For dealmakers, 2026 begins with a sense of déjà vu. A year ago, they expressed renewed optimism that the long-awaited rebound in global M&A activity might finally be underway. Although that recovery did materialize, it emerged only in the second half of the year—later and more unevenly than many expected.

Now, as 2026 begins, the macroeconomic backdrop again looks supportive. Inflation eased throughout much of 2025, interest rates declined modestly, company valuations recovered across multiple regions, and capital markets have stabilized. Corporate and private equity deal pipelines are fuller than they have been in several years.

Yet uncertainty remains a defining feature of today’s environment. Economic-policy uncertainty, geopolitical tensions, and unexpected political developments continue to weigh on executives’ confidence.

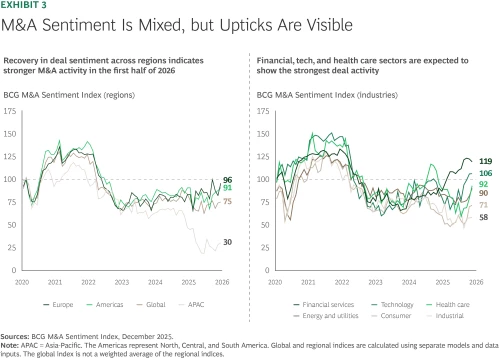

Reflecting this complex landscape, BCG’s M&A Sentiment Index suggests measured confidence as dealmakers enter 2026. Although markedly improved from its lows, the global index remains below long-term historical averages. However, sentiment in Europe and North America has returned close to its historical average. At the same time, sector-level sentiment is trending upward globally, with technology and financial services now above their long-term averages. The result is a familiar starting point for the year: optimism is rising once again, but confidence remains sensitive to shifting macroeconomic and geopolitical signals.

The Late-Blooming Recovery of 2025

Although financial conditions steadily improved in 2025, many dealmakers remained cautious for much of the year. Lingering economic uncertainty, persistent inflationary concerns, evolving monetary policies, and ongoing regulatory and geopolitical challenges kept dealmakers on the sidelines until confidence firmed.

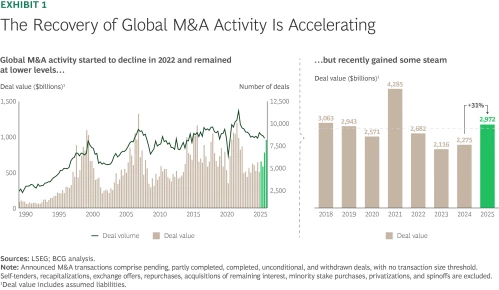

Activity accelerated primarily in the year’s second half, with aggregate deal value 40% higher than in the first half. For the full year, global M&A value reached $3.0 trillion in 2025, an increase of 31% compared with the previous year and slightly above the ten-year average of roughly $2.9 trillion. (See Exhibit 1.) Deal volumes, by contrast, remained broadly stable. There were approximately 33,000 majority M&A deals in 2025, compared with approximately 33,800 in 2024—well below the record high of approximately 41,300 in 2021. These trends point to a rebound driven primarily by larger transactions in 2025 rather than a broad-based increase in dealmaking.

North America was the most active region for acquisitions in terms of deal value. The technology, media, and telecommunications (TMT) sector led among industries in terms of aggregate deal value, while the industrial sector showed the highest growth. (See “Region and Sector Insights.”)

Region and Sector Insights

- Deals involving targets in North America had a total value of $1.9 trillion, an increase of approximately 58% versus 2024. The vast majority (worth $1.8 trillion) involved targets in the US, accounting for 60% of overall global M&A activity. US companies acquired most of these targets. Globally, most megadeals announced in 2025 involved US acquirers and targets.

- Targets in South and Central America accounted for $73 billion in deal value, marking an increase of 25% from the previous year.

- The value of European M&A totaled $524 billion, a 1% decrease versus 2024. Aggregate deal value increased in the Netherlands (341%), Switzerland (80%), Germany (57%), and Sweden (42%), but the deal value decreased in the UK (–30%), Spain (–50%), France (–19%), and Italy (–1%).

- In Africa, deal value decreased by 14% to $12 billion, while in the Middle East it remained fairly stable at $21 billion (up 3%).

- Asia-Pacific’s deal value was $440 billion in 2025, a 3% decline from 2024. The regional total was marked by declines in Hong Kong (–64%), Japan (–30%), India (–12%), and Australia (–3%). Brighter spots included Mainland China (45%), Singapore (18%), and South Korea (5%).

- In 2025, the industrial sector posted the strongest gains in aggregate deal value, rising by 91%, driven by several large deals and a fairly low base in 2024.

- Health care also showed a significant uptick (68%) over the previous year’s low numbers, signaling a return to more normal levels.

- Deal value in the TMT sector grew by 49%, driven significantly by megadeals across all three subsectors.

- The energy and utilities sector also returned to more typical activity levels, increasing by 33%.

- The financial services and real estate sectors were slightly more active (7%) in 2025.

