For global technology executives, following developments on the trade front can be gut wrenching. Until very recently, the technology industry was, for the most part, left out of the tit-for-tat tariff increases announced by Washington and Beijing. But suddenly, the tech industry finds itself at the center of an escalating trade war.

This should come as no surprise. The tech industry is a major contributor to the US trade deficit with China. Consumer electronics such as smartphones, personal computers, and TVs alone accounted for around $130 billion of the 2018 trade gap in goods of $419 billion, which the current US administration has stated it wants to slash nearly in half. Achieving that target only through increased Chinese purchases of such US products as soybeans, liquefied natural gas, and commercial aircraft, as China has reportedly offered to do, is mathematically impossible. If trade deficit reduction is the primary US objective in negotiations, technology products will inevitably have to be on the table.

While the headlines may be dominated by tariffs, there are other major issues regarding the technology industry that further complicate the US view of its trade relations with China and are shaping its policies. They include treatment of intellectual property, access to markets for digital services, and government intervention in support of national champions in strategic sectors such as semiconductors. These issues are all arising within a context of heightened cybersecurity concerns and a race for global leadership in critical new technologies, such as 5G cellular networks and artificial intelligence.

It’s impossible at this point to predict how the current trade dispute between the US and China will play out. But it is becoming increasingly likely that—for better or worse—there will be no returning to the previous status quo for the tech industry. Any “deal” that may emerge from talks between Washington and Beijing will be just one step in a long process of working through geopolitical tensions in the growing strategic competition between two superpowers, both of which regard technology leadership as a critical advantage. These dynamics are likely to redefine the global context for the technology industry for the next one or two decades. As explained below, we see several potential scenarios for how the new US−China technology trade relationship will unfold, ranging from what we call “true reciprocal access” to “technology cold war.” And since any deal will cross many industries, it can present substantial challenges or opportunities to any given tech sector and product line.

Given the uncertainty, a wait-and-see approach may at first seem logical, based on the assumption that either a deal will eventually be reached or nothing can be done anyway. But we think it’s not only possible but critical for technology CEOs to think proactively and start taking steps to adapt quickly to the new context. Companies should evaluate potential scenarios for each of their different businesses, products, or services and take actions to mitigate risk, make their organizations and supply chains more resilient to shifting trade rules, and prepare strategies to seize any competitive advantage that the changes may afford them.

And this is important not just for US and Chinese companies. Every major technology company that has substantial operations in China or the US, and for which either nation is a primary end market, will be affected by these changing trade dynamics and needs to be prepared.

It is becoming increasingly likely that—for better or worse—there will be no returning to the previous status quo for the tech industry.

Why the Technology Trade “Deficit” Is Hard to Resolve

The large US−China deficit in technology products reflects the structure of the technology industry, with its large, truly global supply chains. For many finished electronics goods, China is the primary assembler of imported components and materials. With its massive manufacturing capacity, China accounts for nearly half of worldwide exports of electronic devices. The US is particularly dependent: approximately 70% of its combined imports of major consumer electronics such as smartphones, laptops, and TVs originate in China. The next three largest suppliers—Mexico, South Korea, and Vietnam—account for only 19% combined.

