This is the first chapter of a four-part annual report on the global wealth industry and the trends shaping its future. The full 2026 Global Wealth Report: The Great Reordering is available as a PDF download.

Against a backdrop of trade wars, tariff brinkmanship, and escalating geopolitical tension, global financial wealth rose 10.7% to $333 trillion in 2025, up 2 percentage points over the prior year—the highest rate of growth since 2021. (See Exhibit 1.) Including real assets, net wealth reached $550 trillion, up 9.3%.

The gains were not evenly distributed. Equities surged 13.2% while real assets expanded 7.4%, pinched by high prices and rising supply in major developed markets. Gold was the standout, rising roughly 44%, driven by robust retail buying and a wave of central bank accumulation that reflects deepening unease about reserve currency stability.

Financial wealth is projected to grow at a 7% compound annual rate through 2030, though the pace of gains assumes an easing of geopolitical tensions and energy disruptions in the second half of 2026.

Where Wealth Is Scaling

Global financial wealth is expanding, but 2025 revealed a widening divide between regions generating wealth at scale through deep capital markets and those held back by policy uncertainty or weak economic fundamentals.

Asia-Pacific remained a key engine of growth, supported by its central role in the AI supply chain, from semiconductor exports in South Korea to accelerating data center investment across Southeast Asia, and strong equity market performance in Hong Kong and Japan. Mainland China led the region, with financial wealth expanding by 15% in 2025 and projected to grow at 9% annually through 2030. The rest of Asia-Pacific grew by 9.2%, with 7% annual growth expected over the same period. Trade barriers remain a risk, but the region is set to remain among the fastest-growing globally.

North America delivered a more measured rise of 7.4%, a step down from an exceptional 2024. A weaker US dollar offset strong equity gains, while performance remained concentrated in a narrow group of mega-cap technology stocks. That concentration leaves the market vulnerable to a correction if the AI capital expenditure cycle turns. Growth is expected to average around 7% annually through 2030, in line with global wealth.

Western Europe was the year’s positive surprise, rising 15.3%. This growth was supported by favorable currency movements and a persistently high household savings rate. Underlying equity market performance remained modest, driven by weaker economic momentum and limited exposure to high-growth sectors. Over the next five years, wealth creation in the region is expected to grow at an annual rate of 5%.

In the Middle East and Africa, nominal wealth grew 12.3% in line with a broader rally in emerging markets. Accelerating economic diversification and strong investment activity in the Gulf States underpinned this growth, alongside robust GDP expansion across Sub-Saharan Africa. A 7% five-year CAGR shows real structural momentum, tempered by geopolitical uncertainty, uneven inflation, and the underdeveloped capital markets that still characterize much of the African continent.

From Concentration to Clustering

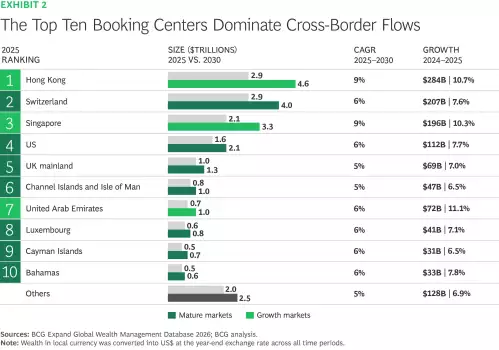

Cross-border wealth rose 8.4% to $15.7 trillion in 2025, lifted by strong market performance and heightened demand for geographical diversification. The top ten booking centers took almost 90% of new cross-border flows. (See Exhibit 2.) They also hold over 80% of existing stock. Concentration is not new in this industry, but it is intensifying.

Cross-border wealth rose 8.4% to $15.6 trillion in 2025, lifted by strong market performance and heightened demand for geographical diversification.

For the first time, Hong Kong narrowly overtook Switzerland as the world’s largest cross-border booking center. (See Exhibit 3.) Cross-border wealth rose 10.7% to $2.9 trillion, driven by mainland China flows and a vigorous stock market that delivered significant IPO activity and strong gains in benchmark-heavy internet platforms. With mainland flows representing over 60% of assets under management, Hong Kong is cementing its role as China’s gateway to global markets, though that same concentration ties its trajectory tightly to economic and regulatory developments on the mainland. Growth of around 9% annually is projected through 2030.

Switzerland, also at $2.9 trillion, grew 7.6%. Its client base is oriented toward Western European markets, with less exposure to the fast-growing market inflows that powered rivals, though that positioning may prove an advantage as geopolitical uncertainty reaffirms Switzerland’s role as a core global booking center, attracting flight-to-safety flows from more volatile regions such as the Middle East. Growth is expected to average around 6% annually through 2030.

Singapore is positioned as the most diversified wealth hub in Asia, serving as a neutral conduit between Asian and Western capital markets. That role has made it a beneficiary of safe-haven flows amid US-China tensions. Regulatory stability, institutional credibility, and a strong wealth management ecosystem have attracted over 2,000 single family offices to the city-state as well as more than 100 independent wealth management firms. (See “Independent Wealth Managers Are a Rising Force.”) Cross-border wealth rose 10.3% in 2025 and should stay at around 9% annually over the next five years.