- The consumer sector showed a decline in activity in 2025 (–7%), with retail M&A falling by 29%. Activity rose in consumer staples (9%) and products and services (3%).

- The materials sector—which was very active in 2023 and 2024—also saw a correction in activity, declining by 7%.

Large deals—those valued at or above $500 million—rebounded strongly, with approximately 900 transactions in 2025, exceeding the number of 2024 deals by more than 100. (See Exhibit 2.) After a dip in April, monthly activity returned to the typical global range of roughly 60 to 80 transactions, reflecting dealmakers’ ability to adjust quickly to shifting political, economic, and market conditions.

Notably, 2025 marked the return of megadeals. A total of 39 transactions valued at more than $10 billion were announced in 2025, compared with 28 in 2024, though still below the record 51 seen in 2021. Private equity and venture capital activity also trended higher, driven in part by a higher number of large deals. (See “Spotlight on Megadeals and Private Capital.”)

Spotlight on Megadeals and Private Capital

- The year ended with rival offers for Warner Bros. Discovery. Paramount Skydance tendered an offer valuing the company at $74.3 billion, surpassing Netflix’s offer of $69.9 billion. The situation remains fluid, with revised offers still possible.

- Union Pacific announced its $71.5 billion acquisition of railroad operator Norfolk Southern, marking a major consolidation in US freight transportation.

- A consortium comprising Silver Lake, Saudi Arabia’s Public Investment Fund, and Affinity Partners is acquiring gaming company Electronic Arts in a deal that values the company at approximately $49.4 billion. If completed, it will be the largest leveraged buyout ever (not adjusting for inflation).

- Kimberly-Clark’s intended acquisition of Kenvue, a maker of consumer health products, is valued at $42.8 billion.

- Data processing and hosting-services company Aligned Data Centers is being acquired for $40 billion by an investor group comprising the AI Infrastructure Partnership, Global Infrastructure Partners (part of BlackRock), and MGX.

- Tech giant Alphabet is pursuing strategic growth in cloud security by acquiring the software company Wiz for $32 billion.

- Electric utility Constellation Energy is expanding its footprint through a $26.9 billion deal for power generator Calpine.

- Palo Alto Networks is reinforcing its competitive position by acquiring CyberArk for $25.1 billion, intending to create an end-to-end security platform tailored for AI.

Private capital also played a substantial role. Global private equity’s deal value rose by 59% in 2025, compared with the value in 2024. Firms continued to hold approximately $2 trillion in undeployed capital as of December 2025, maintaining pressure to deploy strategically even as global fundraising slowed from its 2021 peak.

In venture capital, funding levels climbed by approximately 60% globally, according to Crunchbase data. However, these levels remained below the highs of 2021 and 2022. AI and AI-related companies are still a primary focus for venture investment, despite ongoing market concerns about high valuations, market saturation, and less certain growth trajectories. Companies such as OpenAI, Scale AI, and Anthropic benefited from several megafunding rounds.

Finally, several long-awaited initial public offerings in late 2025 have set the stage for increased IPO activity in the year ahead. The number of companies going public is often an indicator of momentum for M&A activity. The pipeline is full of promising candidates waiting for more favorable market conditions.

Sentiment Heading into 2026

As dealmakers look ahead, their sentiment offers an important signal of how confidence is shifting across regions and sectors. BCG’s M&A Sentiment Index captures this evolving outlook. Although the global index has recovered strongly from its low point in late 2022, the current value of 75 remains well below the long-term average of 100 and has slipped from 88 in October

Optimism is highest in Europe. (See Exhibit 3.) The index rose sharply to 96 in December 2025—below the September 2025 peak of 100 but well above the value of 66 recorded in February 2025—indicating renewed confidence and an expectation of increased deal activity. In the Americas, sentiment continued to trend upward. The index rose to 91 in December 2025, up from 68 in August, indicating a steadier footing heading into 2026. In contrast, sentiment in the Asia-Pacific region remains subdued. The index value of 30 reflects continued uncertainty, driven in part by questions around economic policies and macroeconomic activity.

Sentiment across sectors has also been trending upward. While all major sectors show improving conditions, several stand out as particularly well-positioned for increased activity in the coming months. The financial services and technology sectors signal above-average activity, with both sectors buoyed by strong fundamentals and notable deal momentum. The consumer and industrial sectors remain more cautious, though both contain subsectors that are expected to be more active as conditions continue to normalize.

These sentiment patterns offer a preview of potential dealmaking activity in 2026.

Where M&A Activity Is Likely to Accelerate

Several sectors stand out for their strong momentum, structural drivers, and recent deal activity, offering a clearer picture of where M&A is poised to intensify in the year ahead.

TMT. The TMT sector continues to be one of the most dynamic areas of global M&A. In 2025, sizeable deals across all three subsectors highlighted strong underlying fundamentals and ongoing transformation. Given the sector’s sustained momentum, deal activity in TMT is likely to continue at a robust pace in 2026.

