The increasing adoption of automation, artificial intelligence (AI), and other technologies suggests that the role of humans in the economy will shrink drastically, wiping out millions of jobs in the process. COVID-19 accelerated this effect in 2020 and will likely boost digitization, and perhaps establish it permanently, in some areas.

However, the real picture is more nuanced: though these technologies will eliminate some jobs, they will create many others. Governments, companies, and individuals all need to understand these shifts when they plan for the future.

BCG recently collaborated with Faethm, a firm specializing in AI and analytics, to study the potential impact of various technologies on jobs in three countries: the US, Germany, and Australia. Using the underlying demographics in each country, we developed detailed scenarios that model the effects of new technologies and consider the impact of the pandemic on GDP growth. (See Appendix A.)

One key finding is that the net number of jobs lost or gained is an artificially simple metric to gauge the impact of digitization. For example, eliminating 10 million jobs and creating 10 million new jobs would appear to have negligible impact. In fact, however, doing so would represent a huge economic disruption for the country—not to mention for the millions of people with their jobs at stake. Therefore, policymakers and countries that want to understand the implications of automation need to drill down and look at disaggregated effects. Understanding the future of jobs is a tall order, but the groundbreaking analysis we conducted helps governments, companies, and individuals take the critical first step to prepare for what is to come.

In This Report

- Three Components of Workforce Imbalances

- A Closer Look at Three Markets

- Growing Demand for Technological and Soft Skills

- Sensitivity of Outcomes

- Building an Adaptive Workforce

- Recommendations for Governments

- Recommendations for Companies

- Recommendations for Individuals

- The Way Forward

Three Components of Workforce Imbalances

In general, computers perform well in tasks that humans find difficult or time-consuming to do, but they tend to work less effectively in tasks that humans find easy to do. Although new technologies will eliminate some occupations, in many areas they will improve the quality of work that humans do by allowing them to focus on more strategic, value-creating, and personally rewarding tasks.

To understand the potential impact of new technologies on future workforces, we looked at three components of imbalances in the US, Germany, and Australia:

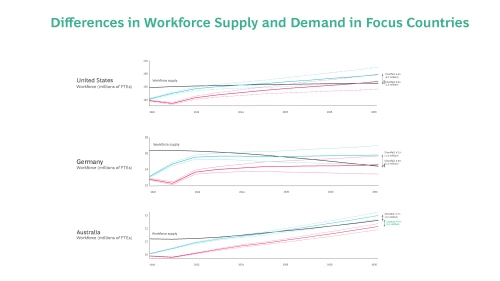

- Workforce Supply and Demand. We analyzed all elements that affect a nation’s full-time equivalent (FTE) workforce, including the number of college graduates and the rates of retirement, mortality, and migration. And we used standardized job taxonomies on a very granular level for both supply and demand. The taxonomies were based on 22 common job family groups, and close to 100 job families, found in countries all around the world. The three countries we studied for our analysis, however, showed slight variations in the numbers of job families—93 for the US, 86 for Germany, and 82 for Australia—because of differences in their national taxonomies. (See Exhibit 1.)

- Technology. To model the impact of technology, we used analytics provided by a Faethm platform to develop three sets of circumstances with different tech adoption rates. The technologies under consideration included programmed intelligence (predefined technologies, such as process automation and robotics), narrow AI (reactive technologies, such as tools that use machine learning to recognize and organize data), broad AI (proactive technologies that can sense external stimuli and make decisions), and reinforced AI (self-improving technologies, such as fully autonomous robots or those that can solve unstructured, complex problems). (See Appendix B.) We considered the medium adoption rate to be the standard, but we also evaluated adoption rates that were 25% faster and 25% slower than the standard in our analysis.

- GDP Growth. Given the continuing and dynamic evolution of the pandemic, we used two major COVID-19 projections to simulate future GDP growth: one is a baseline, while the other is more severe and has a longer recovery time. We leveraged data from Oxford Economics for both projections from 2018 up to 2025 and then used the baseline projections to extrapolate growth to 2030.

Looking at all of these factors gave us an aggregate impact of automation and economic growth on national workforces by 2030. Two economic forecasts, and three possible technology adoption rates, led to a total of six possible scenarios:

- Baseline COVID-19 projection: high, medium, or low rate of technology adoption

- Severe COVID-19 projection: high, medium, or low rate of technology adoption

Throughout this report, unless mentioned otherwise, we will refer to the midrange scenario, which comprises a baseline GDP forecast in response to the pandemic and a medium rate of technology adoption.