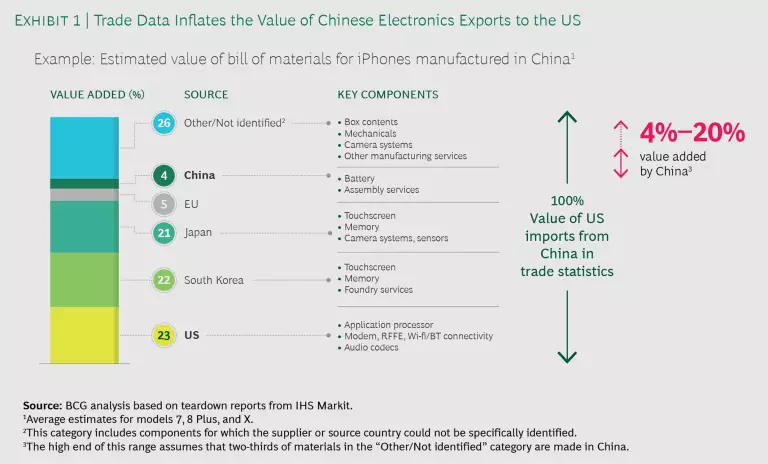

The often cited example of the iPhone—one of the biggest single contributors to the bilateral deficit statistics in the technology sector—is a good illustration. Most of the bill of materials for an iPhone consists of components from suppliers in the US, Japan, South Korea, the European Union, and other nations. While trade statistics count the full cost of the device as a US import from China, we estimate that the actual value that China adds to the average iPhone is somewhere between 4% and 20%. (See Exhibit 1.) Measuring imports in terms of Chinese value added rather than the full value of the device would reduce the US−China deficit in computers, electronics, and electrical equipment by some 70%, according to a BCG analysis based on international trade data from the Organisation for Economic Co-operation and Development.

However, because the US has set its trade objectives based on the total value of devices imported from China, rather than on the value-added measurement, one option for reducing the size of the tech industry trade deficit is to reshore manufacturing back to the US. It will certainly be possible for US technology companies or their foreign manufacturing subcontractors to reshore some Chinese electronics assembly—particularly if high tariffs are imposed on Chinese-made products such as smartphones, personal computers, and televisions. As BCG’s Manufacturing Cost Competitiveness Index has shown, the cost differentials between coastal China and advanced industrial economies have shrunk over the past decade, largely because Chinese labor costs have risen faster than productivity. Although manufacturers could partially compensate by shifting work deeper into China’s lower-cost interior, the tariffs could make the manufacturing math favor the US in some cases.

But it’s also important to keep in mind that for many products for which labor cost is an important factor and for which automation is difficult, it will be more economical for companies to shift production to other offshore locations, such as Southeast Asia or Mexico—effectively reducing the US trade deficit with China but increasing imports from the countries that replace China as manufacturing hubs. In the case of certain electronic devices that are associated with perceived cybersecurity risks, however, bypassing China in the supply chain may in itself be a reason for the US to push for re-sourcing—even if the net impact on the overall trade deficit is not material.

In any case, opportunities to cost-effectively reshore and re-source consumer electronics will be limited and would take years to implement. In some consumer electronics segments, there is a strong argument that China is at the center of complex global value chains and is therefore virtually irreplaceable. China’s major regional suppliers, such as South Korea and Malaysia, have built their businesses around feeding China’s manufacturing facilities. The Wall Street Journal has reported that some major global electronic manufacturing services companies have struggled to set up large factories in the US, suggesting that China’s manufacturing advantages and scale make it difficult to replace as a major source of many consumer electronics devices.

In some consumer electronics segments, there is a strong argument that China is at the center of complex global value chains and is therefore virtually irreplaceable.

The experience of some electronics goods targeted in the initial round of tariff hikes introduced in July 2018 supports the argument that higher tariffs will not meaningfully alter the bilateral flow of some products. For example, although US imports of Chinese printing machinery dropped marginally, Chinese shipments of electrical machinery increased by around 5%, to $154 billion, in 2018. At the same time, China’s retaliatory tariffs likely contributed to the year-on-year drop in US exports to China. The current restrictions, due to intellectual property or security concerns, on US exports to China of some leading-edge technology products for which Chinese demand is booming, such as high-end computers and semiconductors, are likely to further inhibit deficit reduction.

US tariffs on Chinese products could also affect the ability of American technology companies to tap into the vast, burgeoning Chinese consumer market. Even though goods that US companies build in China for the domestic market do not appear in the bilateral trade balance, the Chinese government could regard their sales as US revenues—and use them as leverage to retaliate against US tariffs. In fact, during previous Chinese political or economic disputes with Japan and South Korea, Chinese consumers shunned brands associated with those nations.

