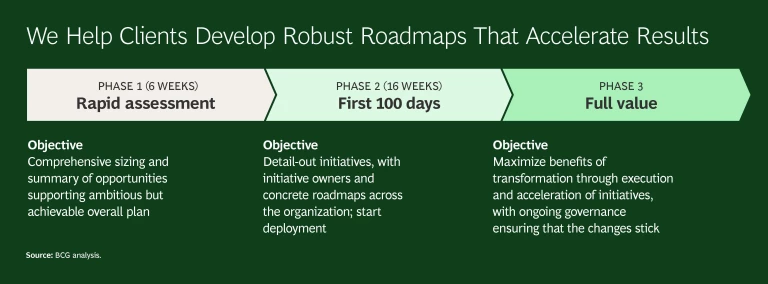

Our business transformation consultants work closely with clients to drive strategic impact quickly, so an organization is engaged and able to make the impact stick.

How We Work with Clients

- Partner with clients: We operate in full partnership with leadership teams, sharing the agenda, incentives, and risks.

- Work shoulder to shoulder: We work together with client teams day-to-day to ensure they are fully engaged, enabled, and upskilled.

- Seasoned operators: Our dedicated team of experts has deep experience along both the what and the how of transformation.

- Rigorous methodology: Our holistic methodology focuses on strategy, cost, the top line, and balance sheet improvements.

- Bring the best of BCG: We have an obsessive focus on value and utilize the best of BCG's industry, sector, and functional expertise.

- Make change stick: Our industry-leading approach ensures that improvements stick by mobilizing and enabling organizations and addressing culture.

Our Clients’ Success in Business Transformation

We have supported thousands of large-scale business transformation programs for enterprises in a diverse array of industries around the globe. Our clients achieve measurable results, including increased revenue, reduced costs, and accelerated performance.

Video

April 22, 2025

Video

March 24, 2025

KONE Democratizing Digital

Urbanization is accelerating, and KONE moves 2 billion people daily. True transformation isn’t just about tech but about people. With BCG’s support, KONE is proving that the right mix of tech, data, and human impact can reshape an entire industry.

Video

February 13, 2025

How does a thriving engineering firm accelerate performance while doubling its investments in digitization and innovation? COWI Group CEO Jens Højgaard Christoffersen talks to BCG's Christin Owings about the successful transformation of COWI.

Video

September 16, 2024

BCG helped Teknosa, Turkey's leading electronics retailer, implement an accelerated holistic transformation and get on a profitable growth path using a combination of cost discipline, bold strategic moves, and technological innovation.

Video

March 27, 2023

How Heineken Europe Is Transforming Its Supply Chain

The brewer launched a supply chain business transformation program to reduce complexity, build new ways of working, and reduce its carbon footprint. Here’s how it succeeded.

Video

October 29, 2021

Turning Around a Global Jewelry Giant

BCG worked shoulder-to-shoulder with leading jewelry company Pandora to launch a transformation program that reignited passion for the brand and helped Pandora get closer than ever to its customers.

Our Business Transformation Solutions

We deploy a number of proprietary tools to ensure that the how of a transformation strategy is set up for success, including:

KEY Impact Management by BCG X

KEY Impact Management is a one-stop-shop for program management, managing complexity on every phase of a transformation.

KEY Impact Management by BCG X

Solution

Solution

BCG U Transformation Academy

Our experts design outcome-focused, tailored, and scalable upskilling solutions to build capabilities and drive transformation success.

BCG U Transformation Academy

Solution

Solution

Leadership Coaching

Our coaches—former C-suite execs with transformation expertise—help leaders shift mindsets and behaviors for successful transformations.

Leadership Coaching

Tool

Tool

OrgVantage

Our tool assesses effectiveness and uncovers organizational advantages that boost performance, engagement and support transformations.

OrgVantage

Explore Our Insights on Business Transformation

Article

May 8, 2025

Companies strive for growth, but costs often outpace it. To avoid this trap, transformations need a dual mandate of reducing costs and increasing revenue.

Article

April 16, 2025

Unlikely as it seems, businesses can not only thrive amid economic uncertainty—they can seize the opportunity to transform for sustained growth.

Explore More

Capability