We find that the US will likely experience a labor shortfall in its workforce of 0.9% to 4.4% by 2030. Germany will also experience a shortfall, of 0.5% to 4.1%. And although Australia will experience a labor shortfall of up to 3.7% in the baseline scenario, it will experience a labor surplus of up to 4.0% if the pandemic causes a more severe impact on GDP growth. (See Exhibit 2.) These consolidated gaps are the difference between the total supply and the total demand in the future workforce for each country. This net number, however, is only an initial indication, and policymakers and business leaders need to look at the disaggregated perspective to see the full picture. Our research also reveals that automation will reduce the number of both unskilled jobs and white-collar positions.

The two additional sets of technology adoption circumstances that we considered would influence the labor curve accordingly. Faster adoption rates would lead to greater demand for people in specific occupations as well as greater surpluses in others that are more prone to automation. Slower adoption rates would lead to a less severe impact on the labor force. In total, the effect would be lower workforce demand.

A Closer Look at Three Markets

Taking the qualifications of the workforce into account in the form of job family groups generates a much more detailed picture.

United States. Talent shortfalls in key occupations, such as computer and mathematics, for the midrange scenario is set to soar from 571,000 in 2020 to 6.1 million by 2030. (See Exhibit 3.) The deficit in supply of architecture and engineering workers is also set to rise sharply, from 60,000 in 2020 to 1.3 million in 2030. So even though the country’s overall supply of labor is projected to rise, the US will face significant deficits in crucial fields. In fact, the sum of all job family groups with a shortfall is 17.6 million. Technology and automation will also drive people out of work in the US, particularly in office and administrative support, where the surplus of workers will rise from 1.4 million in 2020 to 3.0 million in 2030.

Germany. Germany is also projected to have a shortfall of talent in computer and mathematics by 2030: 1.1 million. (See Exhibit 4.) The next most severely affected job family groups are educational instruction and library occupations (346,000) as well as health care practitioners and technical occupations (254,000). Yet Germany’s overall shortfall of talent does not preclude workforce surpluses: production occupations, for example, are expected to rise from 764,000 in 2020 to 801,000 by 2030. This is a very good example of the shift from jobs with repetitive tasks in production lines to those in the programming and maintenance of production technology—and thus the need for significant reskilling (teaching employees entirely new skills needed for a different job or sector) and upskilling (giving employees upgraded skills to stay relevant in a current occupation).

Australia. Australia will experience difficulties in filling jobs in certain sectors, although the overall workforce supply looks less stretched. The greatest shortfall by far exists again in computer and mathematics, where the figure will rise to 333,000 by 2030. (See Exhibit 5.) The three job family groups with the next most significant shortfalls are management; health care practitioners and technical support; and business and financial operations.

However, technology will exacerbate Australia’s workforce surplus in certain sectors. For example, in production, the surplus will stay high, rising slightly—to 118,000—by 2030. And with technology taking over mundane, repetitive tasks, the surplus in office and administrative is expected to rise from 161,000 in 2020 to 180,000 by 2030. Nonetheless, the sum of all job family groups with a surplus is 0.6 million, while the sum of all job family groups with a shortfall is a cumulative 1.0 million jobs. Combining the two cumulative figures of shortfalls and surpluses gives the net workforce imbalances.

Growing Demand for Technological and Soft Skills

For all three countries, the development of labor supply does not fully match the changes in demand, except for certain occupations. At the same time, in many sectors, severe shortages of skilled workers will mean that growth in demand for talent will be unmet. This is particularly true for computer-related occupations and jobs in science, technology, engineering, and math, since technology is fueling the rise of automation across all industries. This is why the computer and mathematics job family group is likely to suffer by far the greatest worker deficits in all three countries.

Meanwhile, in job family groups that involve little or no automation but that do require compassionate human interaction tailored to specific groups—such as health care, social services, and certain teaching occupations—the demand for human skills will increase as well. Germany and the United States, given their overall human resource deficits, will face the greatest pressure for talent in these occupations. For example, Germany will suffer a shortfall of 346,000 people in the educational instruction and library sector by 2030. The deficit for health care practitioners and technical support will rise to 254,000. In the United States, the deficits for those two groups will rise to 1.1 million and to nearly 1.7 million, respectively, by 2030. Even Australia will suffer a significant shortfall, in health care practitioners and technical support: 168,000.