Independent Wealth Managers Are a Rising Force

IWMs combine discretionary and advisory offerings, operate with lower client thresholds than private banks (around $250,000 in many markets), and typically do not rely on a banking license or proprietary product platforms. This translates into distinct client advantages: open-architecture advice without pressure to push in-house products, diversification across custodians, and integrated access to a broader range of services. Independent WMs also tend to see lower advisor turnover, longer client relationships, greater flexibility in executing bespoke investments, and a more personalized experience at lower wealth tiers. A $10 million client may be entry level at a large bank, but a core relationship for an IWM.

The channel’s scale and growth trajectory vary considerably across markets, with emerging booking centers now outpacing mature ones by a wide margin. (See the exhibit.)

Where the Model Is Under Pressure

While we project growth to remain strong in many markets, IWMs now face challenges that disproportionately affect smaller players, particularly in mature markets.

Recruiting senior bankers and their books has become less economical in the US, UK, and Switzerland given tighter retention programs and non-competes; in Singapore, Dubai, and Brazil, the constraint is talent scarcity. Either way, hiring-led growth is harder and more expensive than it was.

The personal nature of the IWM model, long its greatest strength, is becoming a vulnerability. In mature markets, relationships tied to individual advisors often do not transfer as clients hand over wealth, and many next-generation clients choose a different advisor. Firm succession compounds the issue. IWMs are typically founder-driven, so when the senior advisor retires, many firm faces a continuity question, often resolved through a sale or wind-down.

Margins are under pressure from compliance burdens, retrocession restrictions, and rising technology and cyber resilience requirements. Clients expect bank-grade reporting, mobile access, and AI-enabled interaction. Furthermore, emerging-market clients often set a higher bar than European clients accustomed to quarterly PDF statements.

As a consequence, custodian banks and platform providers are becoming de facto operating systems for sub-scale IWMs, bundling technology, reporting, regulatory expertise, and AI-enabled investment infrastructure. However, that relationship creates dependency and shifts the financial benefits upstream.

The net result is an increase in IWM consolidation. Private-equity-backed roll-ups dominate in the US and UK, with European examples emerging and platform-led consolidation taking hold in Brazil.

Four Strategies That Are Working

IWMs have resilience on their side. Many of the pressures they face have been building for years, giving the industry time to respond. Through our interviews with independent WM founders, custody banks, and association members, we have identified four models that show especially strong promise:

- The Segment Specialist. Focuses on a specific demographic (Indian clients in Dubai, Chinese families in Singapore) or occupation (athletes, doctors, tech executives). Tight referral networks make client acquisition capital-efficient. Firms typically remain small and rely heavily on outsourcing.

- The Large-Scale Consolidator. Acquires sub-scale firms, moves them onto a common platform, centralizes the investment office, and captures margins through back-office efficiency. This approach is the dominant scale play in the US and UK. Stronger players preserve advisor autonomy so the client experience remains local while the cost base is industrialized behind the scenes.

- The Upmarket Multi-Family Office. Targets relationships at or above $10 million, with deep investment capabilities and a multigenerational approach spanning tax, estate, philanthropy, governance, operating-business advisory, and deal access. In-house structuring is the differentiator, including bespoke certificates, co-investments, and club deals. Growth is referral-driven and deliberately measured.

- The Digital Multi-Family Office. Extends the multi-family office model to the $1 million to $10 million segment through technology-driven portfolio construction, alternatives access, tax tools, and reporting. The bet is that AI and modern infrastructure can deliver much of the multi-family office experience at a fraction of the cost.

For incumbent banks, the independent WM channel is a structural competitor for high-net-worth and ultra-high-net-worth share. Banks must decide whether to support independent WMs as custodians and partners or compete with them directly by building independent channels alongside the bank.

The US slowed to 7.7% growth, reaching $1.6 trillion as tariff uncertainty and a softer dollar dampened demand and reduced inflows from other regions. Latin American cross-border wealth remained a steady source of support. Over the next five years, growth is expected to average around 6% annually.

The UAE has been among the fastest-growing booking centers in recent years, with cross-border wealth increasing by 11.1% to $721 billion in 2025. The rapid development of financial infrastructure in the Dubai International Financial Centre and the Abu Dhabi Global Market helped enable this rise, along with the country’s appeal as a secondary domicile for international high-net-worth (HNW) individuals. Near-term risks remain elevated given regional tensions, with inflows potentially turning negative. Any projections for the Middle East carry an unusually high degree of uncertainty, and the following estimates should be read in that light. In a base case where conditions stabilize in the second half of the year, growth is expected to resume at around 6% annually, bringing cross-border wealth to more than $900 billion by 2030.

In the UK, cross-border wealth grew 7.0% to around $1 trillion in 2025, but changes to non-domicile and inheritance tax regimes are redirecting HNW outflows, and growth is expected to slow to around 5% annually through 2030.

Across booking centers, wealth creation is becoming more equity driven, favoring regions with strong capital markets and deep investment ecosystems. At the same time, geopolitical fragmentation is reinforcing the emergence of two hub networks, one anchored by Hong Kong and Singapore that serves mainland Chinese, Indian, and Southeast Asian capital, and one anchored by Switzerland, the US, and the UK, serving European, Middle Eastern, and Latin American wealth.

Booking centers that credibly straddle both clusters will command a structural premium, though achieving that position is a significant strategic undertaking and will not make sense for all market participants. The UAE’s trajectory after the current conflict will be the clearest test of whether that positioning can survive geopolitical stress.

The forces driving wealth creation and those determining where wealth is booked are converging. That alignment is new, and it is accelerating. The centers that sit at the intersection of deep capital markets, political stability, and genuine cross-border reach are growing faster and making it harder for others to close the gap.