The Potential for Improved Trade in Digital Services and IP

Often obscured in the discussion of trade deficits is the role of revenues earned from intellectual property and digital services—particularly given that the levers to fundamentally change the bilateral flows in manufactured goods appear somewhat limited. Although the US had a $419 billion trade deficit in goods with China in 2018, it registered a $40 billion surplus in services. And the US enjoyed a $51 billion worldwide balance of payments surplus in IP revenue in 2017, according to the International Monetary Fund—nearly double China’s offshore earnings from IP.

Both IP and digital services such as cloud storage, content streaming, and e-commerce are sectors in which US companies could gain from better access to Chinese domestic markets, leading to a significant uplift in US exports and thereby contributing to an overall reduction in the trade deficit.

Intellectual Property. Ensuring that foreign companies can make market-based licensing agreements for their IP in China—and secure stronger protection of their patents—is a US objective. IP has been a source of tension, with disputes over licensing and antitrust practices that go to the heart of US−China technology competition.

The US has challenged China’s technology-licensing practices through the World Trade Organization, alleging that they are imposing discriminatory obligations on US licensors in China and mandatory ownership of improvements by the Chinese licensee. A WTO panel is adjudicating the dispute.

In parallel, China has openly criticized the structure of the global technology industry, arguing that a small number of foreign companies generate high margins selling end-user devices at high premiums by leveraging their IP to block competition from emerging Chinese challengers through either high royalties or the threat of litigation. Over the past few years, China has been investigating alleged anticompetitive practices by some high-profile foreign technology companies doing business in China.

Both IP and digital services are sectors in which US companies could gain from better access to Chinese domestic markets.

Cloud Services. Asia-Pacific is the fastest-growing cloud storage market, and China is the largest and fastest-growing market within that region. In its March 2019 National Trade Estimate, the Office of the United States Trade Representative (USTR) lists several digital trade barriers imposed by China that inhibit access by foreign cloud providers. China’s Cybersecurity Law and a range of related implementing regulations, for example, restrict cross-border data flows and impose data localization requirements. China prohibits foreign companies from directly providing cloud-computing services to customers in China. Instead, it requires foreign providers “to partner with a Chinese company and to turn over to that partner their technology, know-how, and brands in order to enter the market,” the USTR report states.

Although China continued to reduce formal restrictions on foreign investors in 2018 by removing foreign-equity caps and joint-venture requirements, the USTR alleges that the Chinese government still restricts access to the cloud market through administrative licensing and approval processes.

Streaming and E-commerce. China is the world’s second-largest market for subscription video-streaming services, with $3.7 billion in revenue in 2018, according to Digital TV Research, and is set to grow rapidly. China already leads the world in e-commerce revenues. A growing number of Chinese internet-based companies, meanwhile, have attained the expertise and technological capabilities to successfully compete globally.

Access to China’s domestic market in many of these sectors may be restricted, however. The USTR claims that China’s “extensive blocking of legitimate websites” is “affecting billions of dollars in potential US business.” China blocks 10 of the top 30 global sites and more than 10,000 domains, according to the USTR.

Progress in achieving a more open trade environment for IP and digital services such as cloud storage, streaming, and e-commerce could contribute to a better balance of US−China trade. However, these levers alone will not make a big impact on related US objectives, such as bringing manufacturing jobs back to the US or minimizing perceived cybersecurity threats.

Potential Scenarios for a New Tech Trade Paradigm

“Fixing” the bilateral tech trade deficit and satisfactorily addressing mutual concerns on complex issues such as IP, market access, and cybersecurity will not be easy. Multiple outcomes, all of which encompass significant change and can affect sectors positively or negatively, are possible.

The new US−China technology trade relationship can be framed in terms of potential changes along two key dimensions: the scale and scope of bilateral tariff measures and the dynamics of technology competition, which may involve industrial policy or nontariff barriers, such as export and import restrictions in the name of national security. Tariff measures can range from narrow and targeted to broad and sweeping. The emerging bilateral relationship regarding technological competition can range from open trade to managed trade, under which specific technologies and even companies are singled out for trade restrictions. Based on this framework, we see four potential scenarios for the US−China tech trade relationship. (See Exhibit 2.)