Exhibit 6 provides an overview of all six potential scenarios and gives an indication of the possible situations that may occur across them. For example, Australia will face a shortfall in the baseline COVID-19 projection of approximately 800,000 workers, assuming a low rate of technology adoption. At the other end of the spectrum—the severe COVID-19 projection, with a high rate of technology adoption—Australia will face a labor surplus of about 800,000.

Compared with the United States and Germany, Australia is projected to experience a substantial growth in labor supply. In 2002, the national government started offering cash subsidies to parents of newborns in an effort to lift the country’s fertility rate. The increase resulted in a baby boom of people who will enter the job market over the next decade. At the same time, Australia has significantly cut immigration for the foreseeable future in response to the economic challenges of the pandemic—a short-term effect that will lead to increased labor supply when immigration resumes. Nevertheless, the projected skills mismatch is unlikely to be fully resolved. Therefore, we expect higher levels of unemployment in some areas and more acute skills shortages in others.

The shortfall is even more pronounced in Germany, where the analysis shows a talent shortfall in five of the six potential scenarios we identified. Only a severe impact by the pandemic on GDP, combined with high technology adoption, would generate a net surplus of approximately 1 million employees. Germany faces the dual challenge of a birth rate that has remained low, at an average of 1.6 children per woman, combined with aging baby boomers who will retire in the next decade. Exacerbating this is a demand for workers that we anticipate will either remain constant or increase.

Germany faces the dual challenge of a low birth rate combined with aging baby boomers who will retire in the next decade.

Similarly, five of the six potential scenarios in the US show a shortfall (up to 12.5 million people), and only the severe COVID-19 trajectory, combined with a high adoption rate of technology, indicates a surplus (up to 4.5 million).

Although the adoption of technology is progressing at roughly the same pace in all three countries, demographic profiles suggest that they will face different challenges during the digital transition. However, they all share the need for a labor force that has the right composition of skills to meet the needs of the digital age, which will demand upskilling and reskilling on a large scale. In the baseline projection, all three countries will face a net workforce gap. In addition, a certain level of structural unemployment (defined as the difference between demand and supply) will prevail. Therefore, the challenge is more significant than the aggregate numbers suggest.

Building an Adaptive Workforce

The stark predictions for labor deficits suggest that all three of the countries we studied should take deliberate action to build a workforce that is ready for the future. Governments and corporate leaders need to understand the specific demographic challenges they face, where the biggest impact of automation will be, and how they can help individuals remain employable by maintaining their skills. They then need to ensure that workers continue to learn over time as demand for different skills evolves. In short, countries must build an adaptive workforce.

Through a deeper dive into the analysis, we can identify the job families (which make up the job family groups discussed above) with the highest absolute surpluses and shortfalls in 2030 for the baseline projection. (See Exhibit 7.) These job families reflect the areas with the highest need for action from all stakeholders. The US, Germany, and Australia share some similarities here. For example, all three show that information and record clerks constitute one of the occupations with the greatest overall surplus (1.9 million for the three countries)—an increase generated by the ability of new technology solutions to manage this task. Similarly, all three countries will see a steep shortage of business operations specialists (who analyze business operations and identify customer needs) as a direct result of the data made more widely available by technology.

Of course, although humans may no longer be needed for some tasks, they will nevertheless be necessary to help develop automation. Decisions must be made on the rules governing the use of new tools and how to implement and maintain the software or robots that are taking over those tasks. Despite eliminating the need for human employees for many routine and administrative tasks, technology can also create new jobs as the demand for software developers, data analysts, cybersecurity testers, and other digital specialists rises across all sectors. There may be a need to redeploy, upskill, or reskill people—and perhaps even to redefine any given job itself. Although these markets share characteristics in terms of technology adoption, significant differences emerge.

In the United States, for example, for every six jobs that are being automated or augmented by new technologies, one additional job will be needed in order to develop, implement, and run those new technologies. In the aggregate, those newly created roles will encompass 63 occupations, mostly in the fields of data science and software development.