In the US, the technology subsector remains a focal point for both strategic and financial investors. The ongoing AI boom—and the resulting demand for data centers, chips, cybersecurity, cloud infrastructure, and related technologies—continues to fuel significant dealmaking. For example, Electronic Arts and Aligned Data Centers were recently acquired by financial investors, while Wiz and CyberArk Software were purchased by corporate acquirers. There have also been notable financing transactions and strategic partnerships across the AI value chain.

Financial Services. Financial services’ subsectors, including banking, payments, asset management, and insurance, are poised for further consolidation and portfolio repositioning in 2026.

Europe was a particularly active region in 2025. Dealmaking activity spanned subsectors, with the announced merger of Swiss insurers Helvetia and Baloise and Deutsche Börse’s discussions to acquire the Allfunds platform.

More notably, however, activity picked up in traditional banking, indicating that the subsector’s long-awaited consolidation might finally gain steam. A series of transactions and attempted deals underscored this shift:

- Italy-headquartered UniCredit built a stake in German Commerzbank and signaled an interest in an acquisition, while announcing—although later withdrawing—its intention to acquire domestic peer Banco BPM.

- Italian Banca Monte dei Paschi di Siena acquired a majority stake in Mediobanca, which subsequently launched an offer to acquire Banca Generali from insurance company Generali that was ultimately rejected.

- Italian BPER Banca made a tender offer to take over domestic rival Banca Popolare di Sondrio.

- French Group BPCE agreed to acquire a majority stake in Portuguese Novo Banco.

- French Crédit Mutuel Alliance Fédérale acquired German Oldenburgische Landesbank through its Targobank subsidiary.

- Spanish BBVA launched a takeover offer for Spanish Banco de Sabadell that eventually lapsed.

- Spain-headquartered Banco Santander’s UK unit agreed to acquire UK-based TSB Banking Group from Banco Sabadell.

Momentum is also strong outside Europe. Examples include the Global Payments acquisition of Worldpay and Nomura’s acquisition of Macquarie’s US and European public asset management business.

Health Care. This sector—particularly pharmaceuticals—remains an “always-on” for M&A. Global incumbents consistently seek promising targets to refresh pipelines, expand portfolios, and reinforce long-term growth. A recent deal highlighting the competition for promising targets is Pfizer’s acquisition of obesity drug developer Metsera, for which Novo Nordisk also submitted an offer. This steady strategic demand is likely to sustain activity in 2026.

Energy and Utilities. Robust dealmaking activity is set to occur in this sector as well. The energy transition—combined with steadily rising demand driven by electrification, data centers, and AI—continues to attract investment and fuel M&A activity across regions and subsectors, including oil and gas and renewables.

Industrial and Consumer. Even as these sectors continue to take a more cautious stance overall, certain subsectors are poised for increased activity. Almost all face a convergence of pressures, including supply chain disruptions, geopolitical and regulatory challenges, tariffs, and digital and AI transformation. M&A will be a critical lever as companies aim to build resilience, search for growth opportunities, or realign portfolios. For example, the materials subsector, especially metals and mining, benefits from growing demand for critical inputs such as rare earth elements. Transportation industries—including airlines, logistics providers, and supply chain services—also present promising opportunities.

Addressing Challenges amid the Optimism

As dealmakers prepare for a more active 2026, several risks and structural challenges continue to shape the M&A environment. These factors, while not derailing the broader recovery, demand careful consideration.

Managing Regulatory and Policy Complexity. Regulatory and policy changes remain a significant source of uncertainty. Antitrust scrutiny continues to complicate larger transactions, creating challenges in navigating approval processes and increasing unpredictability around outcomes and timelines.

Beyond antitrust, M&A processes are subject to heightened scrutiny as laws and regulatory frameworks evolve in areas such as data privacy, cybersecurity, and environmental, social, and governance standards. These factors are fundamentally reshaping how companies structure, evaluate, and execute transactions. Dealmakers must also contend with foreign direct investment restrictions, national security considerations, and sanctions policies, all of which can add friction and extend deal timelines.

Applying Discipline in Megadeals. The resurgence of megadeals brings both opportunity and risk. Larger transactions inherently carry higher stakes, and their complexity demands disciplined execution. A recent BCG analysis shows that companies with strong megadeal capabilities—including clear strategic rationale and robust integration playbooks—consistently outperform peers and mitigate downside risks. Since more megadeals are likely to be on the horizon, maintaining discipline will be critical to value creation.

Preparing Across the Deal Cycle. Effective M&A requires systematic preparation, not opportunism. Companies need clear strategies, target-selection criteria, financial guardrails, and strong diligence and integration capabilities. Deals fail more often because of a weak strategy and poor integration than because of price or diligence issues. As opportunities emerge in 2026, organizations that have invested in readiness will be better positioned to move quickly.

Signs point to 2026 as a potentially dynamic year for global M&A. Improving sentiment in key regions and sectors and stabilizing macroeconomic and financial conditions create fertile ground for renewed activity. At the same time, dealmakers must still navigate geopolitical complexity, heightened regulatory scrutiny, and the increasing sophistication required to execute transactions. A well-prepared strategic approach to dealmaking is therefore essential—not just to close transactions but also to create lasting value.