- True Reciprocal Access. Under this scenario, the US and China resolve key differences that inhibit technology trade. For example, they may refocus the measurement of the trade deficit in goods on value added, agree to improved terms on licensing US intellectual property to China, and open up most of their respective digital-services markets. They may also allow cross-border technology mergers and acquisitions. The US rolls back broad-based tariffs but may continue to impose tariffs or other barriers to market access on a narrow and targeted basis in response to industry petitions regarding dumping or subsidization, or in response to alleged IP, privacy, or security infringements. As a result, the US trade deficit is reduced moderately in the short run by a rise in US services. In the long run, the deficit could be reduced by market-based supply chain shifts, as Chinese costs rise and more electronics manufacturing companies invest in capacity in the US or in countries such as Vietnam, India, Brazil, and Mexico.

- Managed Trade. The two countries agree to a framework to manage trade and technology competition. Broad-based tariffs are rolled back in the context of a meaningful bilateral trade agreement for tech and other sectors. The US places or maintains selective tariffs, export and investment restrictions, or market access barriers on only a few sectors and products that it considers strategically important or highly important to national security, such as supercomputers, 5G, and advanced semiconductors. At the same time, China maintains nontariff restrictions in order to build technological competitiveness. The bilateral trade gap changes little over the short to medium term under this scenario.

- Walls and Drawbridges. The US and China fail to resolve bilateral structural issues, leaving each side’s policies regarding IP, investment, licensing, and other nontariff matters essentially unchanged. In the absence of agreed-upon solutions to these issues, the US deepens and selectively broadens its tariffs on Chinese imports, although these may stop short of hitting the most popular consumer electronics products, such as smartphones, laptops, and TVs. The bilateral trade balance could change moderately. Uncertainty remains high for technology companies, with no clearly established framework to manage friction in areas such as IP, cross-border M&A, antitrust, and cybersecurity. Instead, each individual dispute becomes a bargaining chip in the geopolitical conflict between the two countries.

- Technology Cold War. The US and China further escalate nontariff restrictions, including US bans on specific high-tech exports to China. China restricts exports of essential materials such as rare earths, takes antitrust measures against US tech companies, and accelerates indigenous technology development efforts. In response to concerns over IP protection and national security, the US broadens its tariffs or market access restrictions to cover all valuable electronics—including consumer electronics. In an extreme but not implausible case, cyberattacks—such as the one in October 2016 in which hackers gained access to websites by inserting malware into connected devices such as baby monitors, web cameras, and routers—could cause every single networked electronic device imported from certain countries to be considered a potential threat and therefore banned. This would effectively halt the bulk of bilateral technology trade and prompt a massive redefinition of global technology supply chains. It would also lead to fragmentation of global technology standards in areas such as telecommunications, computing architectures, and operating systems.

The impact of each of these scenarios would vary widely by company, depending on its products, service offerings, supply chains, and manufacturing footprint. In fact, a company could have businesses, products, and services susceptible to different scenarios. For a company that sells semiconductors as well as electronic devices and digital services, for instance, the new trade relationship would affect different parts of its business in different ways.

Building Resilience Within a New Trade Paradigm

As negotiations continue to start, stall, and stop—and as various enforcement mechanisms are engaged—each of the scenarios described above could materialize, and potentially even coexist, depending on the specific technology or company. Rather than try to predict which scenario is most likely, we recommend that companies analyze their business and products against each scenario. They can then take proactive steps to minimize risk, make their organizations more resilient to change, and gain competitive advantage.

In our experience with clients across sectors, we have found that companies that take the following actions can best maximize their opportunities in the new global environment, however it plays out.

Analyze exposure and develop playbooks. Building a fact base can help companies understand how their value chains are exposed to each scenario in terms of revenues, costs, and asset allocation. This will enable them to estimate the impact of potential tariffs and technology restrictions on their businesses.