Increased job automation will also create significant opportunities. Primarily, it will enable workers to undertake higher-value tasks. For example, the removal of mundane, repetitive tasks in legal, accounting, administrative, and similar professions opens the possibility for employees to take on more strategic roles. This also illustrates how automation will affect not only blue-collar jobs but white-collar occupations as well.

The removal of mundane, repetitive tasks in legal, accounting, administrative, and similar professions opens the possibility for employees to take on more strategic roles.

Meanwhile, core human abilities—such as empathy, imagination, creativity, and emotional intelligence, which cannot be replicated by technology—will become more valuable. The supply of talent for occupations that require these abilities—such as health care workers, teachers, and counselors—is currently limited, causing the high shortfalls we see in these job families. At the same time, crises such as the COVID-19 pandemic underscore the importance of these occupations in ensuring societal well-being.

Recommendations for Governments

Countries need to take the following actions to get ahead of current and future work imbalances in their employment markets.

Plan for the future workforce. Governments should have a central workforce strategy and policy unit in place to understand the current trends in workforce supply and demand; identify the gaps that exist in certain jobs, sectors, and skills; and predict the measures that will be needed to close those gaps. Specific resources include advanced-analytics models to predict changes over time and sufficiently granular sources of data that can generate insights into various regions, sectors, and demographics. Furthermore, the findings should be translated into strategic directions that are then implemented in specific policies and programs across government departments, including education, welfare, labor, and economics.

Rethink education, upskilling, and reskilling. Guided by strategic workforce planning, governments should create adult upskilling and reskilling programs at scale. Success requires working closely with the private sector and academia to develop more creative solutions that match the shifting realities of the labor marketplace over time. Governments also need to refocus education systems to develop so-called metaskills, such as logical thinking, reasoning, curiosity, open-mindedness, collaboration, leadership, creativity, and systems thinking.

In addition, education systems must become more flexible, moving beyond degree programs that require several years to complete and, instead, facilitating intermittent periods of study. They should also help people to obtain microcredentials and certifications tailored to industry needs (ideally created in partnership with the private sector) and to upgrade their skills on a regular basis.

The right solution will require a much broader set of educational formats to convey these skills in a sound way. Current education funding models need to shift from large, one-time subsidies to smaller, incremental payments spread over a person’s lifetime. This might mean, for example, creating lifelong learning accounts, such as those in a program offered by the Singapore government, which provide funding for a person’s education over their lifetime and can be drawn upon whenever they need to upgrade existing skills or gain new ones. Traditional education systems will need to apprise prospective students of the fields of study and types of degrees that are most aligned with the needs of the workforce, so they can make informed decisions about which path to pursue. This is especially true for students who are transitioning to higher education. What’s more, doing so would cut down on any future reskilling needs because citizens will have acquired the skill profiles demanded by the labor market right from the start.

Build career and employment platforms. To ensure that the labor market is working as efficiently as possible, some governments are creating comprehensive data and digital employment platforms so that workers can navigate to jobs and training opportunities more easily and quickly. A world-class platform helps citizens assess their skills, identify potential employment pathways, and close capability gaps through upskilling and reskilling opportunities. Critically, these platforms need to be continually updated and reinvented to ensure that they remain relevant and useful. In addition, governments need to establish their own employer brands in order to influence immigration patterns and attract employees with relevant skills from other countries.

Update social safety nets. Given the risk that automation poses for many jobs, policymakers need to focus on providing upskilling and reskilling opportunities for workers who are in transition, employed part-time, or unable or unwilling to adapt to the digital economy. Welfare policies need to adapt so the system can assist people who regularly enter and exit the workforce. Supporting those who do not profit directly from the positive effects of future technologies is critical to fuel a societal support for this major shift toward a more flexible and adaptive workforce. Funding all this will require governments to embrace automation in their own administrations as boldly as possible.

Drive innovation and support small and midsize enterprises (SMEs). SMEs may lack the funds to continually enhance their automation and thus will need support in the form of subsidized loans or investment tax breaks as they work to develop a digitally enabled workforce. Regulations for the use of advanced technologies should not overburden these SMEs, in order to avoid inhibiting their innovation. Supporting SMEs will help build the capabilities needed to drive innovation throughout the economy as well.

To ensure that current and future work imbalances do not have an impact on their financial stability and ability to compete, companies need to take the following actions.

Perform strategic workforce planning. As at the country level, a company should regularly assess the current size, composition, and development of its workforce. It should also evaluate future demand on the basis of strategic direction and determine the gaps for certain jobs and specific skills. Furthermore, it should proactively design the measures needed to close those gaps. These strategic measures need to be closely connected to the company’s overall planning for the medium term and need to be budgeted accordingly to ensure swift implementation.

Upskill and reskill existing workforces. Given the rapid shifts in skill requirements and the number of entirely new tasks and roles that are emerging, the labor market will be unable to supply sufficient new talent to fill available positions. Companies therefore need to supplement external hiring with internal development initiatives and on-the-job training.

Create a lifelong learning culture. Corporate training used to consist of certifications or intermittent training programs, but the digital economy will demand a constant upgrading of skills. Companies therefore need to build constant learning into their business models. Content and skill upgrades should be delivered in a variety of formats so that they can be integrated into the daily routine of every employee, ensuring a nimble and agile workforce.

Rethink talent recruitment and retention strategies. The combination of demand for digital skills and demographic shifts will put extreme pressure on the labor supply pipeline, creating fierce competition for talent. Thus, companies may need to shift the recruitment focus from hiring for skill to hiring for will: as some of the skills needed in the future (such as coding computer languages) will most likely be self-taught or come without an explicit certification, HR professionals will need to view candidate criteria with a more open mind and embrace diverse curricula. Companies will also need to find new ways of retaining their talent and equipping them with the skills that will enable them to stay relevant within the changing context in which the enterprise operates.

Companies may also opt to create an employee pool to which people with new skills can be added without yet knowing which field of operations they’d be best suited for. Companies could choose to assess intangible skills with trial periods as well. In a postpandemic era, the higher prevalence of remote working will allow companies to access international and more fluid talent pools that are outside the companies’ main markets. For many organizations, this will be a completely new source of talent to explore and manage.

Recommendations for Individuals

In order to ensure that they are prepared for the jobs of the future, individuals will have to take greater responsibility for their own professional development, whether that means through upskilling or reskilling. They should take the following actions.

Make lifelong learning the new normal. Whether through programs offered by employers or through private channels, continuous learning and the acquisition of new skills must become central to an individual’s working life. Individuals should also invest not only in digital skills but also in metaskills, which will serve them well regardless of shifts in the market.

Continuous learning and the acquisition of new skills must become central to an individual’s working life.

Remain focused on upskilling and reskilling. More and more sources of information about jobs and skills will become available in the coming years. Many governments are establishing overviews of jobs and skills that are currently in demand and creating forecasts for the future. Individuals need to pay attention to these sources of information and update their skills accordingly, either by searching out high-quality providers of education or by charting their own course amid the vast amount of online-learning offers.

Become more flexible when developing a career path. Frequent career changes and lateral moves into similar job positions will become increasingly necessary. Therefore, workers should remain flexible throughout their careers, looking for positions where their existing skill sets can be applied successfully as well as updating their skill sets according to where their own interests match the market’s needs.

As countries prepare to meet the demands of the digital age, they must understand the challenges that lie ahead. This means making use of more sophisticated analytical models to predict supply and demand in the labor market and integrating them into the foundation of their workforce strategies. It also means focusing on managing the transition to a future workforce so that the economic and social friction associated with the mismatch of supply and demand is minimized.

To reduce the mismatch in skills, governments should update the education system. They should create more flexible institutions that can anticipate the future needs of companies and refocus on metaskills.

Companies need to invest in corporate academies, training partnerships, and constant upskilling and reskilling of their existing workforces. They should also transform their HR functions and processes to cater to the shift in approach needed to hire and retain talent with the new skills in demand. Companies that make these investments and significant changes in their own processes stand to gain a substantial competitive advantage over those that stick with their current approach.

Countries that leverage education to create attractive locations for companies will gain a competitive edge over their static neighbors.

Perhaps more important, given the speed of the digital transformation, it is urgent to make such investments today. Countries that leverage education to create attractive locations for companies will gain a competitive edge over their static neighbors. Companies that hesitate will find themselves unable to access the talent they need and will fail to capitalize on the opportunities that technology brings. Surviving and thriving in the digital age means understanding current shifts, predicting future transformations, and responding rapidly to build an adaptive, future-ready workforce that can support a strong and equitable economy.