Companies should then create a playbook of actions to take under each scenario. This will help them adapt quickly when actual change comes. For example, a company might identify alternative production sites and suppliers in other nations that can meet its needs and assess how those alternatives would affect production costs, quality, and speed to market.

Companies that are truly well prepared will have assessed the exposure not only of each of their own product lines, but also that of key competitors in each segment. Identifying relative differences in impact may reveal new competitive advantages and disadvantages.

Consider this powerful example of forward-looking planning amidst the current US−China trade friction. When the US first indicated that it would raise tariffs on products imported from China, the senior leadership of a durable-goods company began reviewing the implications of potential scenarios three months before the initial round of tariffs were to be levied. By the time the US raised tariffs from 10% to 25% on a broad set of imports, the company had already begun more than two dozen cross-functional mitigation projects with oversight from top management. Meanwhile, many of its competitors waited for the US and China to make a deal that would bring back the previous status quo. As a result, while its competitors were just beginning the process of analysis and adaptation, the company had gained a 9- to 12-month advantage.

Companies that are truly well prepared will have assessed the exposure not only of each of their own product lines, but also that of key competitors in each segment.

Be proactive to build resilience. We recommend that companies identify a series of no-regrets moves, such as creating sourcing options by prequalifying new suppliers. They can also consider deploying automation and other advanced technologies that could change the economics of their supply chain. And beginning the shift toward more flexible, regional approaches to global manufacturing supply chains, a move BCG has long advocated on its own merits, will bring additional resilience in the current trade dynamic. Some major Chinese consumer electronics manufacturers, for example, have been expanding their manufacturing networks by adding capacity in nations such as India, Vietnam, Brazil, and Mexico to serve growing consumer demand in Southeast Asia and Latin America.

The apparel industry, which by the nature of its products requires highly flexible and responsive supply chains and is often subject to changes in trade rules and labor rates, is a good example of how to proactively build resilience. Some leading apparel players have designed their global industrial models around a series of trade agreements linking production facilities in countries with acceptable costs to markets for finished goods in North America and the European Union. This has allowed them to modulate production by product and market type in the event that any of these trade agreements is disrupted.

In addition, ensuring end-to-end transparency and integrity of the supply chain—such as through the Internet of Things or blockchain, which enables goods and digital products to be traced in real time—is likely to be increasingly critical to compliance with heightened scrutiny and could potentially serve as a competitive differentiator in a world with high cybersecurity concerns.

Shape policy. Finally, while there is still time, company leaders should consider seeking to influence the shaping of detailed policy to create relative advantage. Of course, determining which policies to advocate requires careful analysis. They might be broad and structural, or perhaps more technology specific. Companies should determine whether it is most effective to work in tandem with other companies through industry associations or to voice concerns specific to the company on their own. Different approaches will be required for authorities in China and the US, given the different political systems.

During the recent NAFTA renegotiations, several companies in the automotive sector—makers of cars, buses, and recreational vehicles, as well as tier one suppliers—conducted deep evaluations, such as those mentioned above, of how their supply chains would be affected by the proposed new rules. They also assessed how those rules would impact competitors, given their different product portfolios and global supply chain structures. These companies were able to identify where the proposed rules would have an asymmetrical impact on them compared with the rest of the sector and, potentially, create a relative competitive advantage. These companies then translated this information into robust, detailed materials for their discussions with policymakers.

Given the broad underlying geostrategic and technological dynamics, it is clear that US−China tensions surrounding trade in general, and technology trade in particular, will persist for years. This will present risks, to be sure. But change will also open opportunities for companies in both China and the US. For technology companies, we see no advantage in waiting: every day lost is another day of growing risk. A proactive and strategic approach will enable resilient technology companies to navigate through the uncertainty and thrive as the world’s most important trade relationship is reset.

The authors thank their BCG colleagues Pete Engardio, Ali Kchia, Patrick Ward, and Yang Yankang for contributions to this article.